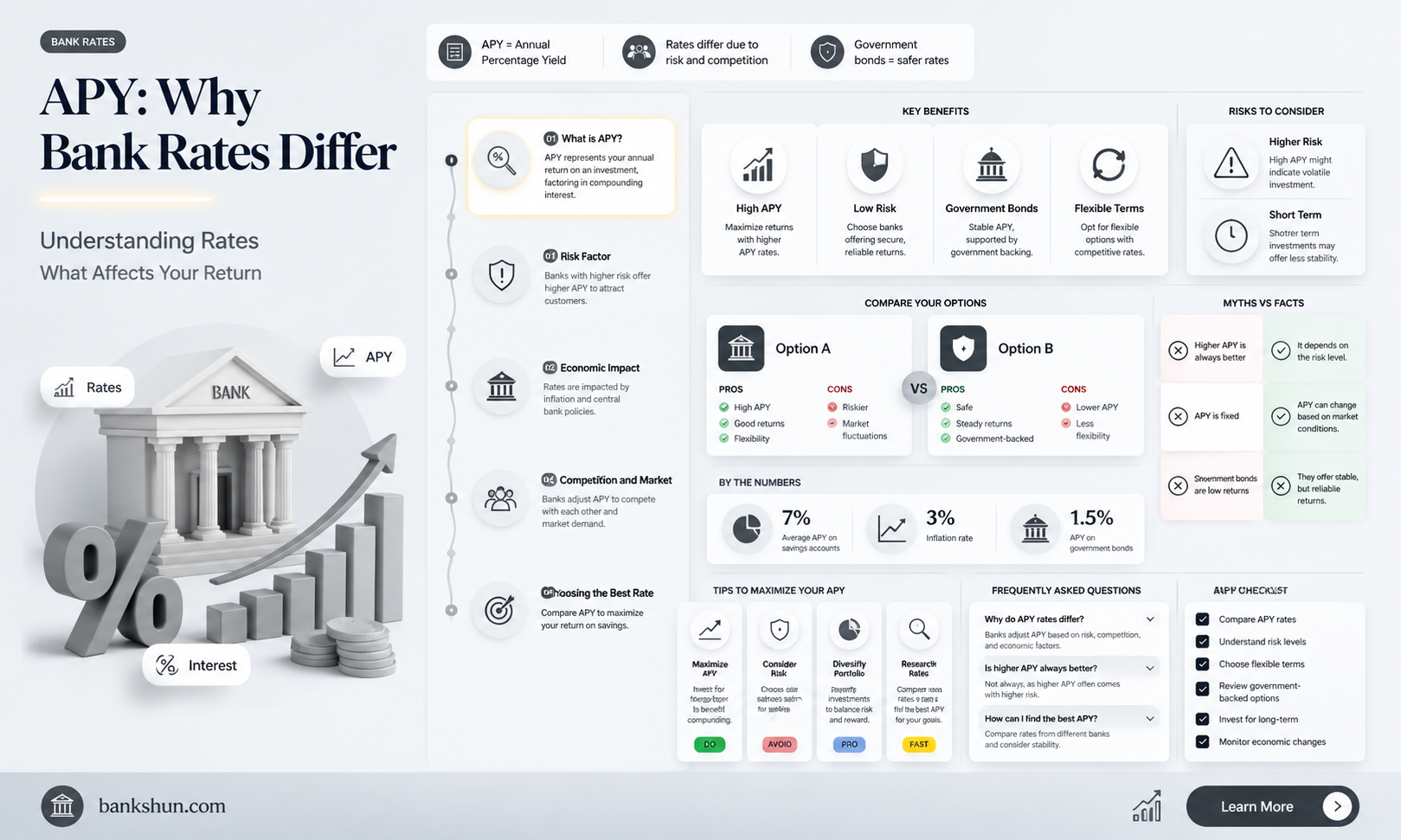

APY, or annual percentage yield, is the rate of return on money in a bank account, taking compound interest into account. Banks determine annual interest rates for savings and other interest-bearing accounts based on their analysis of economic factors. The type of savings account may also influence the APY offered. Banks may compensate customers who agree to maintain a higher balance in an account with a higher APY. Online banks tend to offer higher APYs because they don't have to operate branches, and most savings, money market, and checking accounts have variable APYs. Therefore, APYs are not the same at every bank.

| Characteristics | Values |

|---|---|

| APY meaning | Annual Percentage Yield |

| APY calculation | Takes into account the interest rate and compounding frequency |

| APY vs APR | APR focuses on how much interest is paid for money borrowed, while APY refers to how much interest is earned on savings and includes compounded interest |

| APY variability | APY is variable and subject to change at any time |

| APY comparison | APY differs across banks, with online banks tending to offer higher APYs due to lower operational costs |

| APY and account types | Checking accounts typically have the lowest APY, while savings accounts and CDs may offer higher APYs depending on the bank and account features |

| APY and balance | Banks may offer higher APYs for customers who maintain higher balances in their accounts |

Explore related products

What You'll Learn

![]()

APY vs APR

APY stands for Annual Percentage Yield, which is the effective rate of return on an investment for one year, taking compounding interest into account. Banks in the US are required to include the APY when they advertise their interest-bearing accounts. APY is calculated by taking the product of 1 and the periodic rate and dividing it by the number of compounding periods. This result is then raised to the power of the number of periods the rate is applied for and finally subtracting 1 from the resultant figure.

APR, or Annual Percentage Rate, is the yearly rate charged for borrowing money. It includes fees but does not include compounding. APR is calculated by multiplying the periodic interest rate by the number of periods in a year in which the periodic rate is applied.

APY and APR are both used to calculate interest for investment and credit products. However, they are not interchangeable. APY is generally used for savings and fixed investments, while APR is used for loans. The difference between APR and APY increases as interest is compounded more frequently.

Understanding Point-of-Sale Banking Systems

You may want to see also

Explore related products

![]()

High-yield savings accounts

When it comes to high-yield savings accounts, there are a few key things to keep in mind. Firstly, the annual percentage yield (APY) is the effective rate of return on an investment for one year, taking compounding interest into account. This means that the APY reflects how much interest you earn on your savings over time. Banks determine annual interest rates for savings accounts based on economic factors and the type of savings account.

It's important to note that savings APYs are variable and may change over time. When choosing a high-yield savings account, look for accounts with high rates, low or no fees, and convenient withdrawal options. Some accounts may also offer automatic savings features. To calculate the APY of a savings account, you need to know the interest rate and compounding frequency. The formula involves the interest rate and the number of compounding periods.

Online banks often offer higher APYs due to lower overhead operational costs. Additionally, some banks may offer higher APYs for customers who maintain higher balances or agree to time restrictions, such as certificates of deposit (CDs). CDs lock in an APY in exchange for leaving your money deposited for a set period. However, early withdrawal penalties may apply.

When comparing APYs between banks, ensure you are considering the same types of accounts and compounding frequencies. The compounding effect can significantly impact the interest accrued. Federal Deposit Insurance Corporation (FDIC) insurance is also an important consideration, as it ensures your money is protected up to certain limits.

As of August 2025, some of the best high-yield savings accounts include EverBank's Performance Savings account, BrioDirect's High-Yield Savings account, TAB Bank's TAB Save account, and Bask Bank's Interest Savings account. These accounts offer competitive interest rates and may provide additional features to make saving easier.

Best Covered Seats at Citizens Bank Park?

You may want to see also

Explore related products

$33.53 $42.99

![]()

Online banks offer higher APYs

APY, or annual percentage yield, is the rate of return on money in a bank account, including compound interest. Banks determine annual interest rates for savings and other interest-bearing accounts based on their analysis of economic factors. The type of savings account may also influence the APY offered. Banks may compensate customers who agree to maintain a higher balance in an account with a higher APY. Time-restricted accounts, such as certificates of deposit, may also earn higher rates of return as long as the customer doesn't withdraw their money before the term ends.

Online banks tend to offer higher APYs because they don't have to operate branches, allowing them to save on overhead costs and pass those savings on to customers. For example, the Axos ONE Savings account offers a promotional rate of up to 4.46% APY. The Rising Bank High Yield Savings Account offers a competitive interest rate but requires a relatively high minimum opening deposit of $1,000.

When comparing APYs, it's important to consider the compounding frequency, as accounts with more frequent compounding may offer higher APYs. For example, Bask Bank offers compounding daily, which can result in a higher APY than banks that compound less frequently. Additionally, promotional bank accounts or bank account bonuses may offer higher fixed APYs up to a specific level of deposits. For instance, a bank may offer 5% APY on the first $500 deposited and then pay 1% APY on all other deposits.

It's worth noting that APYs are variable and can change at any time. Therefore, it's essential to understand the difference between interest rates and APYs to make informed financial decisions.

Wells Fargo ATM Access for Advisors

You may want to see also

Explore related products

![]()

APY and compounding interest

APY, or Annual Percentage Yield, is the rate of return on money in a bank account over one year, taking compound interest into account. Banks in the US are required to include the APY when they advertise their interest-bearing accounts.

APY is calculated using the interest rate and compounding frequency. The compounding frequency is the number of times that interest is added to the principal balance, with future interest payments calculated on the new, larger balance. This compounding effect means that two investments with the same interest rate can have different yields. For example, a 6% interest rate with monthly compounding will yield a higher APY than a 6% interest rate paid at maturity, as the monthly compounding will result in a larger principal balance at the end of the year.

APY is often confused with APR, or Annual Percentage Rate. APR is used to calculate the interest paid on borrowed funds, such as credit cards or loans, and includes fees. APR does not include compounded interest. APY, on the other hand, calculates the interest earned on savings and includes compounded interest. The difference between APR and APY increases as interest is compounded more frequently.

The type of savings account can influence the APY offered. For example, online banks tend to offer higher APYs due to lower operating costs. Banks may also offer higher APYs to customers who maintain a higher balance in their account. Time-restricted accounts, such as certificates of deposit (CDs), may also earn higher APYs, provided that the customer does not withdraw their money before the term ends.

Israeli Settlements: Legality in the West Bank

You may want to see also

Explore related products

![]()

APY and bank account types

APY, or annual percentage yield, is the rate of return on money in a bank account, including compound interest. Banks in the US are required to include the APY when they advertise their interest-bearing accounts. APY is calculated using the interest rate and compounding frequency. The more frequently interest compounds, the higher the APY.

The type of savings account can influence the APY offered. Banks may offer higher APYs to customers who maintain a higher balance in their accounts. Time-restricted accounts, such as certificates of deposit (CDs), may also earn higher rates of return, provided that the customer does not withdraw their money before the term ends. CDs are considered low-risk and generally offer a guaranteed rate of return that is higher than a savings account. However, early withdrawal penalties may apply.

Checking accounts, on the other hand, typically have lower APYs because there is no risk or sacrifice for the consumer. Money market accounts (MMAs) are another option for individuals looking to save for shorter-term goals. While these accounts may require larger minimum balances and have transfer limitations, they can be a safe way to earn interest and grow your savings.

It is important to note that APY is different from APR, or annual percentage rate. APR represents the yearly rate charged for borrowing money and includes fees, but it does not take into account the effects of compounded interest. APY, on the other hand, refers to the interest earned on funds in a bank account and takes compounding into account.

When comparing different bank accounts, it is essential to consider both the APY and the compounding frequency to make an informed decision. Online banks tend to offer higher APYs due to lower overhead operational costs.

Vernon Hill: The Owner of Metro Bank

You may want to see also

Frequently asked questions

APY stands for Annual Percentage Yield. It is the effective rate of return on an investment for one year, taking compounding interest into account.

No, APYs vary across different banks and financial institutions. Banks determine their own annual interest rates for savings and other interest-bearing accounts based on their analysis of economic factors.

The type of savings account can influence the APY offered. Banks may offer higher APYs to customers who maintain a higher balance in their accounts. Time-restricted accounts, such as certificates of deposit (CDs), may also earn higher APYs. Online banks tend to offer higher APYs due to lower overhead operational costs.

To calculate a savings account's APY, you need to know the interest rate and compounding frequency. You can then use the APY formula, where "r" equals the interest rate, and "n" represents the number of compounding periods. By comparing the compounded APY of different banks at an equivalent rate, you can make an informed decision.