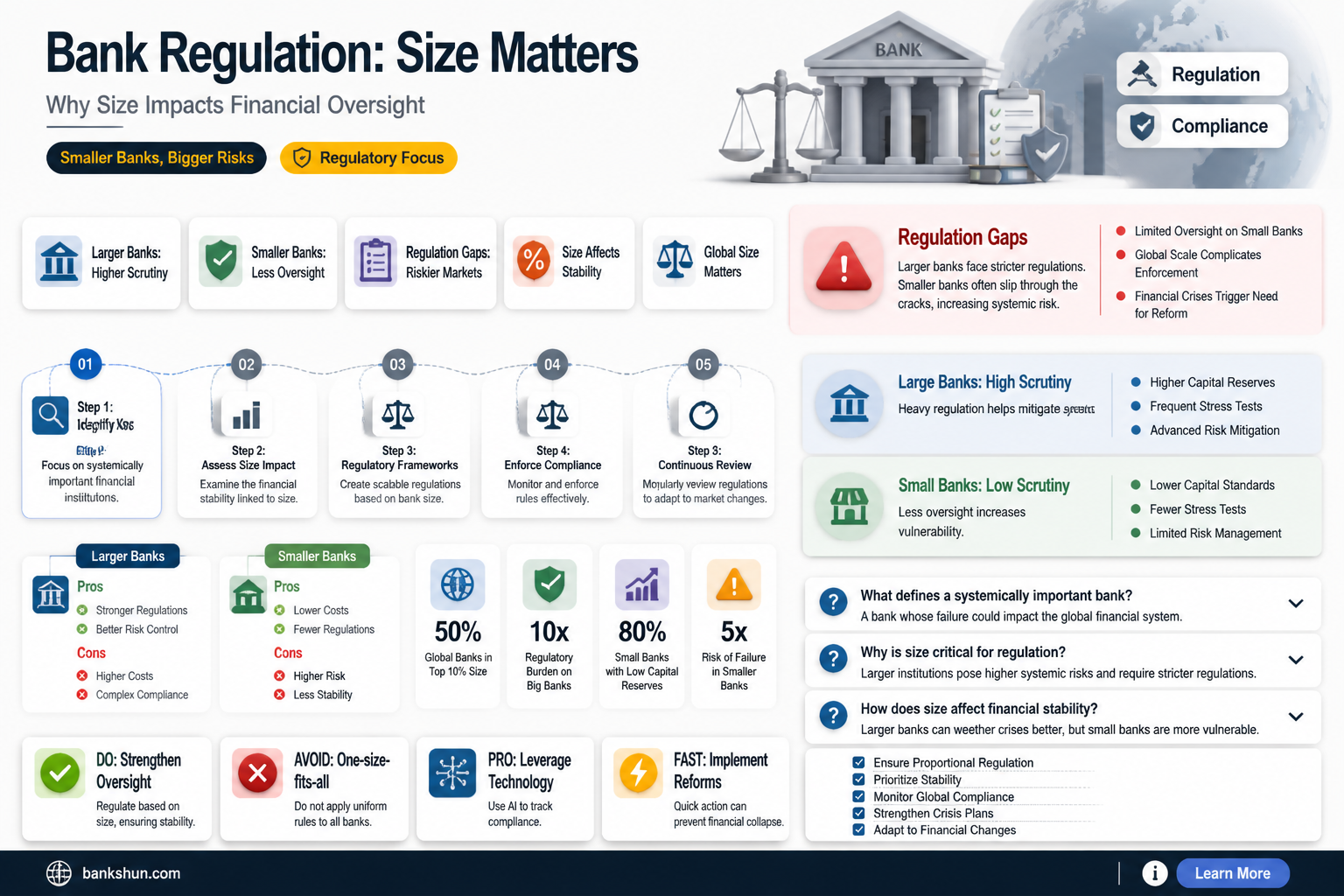

Bank regulations are tailored based on the size and complexity of the institution. The Federal Reserve supervises and regulates banks of all sizes, from very small community banks to some of the largest and most complex financial institutions in the world. However, there have been calls to update the size categories used for regulatory classification as the current thresholds were established in a different economic context, and inflation has significantly eroded the value of the dollar since then. Regulatory compliance has been identified as a key factor in the decline of small and medium-sized banks, as they struggle with the rising costs and limited resources.

| Characteristics | Values |

|---|---|

| Regulatory authority | Almost all banks are subject to the regulatory authority of more than one bank regulatory agency. |

| Supervision | The Federal Reserve supervises and regulates bank holding companies, state member banks, savings and loan holding companies, foreign bank offices in the U.S., and foreign branches and operations of U.S. banks. |

| Regulation | Regulation involves setting the rules by which financial institutions operate, including their formation, operations, activities, and acquisitions. |

| Enforcement | The Federal Reserve takes formal enforcement actions against regulated institutions for violations of laws, rules, or regulations, unsafe or unsound practices, breaches of fiduciary duty, and violations of final orders. |

| Examination | The Federal Reserve sends examiners into the banks it supervises to check their operations and activities. |

| Compliance | Regulated institutions implement practices to ensure they are in compliance with the rules. |

| Size | Regulatory classifications are based on outdated asset-size thresholds, and there is a need to revise the size thresholds that determine regulatory standards. |

| Complexity | Supervision of financial institutions is tailored based on the size and complexity of the institution. |

Explore related products

What You'll Learn

![]()

The Federal Reserve supervises banks of all sizes

In the United States, banks are subject to the regulatory authority of more than one regulatory agency. All banks fall under the supervision and regulation of their chartering authority at either the state or federal level. If a state bank becomes a member of the Federal Reserve System, the Federal Reserve becomes its primary federal supervisor.

The Federal Reserve's supervision of financial institutions is tailored based on the size and complexity of the institution. It involves monitoring, inspecting, and examining these institutions to ensure compliance with rules and regulations and safe and sound operations. Federal Reserve examiners are sent into the banks to check their operations and activities, such as testing capital adequacy and assessing processes. Banks are provided with examination findings and are expected to address any identified weaknesses. The Federal Reserve also takes enforcement actions against regulated institutions for violations and unsafe practices.

While the Federal Reserve supervises banks of all sizes, the regulatory landscape for banks in the U.S. is complex. Banks may be subject to multiple regulatory agencies and overlapping regulations. Additionally, there have been calls to update the size-based regulatory classifications for banks, as the current thresholds are seen as outdated and no longer reflective of the changing economic landscape and inflation. The regulatory burden is particularly challenging for smaller banks, which may lack the resources and scale to keep up with larger institutions.

Transfer Apple Cash to Your Bank Account

You may want to see also

Explore related products

![]()

Regulatory compliance disproportionately affects small and medium-sized banks

Banks are subject to the regulatory authority of multiple agencies. These agencies include the Federal Reserve System, the Federal Deposit Insurance Company (FDIC), and the Office of the Comptroller of the Currency (OCC). The Federal Reserve supervises and regulates banks ranging from very small community banks to some of the largest financial institutions in the world. The FDIC provides federal insurance of deposits at commercial banks and acts as a receiver for failed banks. State regulatory agencies are also responsible for chartering and supervising state banks and foreign banks located within their respective states.

The increased regulatory requirements have resulted in higher compliance costs for small and medium-sized banks. A study titled "How are small banks faring under Dodd-Frank?" found that approximately 90% of respondents reported an increase in compliance costs, with 82.9% reporting increases of more than 5%. The efficiency ratio, or the cost to generate a dollar of revenue, has risen to 76 cents for banks with assets of under $100 million, compared to 69 cents for banks with assets of $100 million to $500 million.

The decline in the fortunes of small and medium-sized banks can also be attributed to their limited resources and the impact of advances in information technology. These banks often operate below the minimum efficient scale due to a shortage of employees, and their customers are shifting to larger banks that can provide more up-to-date technology. As a result, the market share of small banks in terms of assets has decreased, and there has been a sharp decline in small business and residential lending.

Mr. Banks' Story: The Making of Mary Poppins

You may want to see also

Explore related products

![]()

Size-based regulatory categories are outdated

In the United States, banks are subject to the regulatory authority of more than one regulatory agency. These agencies include the Federal Reserve System, the Federal Deposit Insurance Company (FDIC), and the Office of the Comptroller of the Currency (OCC). The Federal Reserve supervises and regulates banks of all sizes, from very small community banks to some of the largest and most complex financial institutions in the world.

The Federal Reserve's supervision and regulation of banks are tailored based on the size and complexity of the institution. However, the size-based regulatory categories used to classify banks are outdated and no longer reflect the current economic landscape. These categories are based on asset-size thresholds determined in a different era, and they have not kept up with inflation, technological advancements, and increased competition in the financial industry.

As a result, banks are forced to choose between shrinking their ambitions or outgrowing their regulatory category, adding expense and complexity to their operations. This misalignment between regulatory categories and the actual size of banks can hinder their ability to serve smaller businesses and desired customers. Furthermore, the failure to update size-based regulatory categories can put banks at a competitive disadvantage compared to similarly sized non-bank competitors with lower regulatory overhead.

To address this issue, it is recommended to recalibrate and index the size thresholds used for regulatory classification to inflation. This would involve doubling the current size thresholds for the largest and smallest banks and allowing reasonable timing for banks to transition to the appropriate category as their asset size changes. By updating the size-based regulatory categories, banks will have more flexibility to grow and better meet the needs of their customers, ensuring a strong and competitive banking industry.

M&T Bank: Where Are Their Branches Located?

You may want to see also

Explore related products

![]()

The Federal Deposit Insurance Company (FDIC) supervises banks

In the United States, banks are subject to the regulatory authority of multiple agencies. The Federal Deposit Insurance Company (FDIC) is an independent agency created by Congress to maintain stability and public confidence in the nation's financial system. The FDIC provides deposit insurance to protect customers' money in the event of bank failure. This insurance is mandatory for Federal Reserve member banks and may be extended to non-member banks with FDIC approval. The FDIC also has the authority to examine and supervise banks for safety, soundness, and consumer protection.

The FDIC supervises and examines state-chartered banks that are not members of the Federal Reserve System. It acts as a receiver for failed banks and administers deposit insurance funds. The FDIC may also appoint itself as a conservator or receiver of an insured depository institution. The FDIC has the power to make special examinations of banks to assess their condition for insurance purposes.

The Federal Reserve System is another key regulator, responsible for supervising and regulating banks of various sizes, including some of the largest and most complex financial institutions in the world. The Federal Reserve ensures that banks follow laws and regulations, conducting examinations and providing written reports on findings. It also releases reports on banking system conditions, regulatory changes, and supervision developments.

In addition to federal regulators, each state has its regulatory agency responsible for chartering and supervising state banks and foreign banks within the state. These agencies issue bank charters, conduct examinations, enforce regulations, and make decisions on proposed branch and merger applications. State banks that obtain deposit insurance or become members of the Federal Reserve must comply with federal regulations in addition to state laws and regulations.

Understanding Point-of-Sale Banking Systems

You may want to see also

Explore related products

![]()

State regulatory agencies regulate banks

In the United States, banking is regulated at both the federal and state levels. Banks are subject to the regulatory authority of more than one bank regulatory agency. All banks fall under the supervision and regulation of their chartering authority at either the state or federal level.

State regulatory agencies regulate state-chartered banks and foreign banks located within their respective states. Banks chartered by the state must follow all applicable state laws and regulations. State regulatory agencies issue bank charters, conduct bank examinations, construct and enforce bank regulations, and decide on proposed branch and merger applications. All state regulatory agencies can impose sanctions such as revoking a state bank’s charter, issuing cease-and-desist orders, removing bank officials, and levying fines.

For example, a California state bank that is not a member of the Federal Reserve System would be regulated by both the California Department of Financial Institutions and the Federal Deposit Insurance Company (FDIC). Likewise, a Nevada state bank that is a member of the Federal Reserve System would be jointly regulated by the Nevada Division of Financial Institutions and the Federal Reserve.

The Federal Reserve Board of Governors in Washington, DC, oversees very small community banks as well as some of the largest, most complex financial institutions in the nation and the world. The Federal Reserve's semiannual Supervision and Regulation Report provides analysis and updates on banking system conditions, recent regulatory changes, and supervision developments.

Other federal regulatory agencies responsible for supervising commercial banks and administering state and federal banking laws include the Federal Reserve System, the Office of the Comptroller of the Currency (OCC), and the FDIC. The OCC is the primary supervisory agency for national banks, savings associations, and federal branches of foreign banks. The FDIC provides federal insurance of deposits at commercial banks and acts as a receiver for failed banks.

The Impact of Virus on Banks: Closures and Future

You may want to see also

Frequently asked questions

Yes, the Federal Reserve supervises and regulates banks based on their size and complexity. The Federal Reserve also releases reports on the conditions of banks and their regulatory activities. However, there are calls to update the size categories used for regulatory classification as the current system is outdated and does not reflect the changing economic landscape.

The Federal Reserve sends examiners to supervised banks to check their operations and activities. These examiners then provide a written report of their findings, and banks must respond with plans to fix any issues. The Federal Reserve also takes enforcement actions against regulated institutions for violations and unsafe practices.

Yes, in addition to size, banks are regulated based on their activities and how they are formed. For example, banks with deposit insurance are subject to certain statutes of the Federal Deposit Insurance Act. Additionally, state banks must comply with state laws and regulations, while Federal Reserve member banks must follow federal regulations.