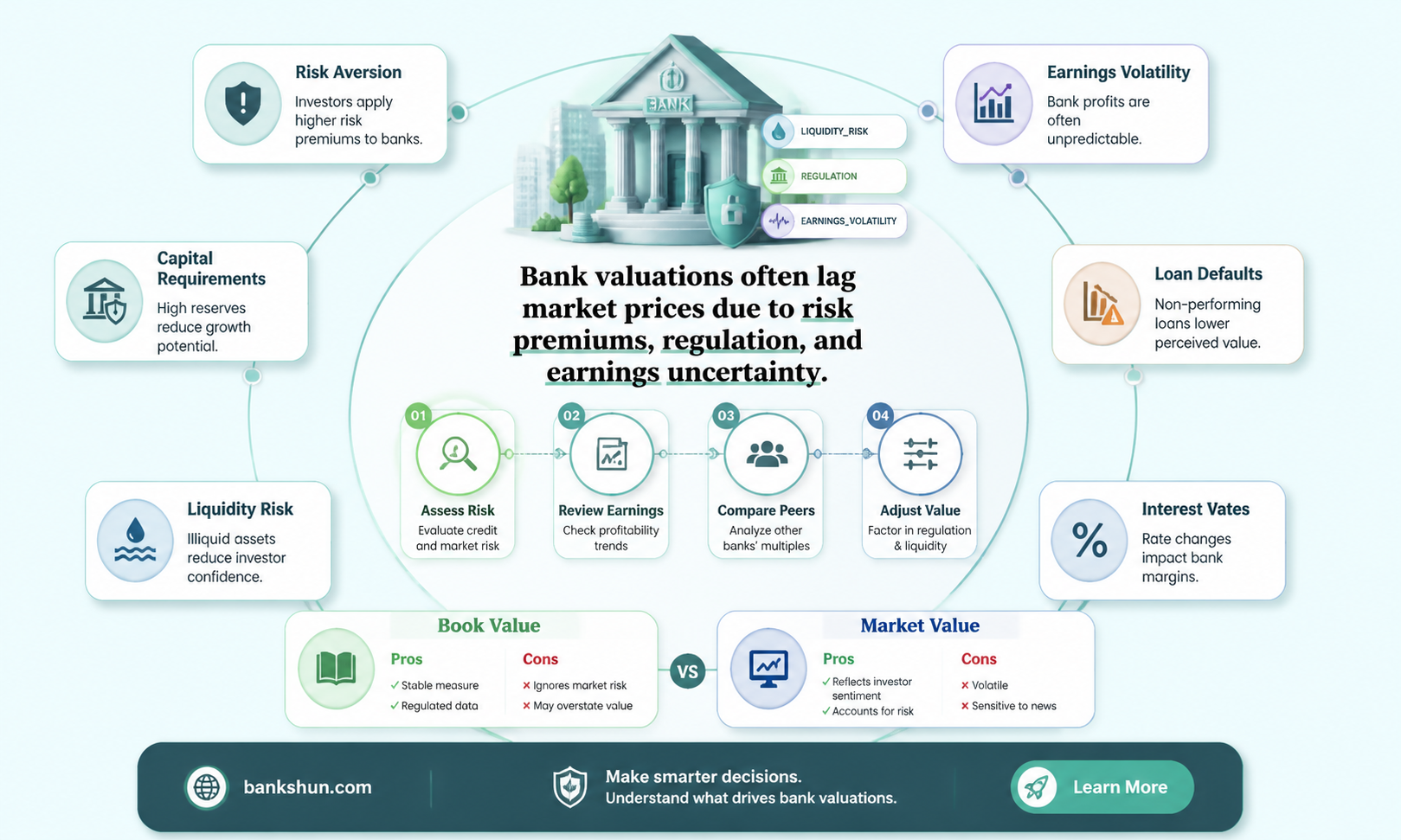

Understanding the difference between bank valuation and market valuation is crucial for property buyers, especially those looking to unlock equity or sell their property. Bank valuations are often lower than market valuations due to their conservative nature, which prioritises minimising risk and relies on historical sales data. Market valuations, on the other hand, are influenced by buyer demand, competitive bidding, and emotions, resulting in higher valuations. This discrepancy can impact buyers' borrowing capacity and refinancing options.

| Characteristics | Values |

|---|---|

| Purpose | Banks: Risk assessment and minimising risk; Market: Reflect current market prices |

| Factors considered | Banks: Physical aspects of property, comparable sales; Market: Value of similar properties in the area, demand, competitive bidding |

| Subjectivity | Banks: Objective; Market: Subjective |

| Timing | Banks: Rely on historical sales data; Market: Consider future values |

| Approach | Banks: Conservative; Market: Driven by buyer demand |

| Outcome | Banks: Lower valuation; Market: Higher valuation |

Explore related products

What You'll Learn

- Bank valuations are conservative estimates, often on the lower end of a property's value

- Market value is influenced by buyer demand and competitive bidding

- Bank valuations are focused on minimising risk for the lender

- Market value is driven by emotion and ego, which can drive up the price

- Bank valuations are based on the condition of the property

![]()

Bank valuations are conservative estimates, often on the lower end of a property's value

Bank valuations are conservative estimates, prioritising the minimisation of risk over reflecting current market prices. They are often on the lower end of a property's value, especially in competitive areas, due to the banks' cautious approach and reliance on historical sales data.

Bank valuations are conducted by lenders to assess property value and manage financial risk. They are not looking to gauge the fair market price but instead focus on recovering the outstanding loan amount in the event of a defaulted sale. This means that bank valuations are typically lower than market valuations, which consider the higher price a buyer would be willing to pay for an investment property.

Market valuations are driven by buyer demand and competitive bidding, resulting in higher prices. In contrast, bank valuations are more objective, lacking the emotional component that can drive up prices in a competitive market. They are based on the physical aspects of the property, such as its condition, and comparable sales data.

The conservative nature of bank valuations can be frustrating for buyers, who may need to increase their deposit or secure additional funding to make up for the valuation shortfall. This is particularly true in high-demand markets, where buyers are willing to stretch their budgets.

Overall, bank valuations are conservative estimates that prioritise financial risk management for the lender. As a result, they often fall on the lower end of a property's value compared to market valuations.

Western Alliance Bank: Mobile App Availability

You may want to see also

Explore related products

![]()

Market value is influenced by buyer demand and competitive bidding

The market value of a property is influenced by buyer demand and competitive bidding. This means that the price a buyer is willing to pay for a property can be driven by their emotions and how much they want it. For example, in an auction setting, buyers can get carried away with the competitive environment and end up paying more than their budget to 'win' the property.

Market value is also influenced by the current sales climate, including the number of buyer and seller enquiries, and how 'hot' or 'cool' the market is. This can be determined by a real estate professional's gut feel and experience.

On the other hand, bank valuations are often lower than market value because they are focused on securing the bank's financial position and minimising risk. They are typically conservative estimates that take into account the physical aspects of the property and comparable sales data to determine the minimum amount the lender could recover on a defaulted sale.

The discrepancy between market value and bank valuation can be frustrating for buyers, who may need to increase their deposit or secure additional funding to make up for the valuation shortfall.

It is important for property buyers to understand the difference between market value and bank valuation to avoid being caught out by a low bank valuation and to make informed decisions when purchasing a property.

UK Interest Rates: Will They Drop?

You may want to see also

Explore related products

$71.18 $90

$89.09 $131

$21.49 $27.95

![]()

Bank valuations are focused on minimising risk for the lender

Bank valuations are often lower than market valuations because they are focused on minimising risk for the lender. The bank valuation is generally on the conservative side, meaning that it is often on the lower end of the value spectrum. This is because banks are not looking to gauge the fair market price, but rather want to ensure they can recover the outstanding loan amount in the event of a loan default.

Market value, on the other hand, uses comparable properties in the area that have recently sold or are currently on the market. It reflects what a buyer might be willing to pay and what a seller would be willing to accept in an open and competitive market. This can be influenced by emotions and the competitive bidding process, which can drive up the price.

Bank valuations, however, are based on the condition of the property and the minimum amount the lender could recover on a defaulted sale. They consider the physical aspects of the property, such as its location and any disrepair, to assess the resale value. This conservative outlook can result in lower valuations compared to what a competitive buyer might pay, especially in high-demand markets.

The cautious approach taken by banks helps protect them from potential losses. They are more focused on the potential resale value than on the property's appeal or current demand. This can create the perception of inaccuracy when compared to market valuations, as bank valuations may not always reflect the current market environment.

Overall, bank valuations are designed to secure the bank's financial position by minimising risk. This can result in lower valuations that prioritise recovering loan amounts over estimating fair market prices.

Relationship Managers: Banking's Key to Customer Success

You may want to see also

Explore related products

$45.78 $100

$68.33 $105

![]()

Market value is driven by emotion and ego, which can drive up the price

The concept of property valuation can be confusing for buyers, as a property can have two different values: a bank valuation and a market valuation. A bank valuation is typically conservative and is often on the lower end of the value spectrum. This is because it is based on the physical aspects of the property and the minimum amount the lender could recover if the loan defaulted. On the other hand, a market valuation uses data from the sale of similar properties in the area to establish a reasonable value. The buyer and seller can then negotiate a price based on this value.

Emotions can also drive market behaviour in other ways. For instance, investors may assume that a company's recent strong performance is an indication of future performance and start bidding for shares, driving up the price. This can lead to a situation where the market deviates from its underlying fundamentals, and investors, driven by emotion, can lead markets astray. However, it is important to note that while emotions can play a role in market behaviour, they are typically short-lived, and fundamentals still rule in the long run.

Furthermore, ego can also play a role in pricing decisions. For example, a business leader may "fall in love" with their product and assign a higher value to it than is justified. This can also occur with homeowners who may cite a list of features to justify a higher selling price, even if buyers are oblivious to these features. Overall, while market value is driven by emotion and ego, which can drive up the price, it is important to approach pricing decisions with a balance of rational analysis and an understanding of customer motivations.

Capital One: Physical Branches or Online-Only?

You may want to see also

Explore related products

![]()

Bank valuations are based on the condition of the property

Bank valuations are often lower than market valuations, and this is mainly due to the fact that they are based on the condition of the property. Banks are conservative in their valuations as they aim to minimise risk and secure their financial position. They are not looking to gauge the fair market price but rather ensure they can recover the outstanding loan amount in case of a defaulted sale. This means that a bank valuation may be accurate within its intended purpose but may not always reflect what a buyer would pay in the current market environment.

A bank valuation is based on the physical aspects of the property, and a valuer will assess the property 'as is'. If there is a minor state of disrepair or low-quality presentation, this will be factored into the assessment. The bank valuation will also consider comparable sales, but the methodology used tends to be stricter than that of independent valuers, and they rely on historical sales data rather than speculative future values.

The bank's conservative approach can result in lower valuations compared to what a competitive buyer might pay, especially in high-demand markets where buyers are willing to stretch their budgets. This can be frustrating for buyers, who may then need to increase their deposit or secure additional funding as banks will only lend a percentage of the bank valuation, not the market value.

The difference between bank and market valuations can be confusing for property buyers. A market valuation uses data from the sale of similar properties in the area to establish a reasonable value, which the buyer and seller can then use as a foundation to negotiate a price. Market valuations are driven by buyer demand and competitive bidding, and there is more subjectivity and emotion attached.

In summary, bank valuations are based on the condition of the property, and this, along with the bank's conservative approach to minimise risk, contributes to their often lower valuation compared to market value.

Are Bank Windows and Doors Bulletproof?

You may want to see also

Frequently asked questions

Bank valuations are often conservative estimates, focusing on minimising risk for the lender and ensuring they can recover the outstanding loan amount. Market valuations, on the other hand, are driven by buyer demand and competitive bidding, which can drive up the price.

Various factors are considered in a bank's valuation, including the property's physical condition, location, recent sales data of comparable properties, and broader economic conditions.

A low bank valuation may affect a buyer's borrowing capacity, requiring additional funds or a larger deposit. It may also limit homeowners' ability to refinance and access equity.

If the bank valuation is lower than expected, buyers can consider ordering another valuation from a different organisation or local valuation firm. They may also need to increase their deposit or secure additional funding. In some cases, finding an alternative lender may be an option.