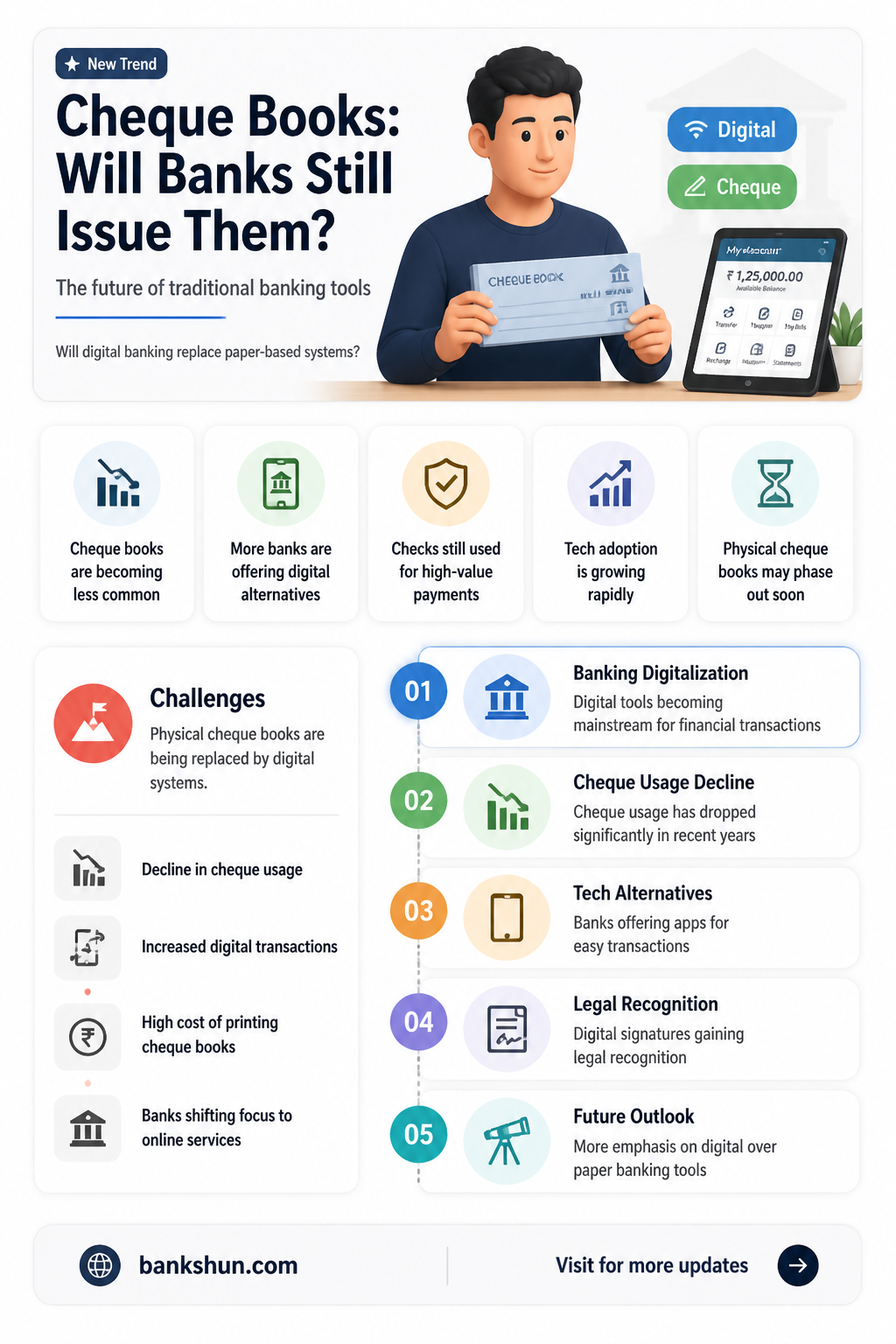

While some banks have already stopped issuing cheque books, there is no indication that banks will completely stop issuing cheque books. In 2011, the Payments Council, an industry body independent of the government, decided to continue providing customers with cheques for as long as they are needed. In Singapore, the Association of Banks (ABS) has announced a timeline to eliminate corporate cheques by the end of 2025, but individual cheque users will still be able to use cheques beyond this date. The decline in cheque usage is due to the increasing popularity of faster and more convenient digital payment methods.

| Characteristics | Values |

|---|---|

| Banks that have stopped issuing cheque books | Citibank, DBS Bank, HSBC, Maybank, OCBC Singapore, Standard Chartered Bank, UOB, and one unknown bank |

| Reasons for stopping | The average cost of clearing a cheque has increased, and banks will no longer be able to absorb these costs |

| Alternatives | Banks are encouraging customers to switch to digital payments, such as PayNow, FAST, GIRO, and MEPS+ |

| Country-specific initiatives | Singapore has announced an end-2025 timeline to eliminate corporate cheques |

| Future of cheques | The Payments Council in the UK has decided that cheques will continue for as long as they are needed |

Explore related products

What You'll Learn

- Banks in Singapore are eliminating corporate cheques by the end of 2025

- The UK Payments Council decided cheques will continue for as long as they are needed

- Banks will no longer be able to absorb the costs of cheque processing by 2025

- Customers can request a new chequebook online or by visiting a branch

- Some banks have discontinued cheques, but customers can still pay in cheques

![]()

Banks in Singapore are eliminating corporate cheques by the end of 2025

Banks in Singapore are set to stop issuing cheque books to corporates by the end of 2025. The Monetary Authority of Singapore (MAS) has announced that all centrally cleared cheques issued by corporates will be eliminated by the end of 2025. This decision comes as a response to the decreasing usage of cheques and the increasing cost of processing them. The cost of clearing a cheque is expected to rise to between S$2 and S$6 if cheque volumes fall by 70% by 2025. Banks will no longer be able to absorb these costs and will have to pass them on to their customers.

To facilitate the transition to zero corporate cheques, the Association of Banks in Singapore (ABS) will work with Domestic Systemically Important Banks (D-SIBs) to develop an electronic deferred payment (EDP) solution. This solution will enable users to make deferred payments or issue cashiers' orders without the need for cheques. The EDP solution will leverage existing payment solutions like PayNow and GIRO and is expected to be ready by 2025.

In the meantime, banks will be reaching out to customers who have not yet transitioned to digital payments to address their concerns. MAS will also conduct a second public consultation in 2024 to set out initiatives and timelines for eliminating individual cheques and terminating the cheque truncation system (CTS). While individual cheque users will still be able to use cheques beyond 2025, MAS encourages all cheque users to switch to alternative payment methods as the industry prepares for the retirement of CTS.

The decision to eliminate corporate cheques by the end of 2025 is part of Singapore's Smart Nation vision, which aims to provide fast, simple, and secure payments for everyone. By eliminating corporate cheques, Singapore's financial system will become more efficient and cost-effective.

Federal Regional Banks: How Many Are There?

You may want to see also

Explore related products

![]()

The UK Payments Council decided cheques will continue for as long as they are needed

In 2009, the UK Payments Council announced that cheques would be phased out by October 2018, but only if alternatives were developed. The Council's decision to set a proposed abolition date was intended to encourage the development of other forms of payment. However, in 2011, the Payments Council reversed its decision and announced that cheques will continue to be issued for as long as customers need them.

The Payments Council is an independent industry body that was created in 2007 to set the strategy for payments in the UK, including cheques. Its members include financial institutions, technology firms, and payment processing companies. The Council's role is to provide direction and ensure that payment systems are fit for the 21st century. While the use of cheques has been declining in the UK, with businesses and consumers opting for alternative payment methods such as cards and remote banking transfers, the Payments Council recognised the continued value of cheques for those who prefer to use them. Cheques provide a convenient and secure method of payment when the recipient's bank account details are unknown.

The decision to continue issuing cheques was reinforced by the introduction of the Image Clearing System (ICS) by the Cheque and Credit Clearing Company in 2017, which accelerated the cheque clearing process. This improvement addressed one of the challenges associated with cheque payments. Additionally, the Payments Council has committed to enhancing other payment methods to provide customers with a range of efficient and secure options.

While the UK Payments Council initially targeted 2018 for the closure of the cheque clearing system, it ultimately decided to prioritise the needs of its customers. By choosing to retain cheques indefinitely, the Council demonstrated its responsiveness to feedback from the government and the public. This decision ensured that individuals and organisations could continue utilising cheques as a familiar and trusted payment method, particularly when other payment alternatives were not feasible or preferred.

Truist Bank Headquarters: Where is it Located?

You may want to see also

Explore related products

![]()

Banks will no longer be able to absorb the costs of cheque processing by 2025

The Monetary Authority of Singapore (MAS) has announced that all corporate cheques will be phased out by the end of 2025. This decision comes as cheque usage in Singapore continues to decline, resulting in rising costs for banks to process each cheque. MAS has stated that banks will need to start charging for cheque processing to recover these costs.

Historically, banks have been able to subsidize the cost of cheque processing. However, with a projected further decrease in cheque usage by 2025, the cost of clearing a cheque is expected to increase significantly, reaching between S$2.00 and S$6.00. As a result, banks will no longer be able to absorb these costs and will have to pass them on to their customers.

To facilitate the transition away from cheques, MAS is working closely with the Association of Banks in Singapore (ABS) and the financial industry to promote the use of e-payment solutions. This includes the development of an electronic deferred payment (EDP) solution, leveraging existing payment platforms such as PayNow and GIRO. The EDP solution will enable users to make deferred payments or issue cashiers' orders without relying on cheques.

While the focus is currently on eliminating corporate cheques by the end of 2025, MAS recognizes that individual cheque users will need more time to transition to alternative payment methods. As such, individuals will still be able to use cheques for a period beyond 2025. MAS plans to conduct further consultations to determine the timeline for phasing out individual cheques and terminating the cheque truncation system (CTS) entirely.

To summarize, the increasing costs of cheque processing due to declining usage have made it unsustainable for banks to continue absorbing these costs. By the end of 2025, banks will start reflecting these costs in their charges, and alternative electronic payment methods will be promoted to facilitate a smooth transition away from cheques.

Food Banks: Community Support and Beyond

You may want to see also

Explore related products

![]()

Customers can request a new chequebook online or by visiting a branch

Alternatively, customers can request a chequebook by visiting a branch. For instance, ICICI Bank customers can visit any branch to request a chequebook. Similarly, NatWest customers can order a chequebook at a branch or at an ATM.

In addition to online and in-person methods, some banks offer other options for requesting a chequebook. For example, ICICI Bank customers can request a chequebook over the phone by calling customer care. NatWest customers can also place their order using a digital stationery order form.

Regardless of the method used, customers will typically receive their chequebook by mail or can pick it up at a branch within a few business days.

Understanding APY: Maximizing Your Banking Returns

You may want to see also

Explore related products

![]()

Some banks have discontinued cheques, but customers can still pay in cheques

While some banks have discontinued the use of cheques, customers can still pay them into their accounts. For example, in 2017, one UK bank discontinued cheques, but customers could still pay in cheques from other banks. Banks that continue to issue cheques often do so through online or in-branch requests. Some banks automatically send new chequebooks when a customer's current book is close to running out.

The shift away from cheques towards digital payments has been ongoing for several years. In 2011, the UK Payments Council announced that cheques would continue indefinitely but encouraged innovation in new and existing payment methods. More recently, in 2023, Singapore's Payments Council proposed a roadmap to eliminate corporate cheques by the end of 2025. This proposal received support from the financial services sector and business communities.

The decline in cheque usage is evident in Singapore, where the share of cheque transaction volume as a proportion of payments using FAST, Inter-bank GIRO, and cheques fell from 32% in 2016 to 4% in 2022. The average cost of clearing a cheque has also quadrupled since 2016, with banks absorbing these costs. However, if cheque volumes fall by 70% by 2025, the cost of clearing a cheque is projected to increase to between $2.00 and $6.00, which banks will no longer be able to absorb.

Despite the push towards digital payments, some individuals and businesses still rely on cheques for transactions. In Singapore, individual cheque users will still be able to use cheques beyond 2025, and banks will assist these customers in transitioning to alternative payment methods. Similarly, in the UK, the Payments Council has committed to providing customers with cheques for as long as they are needed.

Social Security and Death: Banks Notified?

You may want to see also

Frequently asked questions

There is no universal answer to this question. While some banks have discontinued issuing cheque books, others continue to provide this service. The decision to stop issuing cheques may be influenced by the declining usage of cheques and the increasing preference for faster digital payment methods.

Banks are transitioning to digital payment methods due to the decreasing usage of cheques. This shift aims to streamline payment processes and reduce the costs associated with cheque processing, which have been subsidised by banks.

There are several alternative payment methods available, such as online banking, card payments, and digital payment platforms like PayNow, FAST, GIRO, and MEPS+. These methods offer faster and more secure ways to transfer funds.

Cheques provide a written record of transactions, which can be useful for tracking and budgeting purposes. They can also be used for payments to individuals or organisations that do not accept digital payments or require a guaranteed payment method.

You can request a cheque book from your bank by ordering through their website or online banking platform, or by visiting a local branch. Some banks may automatically send a new cheque book when the current one is close to running out.