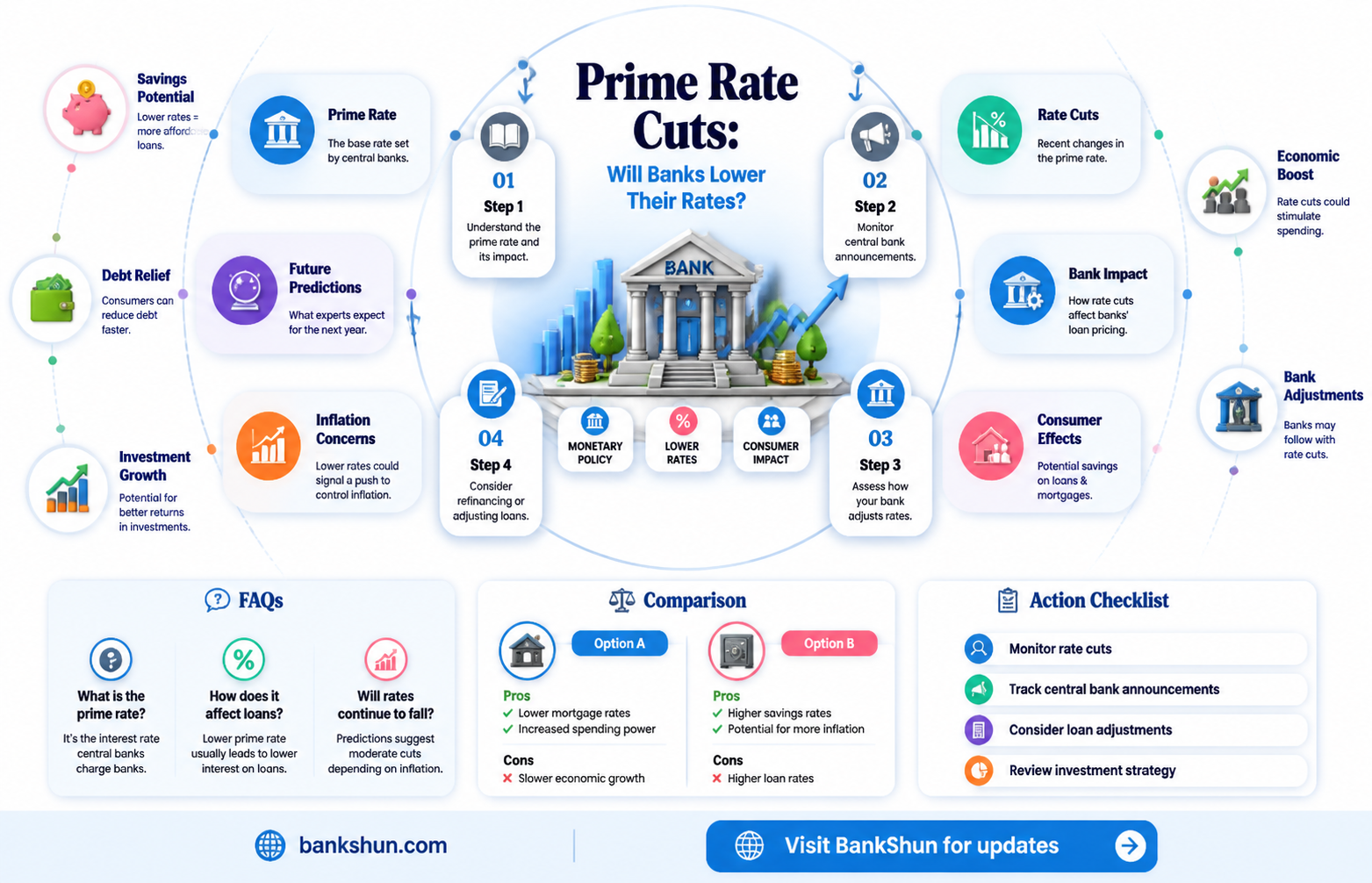

The prime rate is the interest rate that commercial banks charge their most creditworthy borrowers. It is used as a baseline that most banks use to determine the interest rate for customers who want to open a new credit card or take out a loan. The prime rate is determined by individual banks and can change depending on economic conditions. For example, during a recession, prime rates are generally lower. When the Federal Reserve lowers the federal funds rate, banks typically lower their prime rates by the same amount. On the other hand, when the Federal Reserve raises rates, banks usually follow suit. While the future direction of prime rates is uncertain, banks will lower their prime rates if the Federal Reserve continues to cut rates.

| Characteristics | Values |

|---|---|

| Prime Rate Determination | Each bank sets its own prime rate, but it is influenced by the federal funds rate, the interest rate set by the Federal Reserve that banks use to borrow from one another. |

| Prime Rate Usage | The prime rate is used as a baseline interest rate for various loans and lines of credit, including mortgages, small business loans, and credit cards. |

| Prime Rate Impact | A change in the prime rate can affect monthly payments for variable-rate loans, such as adjustable-rate mortgages, and influence investment portfolio performance and auto loan rates. |

| Prime Rate Adjustment | Banks adjust their prime rates based on economic conditions, business cycle shifts, and changes in the federal funds rate set by the Federal Reserve. |

| Recent Prime Rate Changes | In 2024, three banks lowered their prime lending rate to 8% following a reduction in the federal funds rate by the Federal Reserve. As of July 2025, the prime rate in Canada is 4.95%. |

Explore related products

What You'll Learn

- The prime rate is the interest rate that commercial banks charge their most creditworthy customers

- The prime rate is derived from the federal funds rate, usually using fed funds + 3 as the formula

- The prime rate can indirectly impact the stock market

- The prime rate does not directly impact auto loans

- The prime rate is set by individual banks and used as the base rate for many types of loans

![]()

The prime rate is the interest rate that commercial banks charge their most creditworthy customers

The prime rate is the interest rate that commercial banks offer to their best customers—those with the best credit ratings—on loans and mortgages. It is often referred to as the "base rate" or

The Federal Reserve: Central Bank or Not?

You may want to see also

Explore related products

![]()

The prime rate is derived from the federal funds rate, usually using fed funds + 3 as the formula

The prime rate is the interest rate determined by individual banks and used as the base rate for many types of loans, including mortgages, small business loans, and credit cards. While the Federal Reserve does not directly set the prime rate, most banks base their prime rates on the federal funds rate, or the interest rate set by the Federal Reserve that banks use for overnight loans and to borrow from one another. The Federal Reserve adjusts the federal funds rate to keep the US economy stable, lowering it to encourage economic growth and raising it to prevent inflation.

The prime rate is derived from the federal funds rate, usually using the formula fed funds + 3. For example, if the federal funds rate is 4.50%, the prime rate would be 7.50%. Banks use the prime rate as the starting point for other interest rates, which are set at the prime rate plus an additional percentage based on the borrower's credit score, income, and current debts. For instance, an individual with an excellent credit score might be charged prime plus 9% for a credit card, while someone with a good score might get prime plus 15%.

The prime rate is not a universal rate and can vary among banks. The most commonly quoted prime rate is the one published daily by The Wall Street Journal, which surveys the largest US banks and publishes a consensus prime rate based on their rates. The prime rate can change in response to economic conditions, remaining stable for years or changing multiple times in one year, especially during economically turbulent times.

The prime rate can impact the performance of investments, with higher interest rates generally hurting the market. However, some sectors, like the financial industry, benefit from high interest rates as they increase cash flow by charging borrowers more.

Bank CDs vs Brokered CDs: Which is the Better Investment?

You may want to see also

Explore related products

![]()

The prime rate can indirectly impact the stock market

The prime rate is the interest rate that commercial banks charge their most creditworthy borrowers. Each bank sets its own prime rate, which is derived from the federal funds rate, usually using the formula fed funds + 3%. The prime rate is used as a baseline that most banks use to determine the interest rate for customers who want to take out loans or open new credit cards.

Secondly, changes in the prime rate can impact the demand for stocks and bonds. When stock prices decline, investors may seek to reduce portfolio risk by investing more in bonds, which offer lower-risk debt instruments. This increased demand for bonds allows issuers to offer debt at lower interest rates.

Thirdly, the prime rate can impact the performance of investments. Higher interest rates can hurt the market by decreasing cash flow and stock price declines. However, lower interest rates can encourage consumer and business spending and investment, boosting stock prices.

Lastly, the prime rate can impact the economy, which in turn affects the stock market. The Federal Reserve adjusts the prime rate to control inflation and encourage economic growth. Higher interest rates discourage borrowing and spending, while lower interest rates encourage borrowing and can boost economic activity.

Trump Victory: How Are Bank Stocks Faring?

You may want to see also

Explore related products

![]()

The prime rate does not directly impact auto loans

The prime rate is the interest rate that banks charge their most creditworthy customers. It is based on the federal funds rate, which is the rate that banks use to borrow from each other. While the prime rate does not directly impact auto loans, it does have an indirect effect on them.

The prime rate influences the cost of borrowing money for lenders, which can result in higher auto loan rates and, consequently, more expensive new and used cars. The prime rate also impacts the stock market, with higher interest rates usually hurting the market. However, some sectors, like the financial industry, benefit from high-interest rates as they can charge borrowers more.

The Federal Reserve does not directly set the prime rate, but most banks base their prime rates on the target level of the federal funds rate established by the Federal Open Market Committee (FOMC). The FOMC meets around six times a year to discuss and adjust the federal funds rate based on the economy's state and future projections.

While the prime rate does not directly affect auto loan rates, it influences the cost of borrowing money. The Federal Reserve's decisions on interest rates can impact the rates offered to borrowers in the future. However, the rate a borrower receives for an auto loan is primarily determined by their financial history and credit score. A higher credit score generally leads to a lower interest rate on an auto loan, while a lower credit score results in a higher interest rate.

In summary, while the prime rate does not directly impact auto loans, it influences the overall cost of borrowing and the rates offered to borrowers. The actual rate received by an individual is then determined by their financial history and credit score.

Non-Bank Financial Institutions: What Are They?

You may want to see also

Explore related products

![]()

The prime rate is set by individual banks and used as the base rate for many types of loans

The prime rate is the interest rate determined by individual banks and used as a reference rate or base rate for many types of loans. It is the rate that banks charge their most creditworthy customers, and it is derived from the federal funds rate set by the Federal Reserve. The Federal Reserve meets several times a year to discuss and decide on the federal funds rate, which is then used by banks to set their prime rates.

The prime rate serves as a baseline for most banks to determine the interest rates for their customers who want to take out loans or open new credit cards. It can affect many areas of an individual's financial life, including credit card interest rates, small business loans, mortgages, and personal loans. The prime rate can also impact the stock market, with higher interest rates often hurting the market and lower rates encouraging economic growth.

While the prime rate is set by individual banks, they typically use a formula of "federal funds rate + 3%" to determine it. This means that when the Federal Reserve adjusts its federal funds rate, the prime rate of banks usually follows suit. For example, during the Great Recession, the prime rate hit around 3.25%. Additionally, the prime rate can change multiple times within a year, especially during economically turbulent times.

The prime rate is essential in determining the interest rates for different loan types. Banks set a range of interest rates for each loan type, and the rates charged to individual borrowers are based on their credit scores, income, and current debts. For instance, a person with an excellent credit score might be offered a lower interest rate, such as prime plus 9% for a credit card, while someone with a good score might get a higher rate, such as prime plus 15%.

KeyBank CD Rates: Competitive or Not?

You may want to see also

Frequently asked questions

The prime rate is the interest percentage that commercial banks charge their most creditworthy borrowers. It is used as a baseline that most banks use to determine the interest rate for customers who want to open a new credit card or take out a loan.

Each bank sets its own prime rate. The prime rate is influenced by the policy interest rate set by the country's central bank, also known as the target for the overnight rate. Banks adjust the prime rate according to economic and business cycle shifts.

The prime rate can affect many variable-rate loans and lines of credit. It can also indirectly impact the stock market.

Banks typically lower the prime rate when the central bank lowers its policy interest rate, making borrowing cheaper for banks and lenders. However, the decision to lower the prime rate depends on various factors, including the state of the economy, inflation, and the labour market.