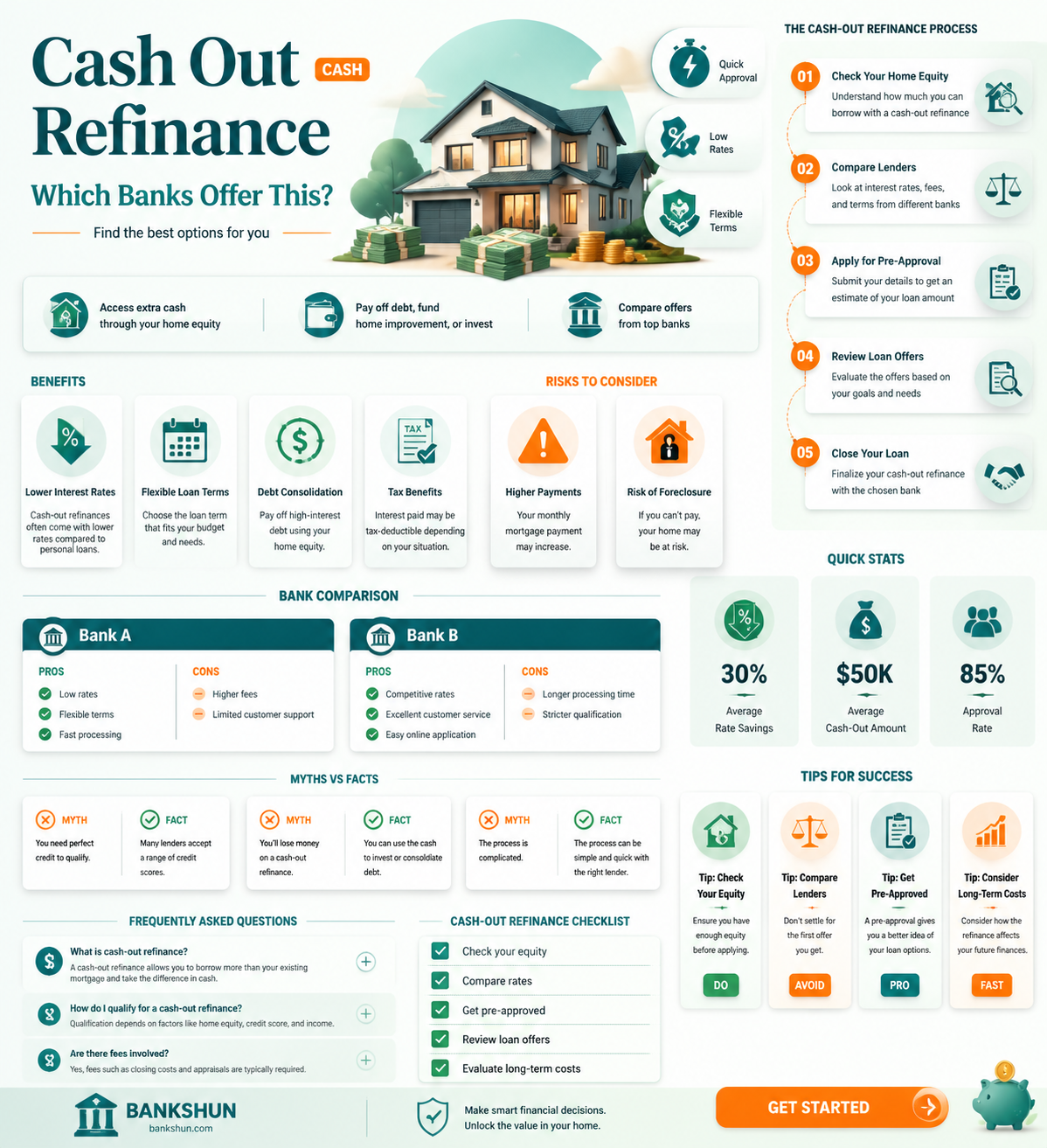

Cash-out refinancing is a method of borrowing money that is available through either a fixed-rate or adjustable-rate mortgage. It is an alternative to a home equity loan. This process involves negotiating new mortgage terms and borrowing funds for one-time expenses. A cash-out refinance replaces your current mortgage with a new, larger loan, and you receive the cash difference between the new amount borrowed and your old mortgage balance. This type of refinancing can be advantageous if you want a lower interest rate, a different type of home loan, or to pay off your loan faster. However, it is important to consider the risks and ensure that the cash-out refinance improves your financial situation rather than worsening it.

| Characteristics | Values |

|---|---|

| Purpose | To access cash by replacing your current mortgage with a new, larger loan |

| Requirements | A credit score of 620 or higher, a DTI of 43% or less, and at least 20% equity in your home |

| Benefits | Lower interest rates, lower monthly payments, access to a large amount of money, ability to negotiate new mortgage terms, and the freedom to use the money as desired |

| Risks | Increased mortgage balance, potential for prolonged repayments, and risk of foreclosure if unable to repay the loan |

| Alternatives | Home equity line of credit (HELOC) or a home equity loan |

| Timeframe | Typically 30 to 45 days, depending on property size, financial complexity, and appraisal/inspection duration |

| Costs | Closing costs of 3-6% of the new mortgage, which can be rolled into the loan but may result in higher monthly payments |

Explore related products

$9.91 $26.99

$5.99 $12.99

What You'll Learn

![]()

Cash-out refinance vs home equity line of credit (HELOC)

There are three main ways to access your home equity and turn it into cash: cash-out refinancing, home equity lines of credit (HELOCs), and home equity loans. All are home-secured debts, meaning they are backed by your residence.

Cash-out refinance

Cash-out refinancing replaces your current mortgage with a new, bigger one, with the difference between the two going to you in cash. This results in a new mortgage loan, which may have different terms than your original loan, including a different type of loan, a different interest rate, and a longer or shorter time period for paying off your loan. This option is available through either a fixed-rate mortgage or an adjustable-rate mortgage. Cash-out refinancing typically takes 30 to 45 days to complete, though this may vary depending on individual circumstances.

Home equity line of credit (HELOC)

A HELOC is a revolving, open line of credit that functions much like a credit card. You can borrow money as needed, repay it, and then borrow again. A HELOC is usually taken out in addition to your existing first mortgage, though it can be a first mortgage if your house is completely paid for and you have no other mortgage. A HELOC has a variable interest rate that changes in conjunction with an index, typically the US Prime Rate. This means that your interest rate will increase or decrease when the index increases or decreases.

Both options have advantages and disadvantages. A cash-out refinance may be the right choice if you want to take advantage of lower interest rates and get cash in hand. However, it may not be the best option if you are looking for quick approval, as it can take a while to get set up. A HELOC, on the other hand, may be preferable if you are looking for flexibility in terms of how much money you take out and when you take it. It is also a good option if you are looking for quick access to funds, as you can typically get approved within a month. However, it is important to keep in mind that the interest rate on a HELOC can fluctuate, which means the rate could rise.

Capital One: Physical Branches or Online-Only?

You may want to see also

Explore related products

![]()

Pros and cons of cash-out refinance

Cash-out refinancing is a way to access a large sum of cash by replacing your current mortgage with a new, larger loan. The new loan pays off your original mortgage, and you receive the difference in cash.

Pros

- You can get a large sum of money by unlocking your home equity.

- Interest rates are generally lower than for home equity loans or lines of credit.

- It can be used to pay for important expenses such as home upgrades, education, or consolidating high-interest debt.

- Qualifying for cash-out refinancing is typically easier than other loan types as you already own the home and have a payment history.

Cons

- It increases your debt burden and reduces your equity.

- It could extend the term of your mortgage, meaning you'll be paying it off for longer.

- There are closing costs, which can range from 2% to 5% of the loan amount, and other fees associated with the transaction.

- If interest rates are higher, a cash-out refinance may not make financial sense.

- You will likely need a credit score of 620 or higher to qualify, and the higher the loan-to-value ratio, the higher the credit score required.

- Borrowing more than 80% of the value of your home may require you to pay private mortgage insurance, adding to your monthly costs.

In summary, a cash-out refinance can be a good option if you need access to a large sum of money and want to take advantage of potentially lower interest rates compared to other loan types. However, it's important to consider the potential drawbacks, such as increased debt, reduced equity, and the possibility of paying more in interest and fees over the long term.

Calculating Yield Percentages: A Banking Guide

You may want to see also

Explore related products

![]()

How to qualify for cash-out refinance

A cash-out refinance is a type of loan that replaces your current mortgage with a new, larger one, allowing you to convert some of your home's equity into cash. This type of loan can be beneficial if you need access to a large sum of money to improve your financial situation, such as adding value to your home or funding education. However, it's important to remember that a cash-out refinance increases your mortgage balance, and failing to repay the loan could result in losing your home. Here are some steps and qualifications to help you understand how to qualify for a cash-out refinance:

Steps to Qualify for a Cash-Out Refinance:

- Determine your goals: Assess whether a cash-out refinance aligns with your financial goals. Ensure that the funds will improve your financial situation and that the larger mortgage payments will not be a burden.

- Shop around for lenders: Different lenders will have varying criteria, closing costs, and fees associated with cash-out refinances. Compare rates and terms from multiple lenders to find the best deal for your specific financial situation.

- Choose a lender and apply: Once you've found a suitable lender, go through their application process. Be prepared to provide proof of income, such as financial statements and tax returns. Your home will also need to be professionally appraised to determine its value.

- Secure the loan and close: After your application has been approved, work with the lender to finalise the loan and complete the necessary closing processes.

Qualifications for a Cash-Out Refinance:

- Credit score: A higher credit score will generally help you secure a better interest rate. The minimum credit score requirement for a conventional loan is typically 620, but a score of 600 or higher may also be acceptable.

- Debt-to-Income Ratio (DTI): Lenders usually require a DTI of 43% or less. Your DTI is calculated by dividing your monthly debt payments, including your current mortgage, by your gross monthly income. If your DTI exceeds 43%, you may need six months of reserves in the bank.

- Home Equity: Most lenders require you to have at least 20% equity in your home. This means you must have paid off at least 20% of the current appraised value of your house.

- Loan-to-Value Ratio (LTV): Lenders typically allow a maximum loan amount of up to 80% of your home's value, but some may offer up to 90%. This means you can borrow up to 80%-90% of your home equity.

- Ownership and Payment History: With a conventional loan, you must have owned the house for at least 12 months to qualify. VA loan borrowers must wait at least 210 days, while borrowers with a loan backed by the Federal Housing Administration (FHA) need to have made 12 months of on-time payments before doing an FHA cash-out refinance.

- Income and Property Value: Similar to applying for a new mortgage, your income and property value will be considered when qualifying for a cash-out refinance.

Jackson's Veto Power: The Bank's Demise and its Aftermath

You may want to see also

Explore related products

![]()

Best cash-out refinance lenders

A cash-out refinance is a method of borrowing from your home's equity to convert the difference into cash. This is done by replacing your current mortgage with a new, larger one. The amount of cash you can borrow depends on your home equity, which is calculated by subtracting the amount you owe on your mortgage from the amount your home is worth. For instance, if your home is valued at $300,000 and you owe $100,000, you have $200,000 in equity. Typically, lenders allow a maximum loan amount of 80% of your home's value, which means you could refinance your home for up to $240,000 in this case.

Rocket Mortgage

Rocket Mortgage, the largest mortgage lender by volume, offers a seamless digital experience and fast closings. It has competitive average rates and a convenient online experience. Borrowers can apply via a mobile app. However, the average origination fees are on the higher end.

Navy Federal Credit Union

Navy Federal Credit Union is best for active military and veterans. They are known for their VA loans and offer flexible VA-like loan options for military borrowers who have exhausted their VA benefits. They provide fixed- and adjustable-rate options that can save you money.

U.S. Bank

U.S. Bank is recommended for the overall mortgage experience. They offer cash-out refinancing to a conventional, FHA, or VA loan, which may result in a better rate and lower monthly payments. They also provide a free tool to check your credit score if you are a U.S. Bank client.

AmeriSave

AmeriSave offers helpful online tools, customer service, and comparatively low rates. They also provide refinance discounts for eligible purchase loan customers. However, they do not originate mortgages in the state of New York, and their mortgage rates are not published online.

When choosing a cash-out refinance lender, it is important to consider factors such as loan volume, origination fees, rate transparency, and the ease of their online application. Additionally, ensure that you understand the terms of the loan and how it fits your financial situation.

Locating Sensor 1 on Bank 1: Where is it?

You may want to see also

Explore related products

![]()

Alternatives to cash-out refinance

If you are looking for alternatives to a cash-out refinance, there are a few options available to you.

Firstly, a home equity loan is a popular alternative. This is a second mortgage that provides a lump-sum payment. It has a fixed rate and you start repaying it immediately. This option is often the cheapest way to access your home's equity, thanks to lower interest rates and minimal closing costs compared to other options.

Another option is a home equity line of credit (HELOC). This is a revolving line of credit, similar to a credit card, that allows you to borrow money when you need it. HELOCs usually have variable interest rates that fluctuate with the prime rate. They are typically taken out in addition to your existing first mortgage.

Home equity investments are another alternative to cash-out refinancing. These agreements typically last 10-30 years and are accessible to homeowners with lower credit scores or limited income. There are no restrictions on how you use the money. However, they are often not the lowest-cost way to access equity.

Finally, a sale-leaseback agreement allows you to access home equity without refinancing. This involves selling your home to another entity, cashing out the accrued equity, and then leasing your home back from the new owner.

Removing Banks from Apple Pay: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Cash-out refinance is a way to access cash by replacing your current mortgage with a new, larger loan. It is considered a second mortgage and will have its own term and repayment schedule.

A cash-out refinance typically takes 30 to 45 days to complete. The loan proceeds are first used to pay off your existing mortgage(s), including closing costs and any prepaid items. Any remaining funds are then paid out to you.

A cash-out refinance can be beneficial if you want a lower interest rate, a different type of home loan, or to pay off your loan amount faster. It can also be useful if you need money for major home repairs or renovations or want to consolidate high-interest debt.

![[2-Pack] Mini Portable Charger 5000mAh Power Bank,3A PD USB C Cell Phone Portable Power, LCD Display Battery Pack Compatible with iPhone 16/15/15 plus/15 pro/15 pro Max/Android/Samsung/Moto/LG etc](https://m.media-amazon.com/images/I/61JTODtGlRL._AC_UL320_.jpg)