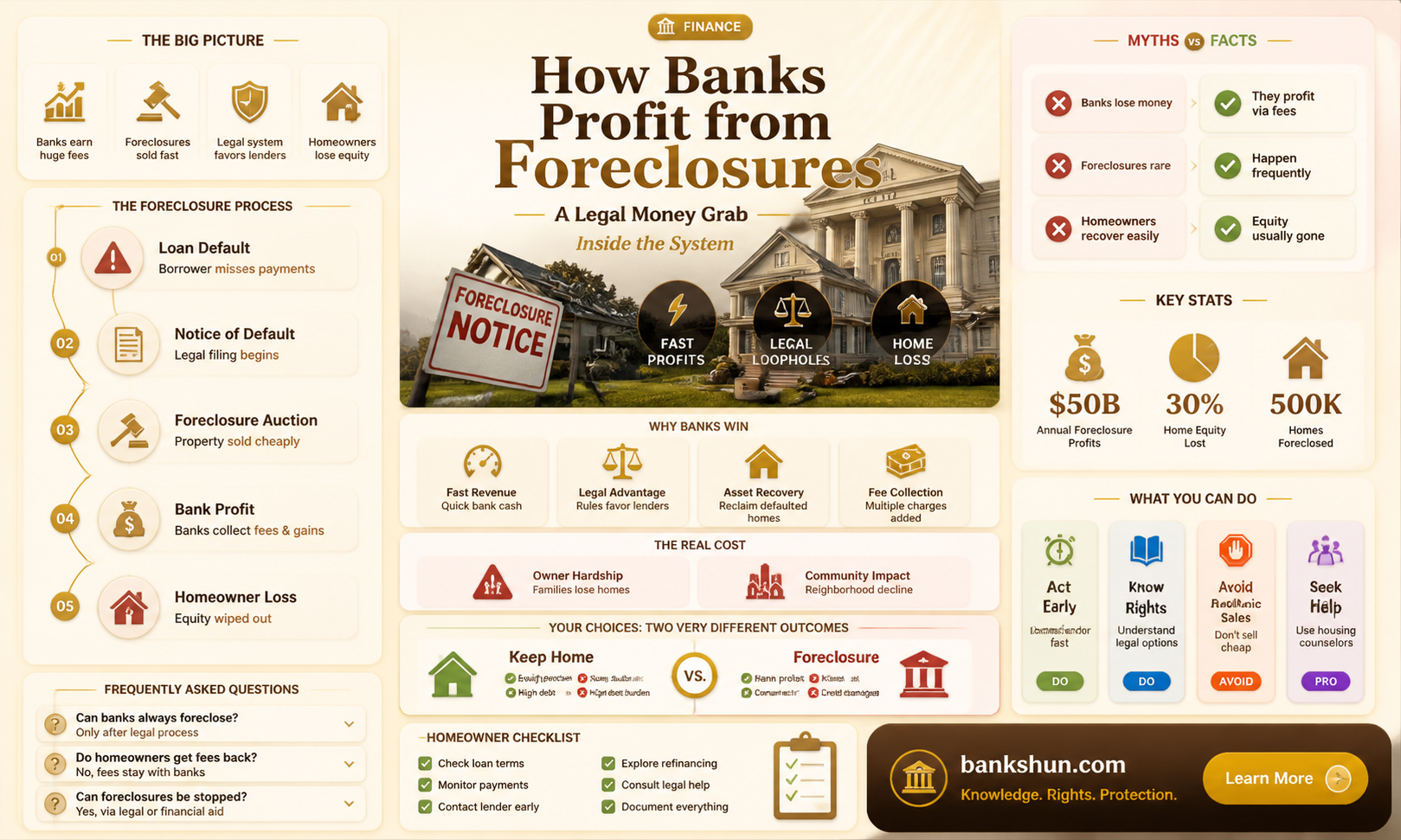

Banks can profit from foreclosure, but it is not always the case. When a homeowner defaults on their mortgage payments, banks as mortgage lenders start the foreclosure process to recover the loan balance that has not been paid back. The bank will hire agents to assess the property during the foreclosure process and calculate its worth as-is and after repairs. The bank then uses these calculations to decide whether to sell the property as-is or fix it up to increase its value. The bank's goal is to recoup its losses and make a profit, but the process is long and expensive, and the property's condition and market conditions may result in low prices that do not cover the original mortgage. In some states, banks may not be able to sell a property for more than its mortgage, and they may favour a short sale if it is close to market value.

| Characteristics | Values |

|---|---|

| Banks' goal of selling a foreclosed property | To recoup their costs as quickly as possible |

| Bank's pricing strategy | Property's condition, market conditions, and whether to sell as-is or fix up the property |

| Profitability | Banks can profit from foreclosures, but there are risks and transaction costs involved |

| Regulatory standpoint | Banks cannot profit from loans that go bad as it is not their core business |

| Tax implications | Losses on foreclosures are allowed as deductions from taxable income |

| Short sales vs. foreclosures | Banks generally lose less money on short sales, but may favor foreclosure if the real estate market is appreciating |

Explore related products

What You'll Learn

![]()

Banks' primary goal is to recoup losses

When a mortgage borrower fails to pay their dues, the bank as the mortgage lender starts the foreclosure process. This involves notifying the borrower, filing a lawsuit, and possessing the property if the borrower fails to pay. The bank will then hire one or two agents to assess the property during the foreclosure process. These agents calculate the property's worth as-is, its value after repairs, and the cost of those repairs.

The bank uses these calculations to find the best way to recoup its losses. While many foreclosed properties are sold as-is, the bank may decide to fix up the home if it will result in a higher profit. The bank's goal is to recoup its costs as quickly as possible, so they are often willing to reduce the asking price. If the bank nets more than enough to cover their costs, the profits might be sent back to the original owner, although this is rare.

In some cases, foreclosure may result in profit for the bank, especially if the property is sold at a higher price than the total outstanding loan amount. However, there are also risks involved, and conditions or market circumstances often result in low prices on foreclosed properties. The bank must also factor in costs such as legal fees, property taxes, maintenance, and administrative charges.

Overall, while banks may sometimes profit from foreclosures, their primary goal is to recoup their losses and recover unpaid loan balances.

Netspend: A Bank by Any Other Name

You may want to see also

Explore related products

$12.95

![]()

Foreclosure pricing factors

When pricing a foreclosure, banks consider several factors. The bank's primary goal is to recoup its losses, and it will use different strategies to do so. Firstly, the bank will hire agents to assess the property and calculate its worth as-is, as well as its potential worth after repairs, including the cost of those repairs.

The bank then decides whether to sell the property as-is or invest in renovations to sell it for a higher profit. This decision is influenced by the property's condition and the state of the market. If the bank is dealing with multiple foreclosed properties, they may be more inclined to sell the property as-is to recoup their losses quickly.

The bank's pricing strategy also depends on the feedback they receive from potential buyers. If the property is receiving interest but no offers, the bank may lower the asking price to compensate for any disadvantages, such as being located on a busy street.

The type of foreclosure also affects pricing. Judicial foreclosures, which involve court proceedings, tend to be more expensive due to additional legal and court fees. Non-judicial foreclosures, on the other hand, are generally faster and less costly for homeowners, although they may still incur fees for foreclosure trustees, notices, and auction costs.

It's worth noting that foreclosure costs can be substantial for all parties involved, including lenders, homeowners, neighbours, and local governments. Homeowners may face late fees, legal expenses, property inspections, and auction costs, amounting to thousands of dollars. Lenders also incur costs such as legal fees, marketing fees, and home maintenance.

Overall, the pricing of foreclosures is a complex process that involves assessing the property's condition, market trends, and the costs and fees associated with the foreclosure process.

The Emergency Banking Act: A Presidential Authorization

You may want to see also

Explore related products

![Profit - The Complete Series [DVD]](https://m.media-amazon.com/images/I/71KkinijN1L._AC_UY218_.jpg)

![Profit - 3-DVD Set ( Jim Profit ) [ NON-USA FORMAT, PAL, Reg.2 Import - Germany ]](https://m.media-amazon.com/images/I/61wYcjWLT6L._AC_UY218_.jpg)

![]()

Banks' profit-making strategies

Banks employ various strategies to profit from foreclosures while navigating associated risks and complexities. Here are some common strategies used by banks to make a profit from foreclosures:

Property Assessment and Pricing

When a bank acquires a property through foreclosure, they hire agents to assess the property's condition and calculate its worth. These agents determine the property's value as-is and its potential value after repairs, along with the estimated repair costs. Banks then use these calculations to decide whether to sell the property as-is or invest in renovations to increase its value and profit potential. The property's location and market conditions also play a role in pricing decisions.

Recouping Losses and Costs

The primary goal of banks in selling foreclosed properties is to recoup their losses and associated costs, such as lawyer fees and maintenance expenses. Banks aim to recover these amounts as quickly as possible, often leading them to reduce the asking price over time. They may also build a certain amount of loss into their financial projections, considering the original loan amount as an afterthought.

Effective Marketing and Outreach

To attract potential buyers and sell foreclosed properties more quickly, banks can benefit from effective marketing strategies. Utilizing various channels, such as online listing services, and engaging the services of real estate agents can help reach a wider audience. Thorough property appraisals are also essential to determine competitive prices, making the offering more attractive to buyers.

Tax Implications and Deductions

Banks can work with tax professionals to navigate the tax implications of foreclosure properties. By treating certain expenses as deductible, banks can claim deductions on their taxes and reduce the overall tax impact of maintaining and disposing of these properties. Proper tax handling ensures compliance and good financial management.

Long-Term Profit Strategies

In some cases, banks may choose to hold onto a foreclosed property and pay for necessary repairs to increase its value over time. This strategy involves a longer timeline but can result in a more significant profit for the bank. Additionally, in rare cases where the bank's profits exceed their costs and associated fees, the surplus may be returned to the original owner, depending on the state's regulations.

Huntington Bank Branches: Florida Locations

You may want to see also

Explore related products

![]()

Regulatory and legal considerations

Banks are subject to various regulatory and legal considerations when dealing with foreclosed properties. One important consideration is the distinction between making risky loans and intentionally making loans that are expected to default for the purpose of profiting from the collection process. This distinction is crucial from a regulatory standpoint, as it can significantly impact the bank's reputation and expose it to legal risks.

Additionally, banks must navigate the complex dynamics of the secondary market, where securitization plays a significant role. Securitization involves packaging multiple loans together and selling them as a single product in the secondary market, often to trusts composed of investors. This process allows companies that acquire bad debt to purchase it at a substantial discount and aim for a higher collection amount. However, it is essential for banks to carefully evaluate the risks associated with such transactions and ensure compliance with regulatory requirements.

The involvement of service providers, such as those facilitating loan modifications or short sales, introduces additional regulatory considerations. Service providers often have differing incentives and preferences, as they are primarily focused on their compensation. For example, they may favour short sales over loan modifications because they receive higher compensation and are not burdened with the property in the case of a short sale. Understanding the role and motivations of service providers is crucial for banks to ensure compliance with regulatory frameworks and avoid conflicts of interest.

Furthermore, banks must be cautious when dealing with properties that have multiple mortgages. In such cases, the main objective of the bank is often to retake the property from the second mortgage holder to recover unpaid loan balances. This process can be complex and may involve legal proceedings, including filing lawsuits and possessing the property. Proper management of these legal considerations is essential to protect the bank's interests and ensure compliance with applicable laws.

Lastly, banks can benefit from understanding the tax implications of foreclosures. In some cases, financial losses incurred during the foreclosure process, such as carrying costs, marketing expenses, and sale costs, may be treated as deductible expenses. By engaging tax professionals, banks can navigate the intricacies of tax regulations and minimise their tax liabilities. Proper accounting and documentation of these losses are crucial to take advantage of applicable deductions and optimise their financial position.

Tyra Banks: Nose Job or Natural Beauty?

You may want to see also

![]()

Risks and rewards of foreclosure

Banks are profit-seeking businesses, and like any business, they aim to earn a profit. Foreclosure may result in profit for banks, but there are various risks involved. The main aim of banks by filing foreclosure notices is to retake property from the second mortgage holder that is securing a mortgage so they can sell it and recover unpaid loan balances.

Risks of Foreclosure

The foreclosure process is long and expensive. It involves multiple costs, including legal fees, property taxes, maintenance, administrative charges, and carrying costs. The bank also has to pay for the marketing and sale of the property. If the property is sold for less than the remaining loan balance, the bank suffers a financial loss. In some states, banks may not be able to sell a property for more than its mortgage. If the short sale price is close to the market value, the bank may favour a short sale over foreclosure to avoid losses.

Rewards of Foreclosure

Banks can profit from foreclosure if the property is sold at a higher price than the total outstanding loan amount. They may also profit by fixing up the property and selling it for a higher price. If the bank receives an offer close to the market value, it may accept the offer instead of foreclosing. Properly managed foreclosures can minimize losses and provide an opportunity for banks to earn profits.

While foreclosure may result in profits for banks, there are also risks and costs involved. Banks must carefully consider the property's condition, the market, and the potential for profit when deciding whether to foreclose or sell a property.

Free Coin-Counting Services: Banks Offering This Perk

You may want to see also

Frequently asked questions

Yes, banks are allowed to profit from foreclosure. However, the main aim of banks by filing foreclosure notices is to retake property from the second mortgage holder that is securing a mortgage so they can sell it to recover unpaid loan balances.

Banks hire agents to assess the property during the foreclosure process. These agents calculate the property's value as-is, its value after repairs, and the cost of repairs. Banks then use these calculations to decide whether to sell the property as-is or to make repairs and sell it for a higher profit.

The foreclosure process is long and expensive, involving legal fees, property taxes, maintenance, and administrative charges. In some cases, banks may suffer financial losses if the amount received from selling the property is less than the remaining loan balance.