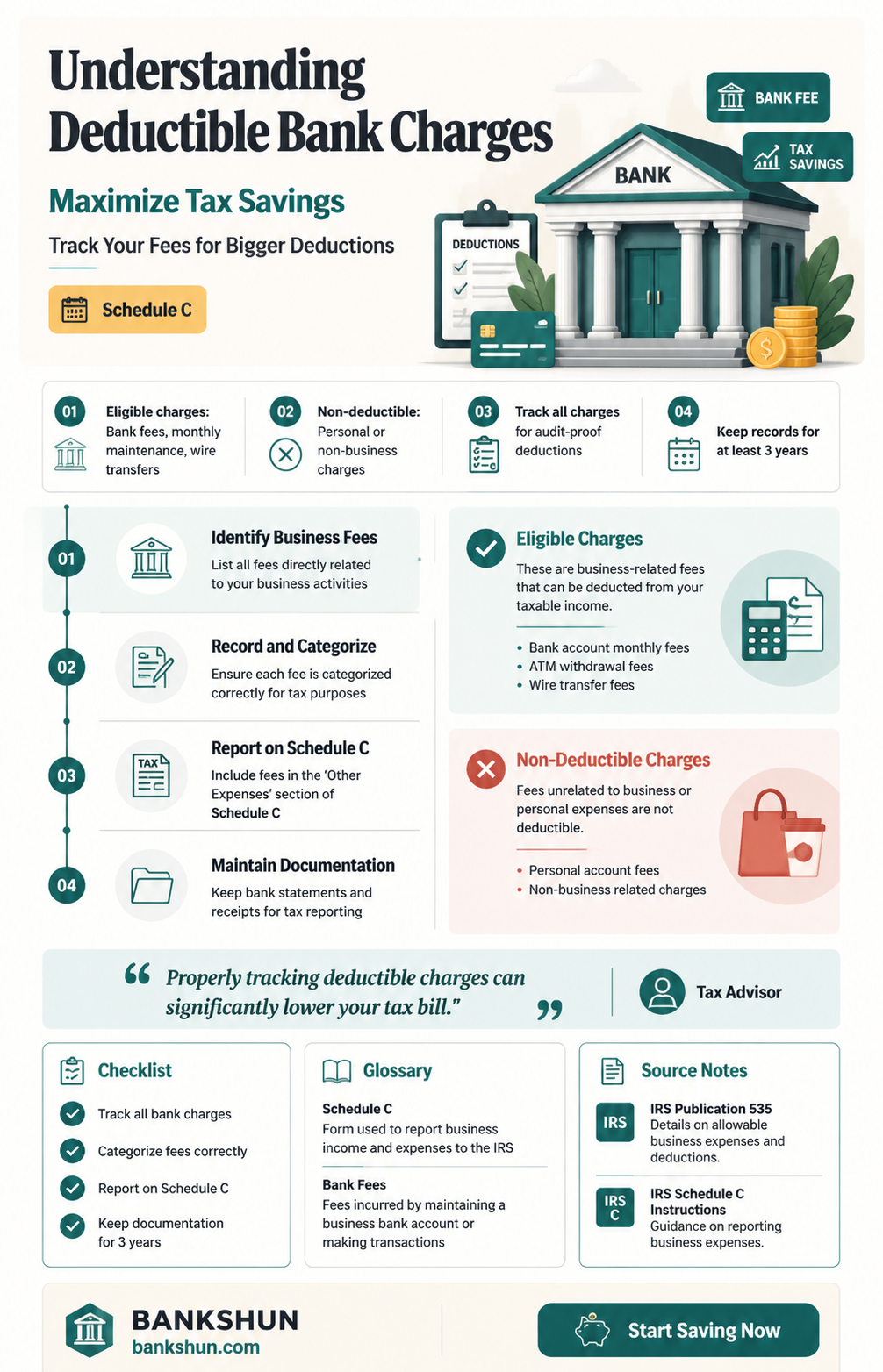

Bank fees are often considered ordinary and necessary expenses incurred in the course of running a business. These fees are tax-deductible if they are charged on a business bank account and are considered business expenses. This includes maintenance fees, ATM charges, overdraft fees, wire transfer fees, check fees, and service charges. Accurate reporting of these fees on Schedule C, a form used by sole proprietors to report income and expenses, is crucial for compliance and minimizing tax liability.

| Characteristics | Values |

|---|---|

| Bank charges deductible on Schedule C | Maintenance fees, ATM charges, transaction fees, wire transfer fees, check fees, overdraft fees, service charges, monthly fees, travel fees |

| Requirements for deduction | Bank charges must be related to a business bank account and be necessary for business operations |

| Benefits of accurate reporting | Minimizes tax liability, reduces risk of audits, ensures compliance with IRS requirements, optimizes tax deductions |

Explore related products

What You'll Learn

- Bank charges must be tied to a business account, not a personal one

- Bank fees incurred while travelling for work are tax-deductible

- Maintenance fees, ATM charges, and overdraft fees should be itemized separately

- Wire transfer fees, check fees, and service charges are deductible

- Safe deposit box fees used for business purposes are deductible

![]()

Bank charges must be tied to a business account, not a personal one

For sole proprietors, Schedule C is the form used to report income and expenses, and accurate reporting of bank fees is crucial for compliance and minimizing tax liability. While bank fees are typically considered "ordinary and necessary," they are only tax-deductible if they are charged through the normal course of running a business and tied to a business bank account. This means that fees incurred on a personal bank account, even if for business purposes, do not qualify for a deduction.

Entrepreneurs often require a dedicated business bank account, and the fees charged by banks, such as wire transfer fees, check fees, overdraft fees, and service charges, can quickly accumulate. These costs are generally accepted as a standard part of doing business and are thus deductible when filing business tax returns. It is essential to differentiate between business-related and personal transactions, and detailed records, including receipts and bank statements, should be maintained to support these deductions.

In the case of ATM fees, as long as the charges were incurred for business purposes, they can be deducted. For instance, if a business owner regularly withdraws cash to cover business expenses, the associated ATM fees can be included as a deduction. Similarly, if a business owner incurs bank fees while travelling for work, these charges are 100% tax-deductible.

To optimize tax deductions and maintain precise financial records, it is crucial to accurately report and categorize bank fees on Schedule C. These fees should be listed under "Other Expenses" in Part V of the form, with each type of fee itemized separately. Proper reporting ensures compliance with IRS requirements and reduces the risk of audits.

Green Dot's Banking Partners: Who's Behind the Scenes?

You may want to see also

Explore related products

![]()

Bank fees incurred while travelling for work are tax-deductible

Bank fees incurred while travelling for work are indeed tax-deductible. This is assuming, of course, that you are travelling for business purposes and not for personal reasons. It is also important to note that the fees must be charged to a business bank account and not a personal one. Fees charged to a personal account do not qualify for a tax deduction, even if they were for business-related purposes.

Bank fees that occur due to travel are 100% tax-deductible. These fees can include ATM and transaction fees, as well as maintenance fees. For example, if you need to withdraw cash from an ATM to cover business expenses while travelling, the corresponding withdrawal fee can be included as a deduction. It is critical to differentiate between business-related and personal transactions, and detailed records of receipts and bank statements should be maintained to support these deductions.

When reporting these fees, they should be categorised under "Other Expenses" in Part V of Schedule C, with each type of fee itemised separately. Schedule C is the form used by sole proprietors to report income and expenses, and accurate reporting is crucial for compliance and minimising tax liability. Proper reporting also reduces the risk of audits and ensures that all deductions are justified.

It is worth noting that travel expenses must be "ordinary and necessary". This means that they cannot be lavish or extravagant, and they should be incurred during a temporary work assignment, typically lasting less than a year. Examples of ordinary and necessary expenses include transportation, lodging, meals, business calls, and other similar expenses related to business travel.

M&T Bank: A Good Choice for Your Money?

You may want to see also

Explore related products

![]()

Maintenance fees, ATM charges, and overdraft fees should be itemized separately

When it comes to reporting bank fees on Schedule C, it's important to understand that only fees related to a business bank account are tax-deductible. Personal banking fees do not qualify for deductions, even if they were for business purposes. This is a crucial distinction to make.

Now, let's delve into maintenance fees, ATM charges, and overdraft fees, and why they should be itemized separately. Maintenance fees, which are charged for the upkeep of business accounts, are generally deductible as ordinary and necessary expenses. These fees are considered common and essential for running a business. For instance, a monthly fee of $15 for a business account can be deducted on Schedule C. However, it's important to retain bank statements to substantiate these deductions and provide an audit trail.

ATM charges incurred through a business account are also deductible if they are necessary for business operations. For example, if an individual needs to withdraw cash from an ATM to cover business expenses, the associated ATM fee can be included as a deduction. Again, it is critical to differentiate between business-related and personal transactions, and detailed records, such as receipts and bank statements, should be maintained to support these deductions.

Overdraft fees can also be tax-deductible if they are incurred on a business bank account. For instance, if a business owner regularly incurs overdraft fees due to business transactions, these fees can be written off on their Schedule C. However, it is essential to ensure that these fees are directly related to business activities, and having separate business and personal bank accounts can make this distinction clearer.

By itemizing maintenance fees, ATM charges, and overdraft fees separately, business owners can provide a clear financial record to the IRS. This level of detail ensures transparency, aligns with IRS guidelines, and reduces the risk of audits. It also helps to optimize tax deductions and ensures compliance with IRS requirements. Therefore, it is crucial to maintain comprehensive financial records, including bank statements, receipts, and invoices, to support these deductions.

Reconciling Bank Statements: Ensuring Financial Data Accuracy

You may want to see also

Explore related products

![]()

Wire transfer fees, check fees, and service charges are deductible

For most taxpayers, bank fees are not deductible. However, if you operate a business, bank fees can be deductible as ordinary and necessary business expenses. These include fees incurred for maintaining and using your business bank account, such as wire transfer fees, check fees, and service charges.

Wire transfer fees are typically considered a standard operating expense for businesses. These fees are often charged by brokers or financial institutions for initiating a wire transfer, and they can be deducted from the sales proceeds or added to the cost basis, reducing the profits on the sale. It's important to note that wire transfer fees should be reported separately from other expenses to ensure accurate record-keeping and compliance with tax regulations.

Check fees, including charges for check writing, returned checks, and late payments, are also deductible business expenses. These fees are common for business bank accounts and can add up over time, so it's important to keep track of them. Check fees should be categorized and reported accurately to maximize deductions and maintain precise financial records.

Service charges, such as monthly maintenance fees, ATM fees, and overdraft charges, are also deductible business expenses. Maintenance fees are considered necessary expenses for the upkeep of business accounts and are typically reported as "'Other Expenses'" on Schedule C. ATM and transaction fees incurred through a business account are deductible if they are necessary for business operations. Overdraft fees, while less common, may also be deductible if they are directly related to the operation of the business.

To ensure proper deduction of wire transfer fees, check fees, and service charges, it is crucial to maintain separate business and personal bank accounts. This simplifies record-keeping and allows for easier identification of deductible expenses. Additionally, retaining bank statements, receipts, and other relevant documents is essential for providing an audit trail and justifying deductions. By following these guidelines, business owners can maximize their tax deductions and maintain compliance with IRS requirements.

Fifth Third Bank: Is It a Good Choice?

You may want to see also

Explore related products

![]()

Safe deposit box fees used for business purposes are deductible

Safe deposit box fees used for business purposes are generally deductible. The Internal Revenue Service (IRS) requires that deductible expenses be directly related to the production or collection of taxable income. If the box is used to store investment-related documents, such as stock certificates or bonds, the associated fees may qualify as a deduction. However, this only applies if the taxpayer itemizes deductions instead of taking the standard deduction.

It is important to note that the Tax Cuts and Jobs Act (TCJA) of 2017 suspended deductions for miscellaneous itemized expenses subject to the 2% adjusted gross income (AGI) floor through 2025. As a result, safe deposit box fees are typically not deductible unless directly connected to a trade or business. For business purposes, the cost of a safe deposit box may be deductible if it stores business-related assets or documents, such as contracts or proprietary information.

Clear documentation is essential to substantiate business use, and the IRS requires evidence to support any claimed deductions. The distinction between personal and investment use of a safe deposit box is critical for tax purposes. Investment use involves storing items directly tied to generating taxable income, which may qualify for deductions under IRS guidelines. Personal use, such as storing jewelry, family heirlooms, or personal documents, does not qualify for deductions as it lacks a direct connection to income generation.

To optimize tax deductions and ensure compliance with IRS requirements, businesses should maintain detailed financial records, including bank statements, receipts, and invoices. Proper reporting reduces the risk of audits and ensures all deductions are justified.

The Branch Manager: A Bank's Face and Leader

You may want to see also

Frequently asked questions

Bank fees are deductible on Schedule C, but only if they are related to business banking. Personal banking fees do not qualify for deductions.

Some common bank charges that may qualify as deductible business expenses include maintenance fees, ATM fees, overdraft fees, wire transfer fees, and check fees.

Bank fees should be categorized under "Other Expenses" in Part V of Schedule C, with each type of fee itemized separately. For example, maintenance fees, ATM charges, and overdraft fees should be listed with their corresponding amounts. This level of detail ensures transparency and compliance with IRS guidelines.