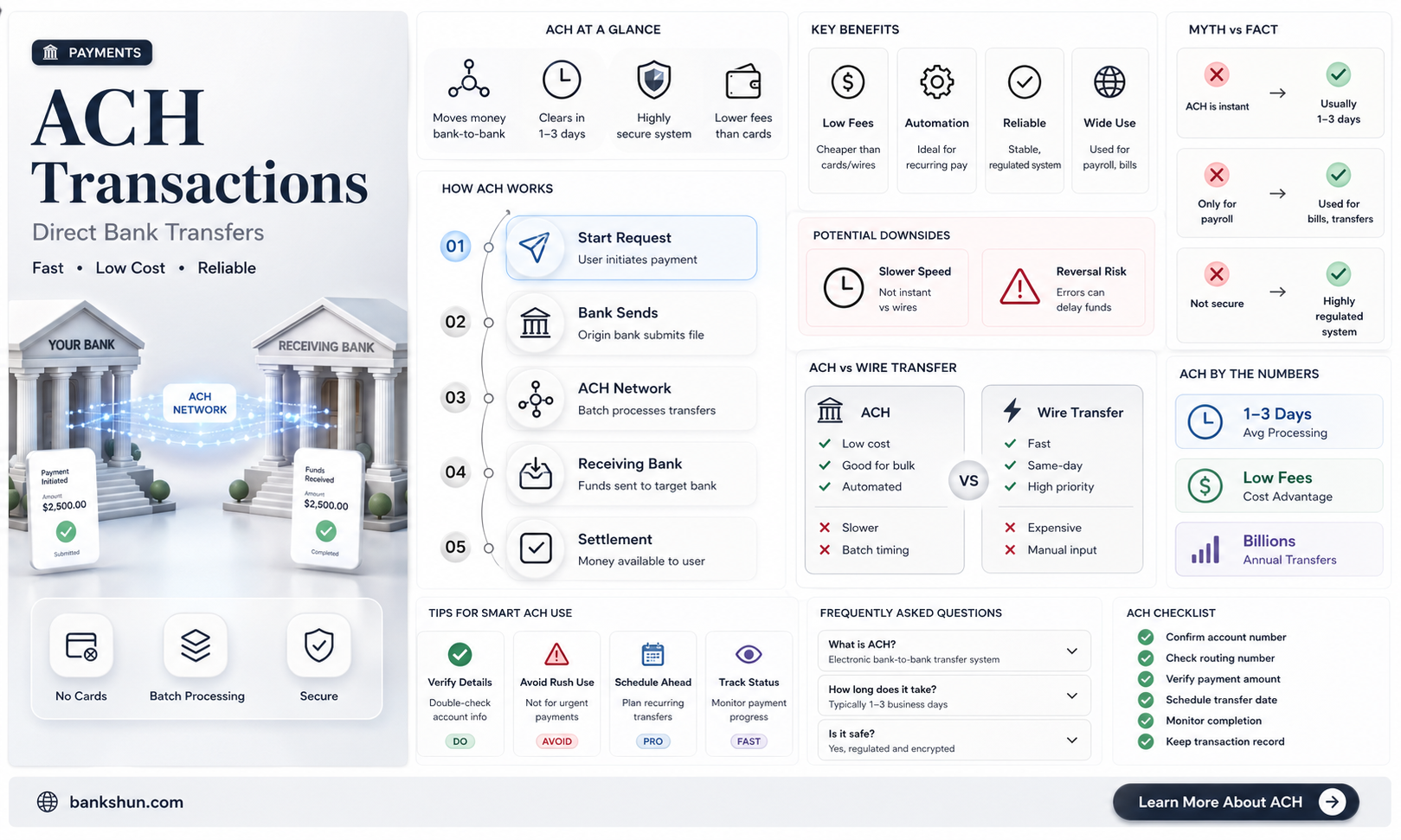

ACH transfers are electronic money transfers sent from one bank to another across the Automated Clearing House (ACH) network. This network is a digital hub that transfers funds, allowing banks, credit unions, and other institutions to bundle direct deposits or payments and send them at specific times of the day. ACH transfers are a secure, reliable, and affordable way to send and receive money between bank accounts. They are ideal for payroll, bill payments, and even P2P payments.

| Characteristics | Values |

|---|---|

| Full Form | ACH stands for Automated Clearing House |

| Type | There are two main types of ACH transfers: credits and debits. |

| Transfer Limit | Same-day ACH payments currently have a $1 million limit per transaction |

| Security | ACH transfers are secure and follow the latest in financial technology requirements. |

| Reversibility | ACH transfers can be reversed |

| Speed | ACH transfers are slower than wire transfers. They can take several business days. Around 80% of ACH payments are settled on the same day but are almost always completed in one to three business days. |

| Cost | ACH transfers cost a few bucks at most. |

| Usage | ACH transfers are used for payroll, bill payments, and P2P payments. |

Explore related products

What You'll Learn

![]()

ACH transfers are electronic money transfers

ACH transfers are a secure, reliable, and affordable way to send and receive money between bank accounts. They are ideal for payroll, bill payments, and even peer-to-peer (P2P) payments. The two main types of ACH transfers are credits and debits. With an ACH credit, you receive money, and with an ACH debit, you send money. For example, when an employer sends a credit to an employee's account, money is transferred directly from the employer's account to the employee's. This is an ACH deposit.

ACH transfers are also useful for direct payments. For example, if you split a bill with a friend, they can use a payment app to send you their share. This type of ACH transaction works by sending and receiving funds. Direct payments include ACH credits and debits. By automating payments through online bill pay, you can avoid having to put a check in the mail every month. It can also help you avoid missing due dates if your account is set up to automatically pay your bills on time.

ACH transfers are also a cost-effective alternative to other digital payment methods, such as wire transfers or card payments. They are usually cheaper than wire transfers, which typically cost around $20 to $30 within the US. ACH transfers are also less costly than credit card payments. For businesses, this can result in significant savings over time. However, it is important to note that ACH transfers can take several business days to process, while wire transfers are processed in real time.

ACH Banking: How Does It Work?

You may want to see also

Explore related products

![]()

They are a secure, reliable, and affordable way to send and receive money

ACH transfers are a secure, reliable, and affordable way to send and receive money between bank accounts. They are electronic money transfers sent from one bank to another across the Automated Clearing House (ACH) Network, a digital hub that transfers funds. The ACH network is administered by the National Automated Clearing House Association (Nacha), an independent organisation owned by a large group of banks, credit unions, and payment processing companies.

ACH transfers are a safe and reliable way to send and receive money. Nacha has strict security regulations for any institution or organisation involved with ACH transactions, including banks, businesses, and third-party processors. All sensitive information, such as bank account numbers, needs to be encrypted. As a result, ACH payments are secure against fraud. The ACH network also works with banks to identify suspicious payments to prevent fraud.

ACH transfers are also a cost-effective way to send and receive money. They are cheaper than wire transfers and credit card payments, which can cost from $20 to $30 to send money within the US. ACH transfers, on the other hand, cost a few dollars at most. For businesses, this can lead to significant savings over time. Additionally, ACH transfers are often free to receive, whereas there is usually a fee to receive a wire transfer.

ACH transfers are also reliable for sending and receiving money. They are a convenient way to send and receive money quickly, with around 80% of ACH payments settled on the same day and almost always completed within one to three business days. While wire transfers can be faster, taking only a few hours, they are also more expensive. ACH transfers are ideal for recurring payments, such as payroll and bill payments, as they can be automated, helping to avoid missing due dates.

Explore Citizens Bank Park's Seating Capacity

You may want to see also

Explore related products

![]()

ACH transfers are cheaper and slower than wire transfers

ACH transfers are electronic money transfers sent from one bank to another across a network called the Automated Clearing House (ACH) Network. The ACH network is a digital hub that transfers funds, allowing banks, credit unions, and other institutions to bundle direct deposits or payments and send them at specific times of the day.

ACH transfers are considered more secure than wire transfers because they are federally regulated, and the process takes a few days to complete, allowing time to reverse the transaction if fraud is discovered. Wire transfers are immediate and irreversible, so it is challenging to reverse the process if necessary. ACH transfers are ideal for everyday transactions like paying bills, sending money through apps, or receiving your paycheck. They are also useful for payroll, bill payments, and P2P payments.

Wire transfers are direct transfers of money from one institution to another, usually within the same day. They are faster and usually cost a larger fee. Wire transfers are generally used for high-value transactions and are reserved for big transfers of money or situations where funds need to be sent quickly and securely. Wire transfers are the go-to option when you need to send a large amount of money.

ACH transfers are free or inexpensive, whereas wire transfers have high fees, sometimes up to $50 per transaction. While some banks charge customers an ACH fee as part of bill-paying services, they rarely charge for incoming ACH payments such as weekly paychecks. Wire transfer fees are set by the banks or companies handling the transaction and vary depending on the type of service.

Exploring Red Bank, NJ: Fun Things to Do

You may want to see also

![]()

They can be reversed

ACH transfers are electronic money transfers sent from one bank to another across an Automated Clearing House (ACH) Network. This is a digital hub that transfers funds. Banks, credit unions, and other institutions use the network to bundle direct deposits or payments and send them at specific times of the day. It is a convenient, secure, and reliable way to send and receive money quickly.

ACH transfers can be reversed under certain circumstances. This process is known as an ACH return or ACH reversal. This is in contrast to wire transfers, which are typically not reversible. If there is a problem with an ACH payment, it may be possible to stop or reverse it. This can be done by the sender or the bank.

If the sender wishes to reverse an ACH payment, they have around 24 to 48 hours to do so. In many cases, the sender may even be able to stop an ACH payment online. After this timeframe, the funds may have already been deposited and cleared, and it may not be possible to reverse the payment. However, with evidence and an investigation, the bank may still be able to return the money via a separate transaction if fraud or another valid reason is discovered.

There are several reasons why a sender may wish to reverse an ACH payment, including insufficient funds, suspected fraud or unauthorized activity, errors in the payment information or account details, or a stop payment request by the account holder. Other reasons for reversals include disputes between the sender and receiver.

Banks can also reverse ACH payments under certain circumstances. If one of several errors occurs, the bank must reverse the charges within five days and notify the affected account owners of the reversal. These errors include insufficient funds, suspected fraud or unauthorized activity, and errors in the payment information or account details.

When Do Bank Transfers Go Through?

You may want to see also

![]()

ACH transfers are administered by the National Automated Clearing House Association

ACH transfers are a secure, reliable, and affordable way to send and receive money between bank accounts. They are ideal for payroll, bill payments, and even peer-to-peer (P2P) payments. ACH transfers are administered by the National Automated Clearing House Association (Nacha), an independent, self-regulating, not-for-profit organisation owned by a large group of banks, credit unions, and payment processing companies.

The Automated Clearing House *(ACH)* is an electronic funds-transfer system that facilitates payments in the US and internationally. The ACH network acts as a financial hub and helps people and organisations move money from one bank account to another. ACH transfers are processed by an ACH operator on the ACH network, which is managed by Nacha. Banks use ACH transfers to move money between different accounts or to transfer funds to another bank, to process recurring bill payments, business-to-business payments, e-commerce payments, and P2P transactions.

The ACH network includes US banks and their territories. ACH payments are completely electronic, either as a direct deposit (credit) or a direct payment (debit). The originator (such as an employer) initiates the payment or deposit by giving instructions to their bank. The bank sends digital payment files to the ACH network. The ACH network passes those payment files on to the receiving bank. The receiving bank then adds money to or takes money from the receiver's bank account, depending on the type of ACH transaction that was initiated.

ACH transfers usually take one to three business days to clear. However, recent changes to Nacha's operating rules have expanded access to same-day ACH transactions, allowing for same-day settlement of most ACH transactions. Same-day ACH transactions currently have a $1 million limit per transaction.

FDIC Insurance: Which Banks Offer the Highest Coverage?

You may want to see also

Frequently asked questions

ACH stands for Automated Clearing House.

ACH transactions are electronic money transfers sent from one bank to another across the ACH network. The originator (such as an employer) initiates the payment or deposit by giving instructions to their bank. The bank then sends digital payment files to the ACH network, which passes those payment files on to the receiving bank.

ACH transactions are a secure, reliable, and affordable way to send and receive money between bank accounts. They are ideal for payroll, bill payments, and P2P payments. They are also faster and cheaper than paper checks and credit card payments.

ACH transactions are typically settled on the same day but can take up to one to three business days.