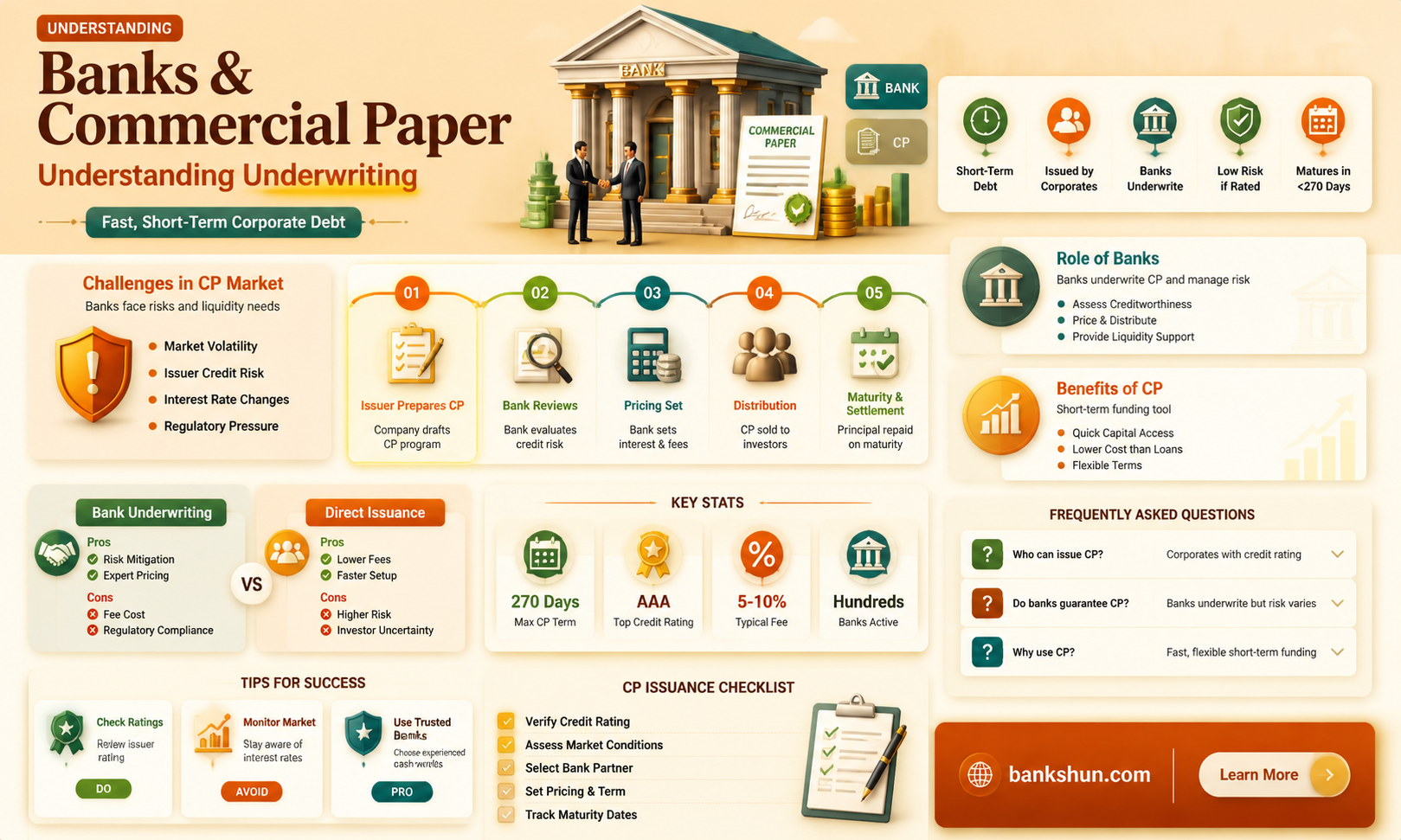

Commercial paper is a short-term money market funding instrument issued by corporates. It is a form of unsecured promissory note that pays a fixed rate of interest. The main issuers of commercial paper are finance companies and banks, but also include corporations with strong credit. The role of banks is to act as agents for the issuing corporations, but they are not obligated for the repayment of commercial paper. In the past, there has been debate about whether banks are allowed to underwrite commercial paper, as it is not classified as a bond by the SEC.

| Characteristics | Values |

|---|---|

| Commercial paper | A short-term US promissory note with a maturity not exceeding 270 days |

| Issuers | Finance companies, banks, and corporations with excellent credit |

| Underwriters | Investment banks |

| Underwriting by commercial banks | Prohibited by the Glass-Steagall Act; allowed by the Federal Reserve in 1987 for subsidiaries of bank holding companies |

| Role of banks | Act as agents for the issuing corporations, but are not obligated for the repayment of commercial paper |

Explore related products

What You'll Learn

![]()

Banks acting as underwriters

Banks are allowed to underwrite commercial paper. Commercial paper is an unsecured form of promissory note that pays a fixed rate of interest. It is typically issued by large banks or corporations to cover short-term receivables and meet short-term financial obligations. The main issuers of commercial paper are finance companies and banks, but also include corporations with strong credit.

Commercial paper was first introduced when New York merchants began to sell their short-term obligations to dealers, who acted as intermediaries. These dealers would purchase the notes at a discount from their par value and then pass them on to banks or other investors. The borrower would then repay the investor an amount equal to the par value of the note.

In the financial primary market, securities underwriting is the process by which investment banks raise investment capital from buyers on behalf of corporations and governments by issuing securities (such as stocks or bonds). As an underwriter, the investment bank guarantees a price for these securities, facilitates the issuance of the securities, and then sells them to the public. Underwriters make their profit from the price difference (called "underwriting spread") between the price they pay the issuer and what they collect from buyers or broker-dealers.

Underwriting services are provided by some large financial institutions, such as banks, insurance companies, and investment houses. Underwriters help establish the true market price of risk by deciding on a case-by-case basis which transactions they are willing to cover and what rates they need to charge to make a profit. They also handle sales activities and contribute to their success.

Washington Mutual Bank: Still Operational?

You may want to see also

Explore related products

$39.61 $65

$301

![]()

The Glass-Steagall Act

Commercial paper is an unsecured form of promissory note that pays a fixed rate of interest. It is typically issued by large banks or corporations to cover short-term receivables and meet short-term financial obligations. Commercial paper is usually issued and traded among institutions in denominations of $100,000. The main buyers are other corporations, insurance companies, commercial banks, and mutual funds.

Commercial bank entry into securities underwriting can affect underwriter behaviour because, unlike investment houses, banks also lend to firms. Commercial banks were prohibited from underwriting commercial paper by the Glass-Steagall Act. The Act was passed in 1933 and separated investment and commercial banking activities. It forced commercial banks to refrain from investment banking activities to protect depositors from potential losses through stock speculation.

Retirement Savings: Are 401(k)s Safe in a Bank Failure?

You may want to see also

Explore related products

$119.98 $51

![]()

Commercial paper's role in the money market

Commercial paper is a short-term, unsecured debt instrument issued by large banks, corporations, and other financial institutions. It is used to raise capital for short-term needs, such as payroll, accounts payable, and inventories. Commercial paper is typically issued at a discount and has maturities of 270 days or less, with most issues maturing in one to six months. The main issuers of commercial paper are finance companies and banks, but the list of issuers also includes corporations with strong credit, foreign corporations, and sovereign issuers.

Commercial paper is a convenient financing method for issuers as it allows them to avoid the costs and hurdles of applying for and securing continuous business loans. It is also not required to be registered with the Securities and Exchange Commission (SEC) when traded in the money market. Commercial paper is usually sold in denominations of $100,000 or more, making it inaccessible to most retail investors. The main buyers are institutional investors, including mutual funds, banks, insurance companies, pension funds, and wealthy individuals.

Commercial paper is an attractive investment option for money market funds as it fits well within their investment strategies that emphasize safety and liquidity. It is also a preferred choice for corporate treasurers due to its short maturity and low risk. Companies often invest their excess capital in commercial paper to generate revenue without taking on substantial risk.

In the 21st century, commercial paper has become the chief source of short-term financing for investment-grade issuers, along with commercial loans. It is widely used in the credit card industry, where credit card issuers provide cardholder facilities and services to merchants using funds generated from commercial paper. The issuers then purchase the receivables placed on the cards by customers from these merchants, profiting from the spread.

Replacing O2 Sensor Bank 1: Step-by-Step Guide

You may want to see also

Explore related products

![]()

The role of investment banks

Commercial paper is an unsecured form of promissory note that pays a fixed rate of interest. It is typically issued by large banks or corporations to cover short-term receivables and meet short-term financial obligations. The main issuers of commercial paper are finance companies and banks, but also include corporations with strong credit.

Commercial banks were prohibited from underwriting commercial paper by the Glass-Steagall Act. However, in June 1987, the Federal Reserve allowed subsidiaries of bank holding companies to underwrite commercial paper.

The primary function of investment banks is to help their clients raise equity capital. This is often done through initial public offerings (IPOs) and the underwriting of stocks or bonds. Investment banks facilitate the trading of securities by buying and selling them out of their own accounts, profiting from the spread between the bid and ask prices.

When a company wants to issue new bonds to fund a new project, it hires an investment bank. The investment bank then determines the value and risk of the business to price, underwrite, and sell the new bonds. Investment banks also underwrite other securities through an IPO or any subsequent secondary public offering.

Underwriting is a complex activity that requires a lot of financial skill and acumen to predict the future performance of an issue. Investment bankers often take significant risks when they decide to underwrite any public issue, so they consider several important factors, including market timing and public opinion.

M&T Bank: Foreign Currency Exchange Services

You may want to see also

Explore related products

![]()

The impact of bank entry into securities underwriting

Commercial banks were prohibited from underwriting commercial paper by the Glass-Steagall Act. However, in June 1987, the Federal Reserve allowed subsidiaries of bank holding companies to underwrite commercial paper. This raised several questions about the impact of bank entry into securities underwriting.

Firstly, it was questioned whether banks, with their superior information about firms, would monopolize the market. However, research suggests that bank entry into the corporate debt underwriting market has lowered market concentration and had a pro-competitive effect in reducing underwriter spreads, yield spreads, and market concentration.

Secondly, the impact of bank entry on the competitive structure of the market was questioned. There were concerns that banks could secure better prices for firms through their underwriting activities, but evidence suggests that any differences in underwriter spreads on bank versus investment house underwritings have not persisted over time.

Thirdly, the impact of bank entry on ex-ante yield spreads of corporate bond issues was considered. Section 20 deregulation resulted in a significant decline in underwriting spreads in the corporate bond market, but similar declines were not seen in equity markets.

Finally, the question of whether banks are better certifiers of firms' securities than investment houses was raised. Banks, as lenders to firms, can be better certifiers than investment houses, but equity holding can hinder their certification ability. Overall, the evidence suggests that bank entry into securities underwriting has had a pro-competitive effect and that banks and investment houses can coexist in the market.

The Federal Reserve: Private Bank or Government Entity?

You may want to see also

Frequently asked questions

Banks are allowed to underwrite commercial paper. Commercial paper is a short-term money market funding instrument issued by corporates, and banks act as agents for the issuing corporations.

Commercial paper is an unsecured form of promissory note that pays a fixed rate of interest. It is typically issued by large banks or corporations to cover short-term receivables and meet short-term financial obligations.

Banks act as agents for the issuing corporations in commercial paper transactions, but they are not obligated for the repayment of the commercial paper. They facilitate the trading of securities by buying and selling them out of their own accounts and profiting from the spread between the bid and ask price.