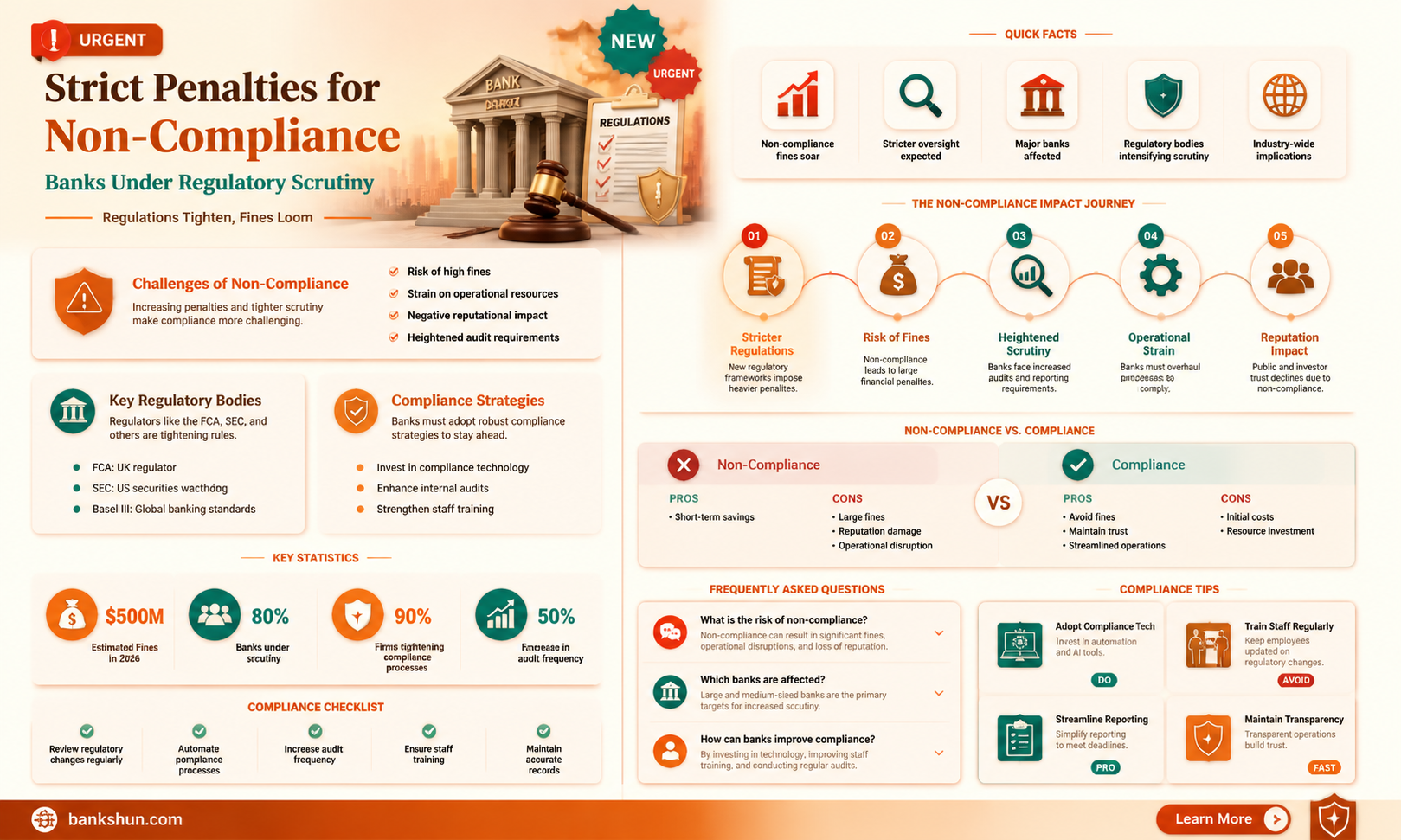

Banks are penalized for non-compliance in several ways. Firstly, governments and regulatory bodies can impose regulatory fines on banks that fail to comply with legal and regulatory guidelines. These fines can be substantial, and banks may also be subject to additional penalties such as growth handcuffs, asset caps, and restrictions on launching new products and services. Furthermore, non-compliance can lead to civil and criminal liability, with the potential for civil lawsuits and, in extreme cases, jail time for bank leadership if they are complicit in financial crimes due to non-compliance. Non-compliance can also result in a loss of public trust, which can be more damaging than financial penalties, and banks may find it challenging to retain customers, especially in international markets, if they are added to sanction lists. The high cost of compliance operations and the constantly changing nature of regulations pose significant challenges for banks, but non-compliance can have severe consequences, making it crucial for banks to stay abreast of the latest regulatory changes and adhere to industry standards.

| Characteristics | Values |

|---|---|

| Consequences of non-compliance | Financial penalties, loss of public trust, civil and criminal liability, loss of license and operating permissions |

| Reasons for non-compliance | High cost of compliance operations, rapidly changing rules |

| Compliance practices | Solid policies and procedures, compliance-oriented culture, regular training, use of technology and automation |

| Compliance requirements | Integration of regulatory requirements into bank's processes and practices, continuous monitoring and updating of compliance processes, cooperation with regulators |

| Compliance risks | Theft of money or sensitive data, fraud, money laundering, unfair practices, financial instability |

| Compliance costs | $5,000 to $100,000 in monthly fines, cost of cloud security tools and audits ($5,000 to $100,000), loss of revenue streams |

Explore related products

![The Penalty [Blu-ray]](https://m.media-amazon.com/images/I/91fZ8MEHZ4L._AC_UY218_.jpg)

What You'll Learn

![]()

Banks face fines for non-compliance

Banks are required to comply with a range of regulations to prevent fraud, protect customers, and maintain financial stability. Non-compliance with these regulations can result in various penalties, including fines, legal consequences, and reputational damage.

Regulatory compliance in the banking sector involves adhering to laws and regulations set by governmental and international bodies, such as the Federal Reserve and the Basel Committee. Banks must also comply with local and global rules from financial agencies. These regulations cover various areas, including risk management, customer protection, and financial stability.

The consequences of non-compliance can be severe. Banks may face regulatory fines, civil and criminal liability, loss of licenses and operating permissions, and damage to their reputation. In some cases, non-compliance can lead to restrictions on growth and operations, as well as increased scrutiny from regulators.

In recent years, several banks have been penalized for non-compliance. For example, in 2024, the CFPB fined Navy Federal Credit Union $95 million for unfairly charging overdraft fees, and Goldman Sachs was penalized $65 million for issues with a credit card product. TD Bank Group was also found to have facilitated the movement of more than $670 million due to major shortfalls in risk management.

To avoid penalties, banks must continuously monitor and update their compliance processes to ensure alignment with the latest industry standards. This includes establishing clear policies and procedures, providing regular staff training, and utilizing technology to streamline compliance tasks. By staying compliant, banks can maintain the trust and confidence of their customers and stakeholders.

Saint Denis Bank: Location and Services

You may want to see also

Explore related products

![]()

Non-compliance leads to loss of license

Non-compliance with banking regulations can have serious consequences for financial institutions, including fines, penalties, and even the loss of their licenses and operating permissions. Regulatory compliance in the banking sector is essential to prevent fraud, protect customers, and maintain financial stability.

Banks must comply with various legal requirements, such as those set by governmental and international bodies like the Federal Reserve and Basel Committee. They must also effectively manage risks, including credit, market, operational, and compliance risks. Non-compliance with these regulations can lead to significant financial penalties, as seen in the case of France's largest bank, which was fined 8.9 billion USD for transferring funds on behalf of countries blacklisted by the US.

Customer protection is another critical aspect of banking compliance. Banks must uphold laws that protect customers against fraud, discrimination, and unfair practices. Failure to do so can result in legal repercussions, damaged reputations, and sanctioning. For example, Navy Federal Credit Union was fined $95 million for unfairly charging overdraft fees. Additionally, non-compliance can lead to a loss of public trust, which can be more damaging than financial penalties.

To maintain their licenses and operating permissions, banks must continuously monitor and update their compliance processes to align with the latest industry standards. They should also collaborate across departments, utilize technology, and establish clear and comprehensive policies and procedures that are regularly reviewed and updated to align with new laws and regulations. By following these practices, banks can reduce compliance risks and maintain legal compliance while preserving operational efficiency.

In summary, non-compliance with banking regulations can lead to severe consequences, including the loss of licenses and operating permissions. Banks must prioritize compliance to maintain their industry standing, protect their reputation, and ensure the safety and well-being of their customers and employees.

Jos. A. Bank: A Brand Worth Trusting?

You may want to see also

Explore related products

![]()

Compliance protects consumers and prevents financial crime

Banks are indeed penalized for non-compliance, and these penalties can be severe. Non-compliance with banking regulations can result in fines and legal consequences, but it can also erode public trust, which can be even more damaging than financial penalties. Banks are required to comply with regulations set by governmental and international bodies, and these regulations are in place to protect consumers and prevent financial crime.

Compliance protects consumers by ensuring fair practices and preventing fraud and discrimination. For example, the Truth in Lending Act (TILA) and the Ability-to-Repay/Qualified Mortgage (ATR/QM) Rule support consumers in making informed decisions about their accounts and credit options. The Dodd-Frank Wall Street Reform and Consumer Protection Act established new standards for remittance transfers, and the National Flood Insurance Program provides federally subsidized flood insurance for homeowners. These measures ensure that consumers are protected from unfair practices and have access to important financial services.

Compliance also plays a critical role in preventing financial crime. Banks must comply with anti-money laundering (AML) regulations and conduct enhanced due diligence on high-risk clients to prevent the facilitation of illicit activities. They must also submit suspicious activity reports (SARs) to authorities, which helps to stop malicious actors and protect the financial system. Additionally, compliance with regulations on interest-rate risk, third-party management, and consumer protection helps to maintain financial stability and prevent systemic risks.

To ensure compliance, banks must establish clear and comprehensive policies and procedures, provide staff training, and regularly update their procedures to stay aligned with new laws and regulations. Technology, such as AML Compliance platforms, can also help banks streamline compliance processes and focus their efforts effectively. By adhering to these practices, banks can maintain consumer trust and confidence, meet legal requirements, and avoid the consequences of non-compliance.

The US Central Bank: What's the Deal?

You may want to see also

![]()

Banks must adhere to legal requirements

Banks are required to comply with a range of legal and regulatory requirements to avoid penalties and maintain their licenses and operations. Non-compliance can result in serious consequences, including fines, civil and criminal liability, and reputational damage.

Legal Requirements

Banks must adhere to various legal requirements imposed by governmental and international bodies. These include:

- Risk Management: Banks must effectively manage different types of risks, including credit, market, operational, and compliance risks. They should also conduct enhanced due diligence for risky customers and screen them against sanctions lists to ensure they are not engaging in illegal activities.

- Customer Protection: Banks are legally obligated to protect their customers against fraud, discrimination, unfair practices, and unauthorized activities. They must also ensure the proper storage and protection of customer data to prevent data breaches.

- Financial Stability: Banks are required to maintain adequate capital, liquidity, and reporting standards to prevent systemic risks and ensure the safety of their customers' funds.

- Anti-Money Laundering (AML) Compliance: Banks must have robust AML compliance measures to prevent the injection of illegally obtained funds into the economic system. AML-related fines on banks are common and can be substantial.

- Collaboration and Reporting: Banks should foster collaboration between their internal departments, such as compliance, legal, and business units. They must also promptly report suspicious activities to the proper authorities and cooperate with regulators to ensure adherence to rules and avoid penalties.

Regulatory Requirements

In addition to legal requirements, banks must also comply with regulatory guidelines set by financial agencies and regulatory bodies. These guidelines can be local or global and are subject to frequent changes. Banks must continuously monitor and update their compliance processes to stay aligned with the latest industry standards. Non-compliance with regulatory requirements can result in regulatory fines and stricter regulations.

To summarize, banks must prioritize compliance with legal and regulatory requirements to avoid penalties and maintain their operations. By adhering to these requirements, banks can protect their customers, prevent financial crimes, and uphold their reputation and trust in the financial industry.

How Bank Transfers Work Over the Weekend

You may want to see also

![]()

Compliance helps maintain financial stability

Compliance plays a pivotal role in maintaining financial stability in the banking sector. It protects consumers, prevents financial crimes, ensures fair practices, and helps banks avoid legal penalties and reputational damage. Compliance also helps banks maintain trust and confidence among stakeholders, including customers and investors.

Banks must comply with regulations set by governmental and international bodies, such as the Federal Reserve and the Basel Committee. These regulations cover various areas, including risk management, customer protection, financial stability, and anti-money laundering controls. For instance, the Gramm-Leach-Bliley Act (GLBA) mandates that financial institutions safeguard nonpublic customer information to prevent identity theft and avoid penalties.

To maintain financial stability, banks should adhere to compliance practices such as proactive risk management, cross-functional collaboration, and regular external audits. By identifying potential risks and implementing preventive measures, banks can mitigate threats and contribute to their long-term sustainability. Cross-functional collaboration between the compliance team, legal department, compliance risk assessment, and other units ensures that all aspects of compliance are thoroughly addressed.

External audits and assessments provide an objective evaluation of the bank's compliance program, helping to identify areas for improvement and maintain transparency and accountability. Additionally, banks should continuously monitor and update their compliance processes to align with the latest industry standards and regulatory changes.

Compliance also plays a role in banking operations and strategy. Compliance teams can help structure company-wide communication flows, streamline processes, and inform decision-making by providing data and insights on security breaches, fraud, suspicious activity, and anti-money laundering flags. By including compliance in strategy discussions, banks can design filtering criteria that exclude companies with suspicious clients or weak regulatory infrastructure from their M&A targets.

In summary, compliance helps maintain financial stability in banks by safeguarding consumers, preventing crimes, ensuring fair practices, avoiding penalties, and building trust. It involves adhering to regulations, proactive risk management, collaboration, audits, and continuous improvement to align with industry standards and regulatory changes. By integrating compliance into their operations and strategies, banks can maintain financial stability and sustain their business in the long term.

Understanding Variable Bank Charges: Fixed or Flexible?

You may want to see also

Frequently asked questions

Non-compliance can result in serious consequences for banks, including:

- Regulatory fines

- Civil and criminal liability

- Reputational damage

- Loss of license

- Difficulty attracting and retaining customers

- Operational restrictions

- Increased costs

- In extreme cases, imprisonment of leadership

Here are some examples of banks being penalized for non-compliance:

- In 2024, TD Bank Group was found to have facilitated the movement of over $670 million due to major shortfalls in risk management.

- Navy Federal Credit Union was fined $95 million for unfairly charging overdraft fees.

- Goldman Sachs was fined nearly $65 million for launching a credit card with Apple that did not meet requirements.

- Deutsche Bank was fined $630 million for its role in wash trading from Russia.

- Wells Fargo was fined an undisclosed amount and has been operating under an asset cap for almost seven years due to a spate of offenses.

Maintaining compliance can be challenging for banks due to the following reasons:

- High cost of compliance operations

- Constantly changing regulations

- Complexity of the regulatory environment

- Difficulty in adapting quickly to new rules and requirements