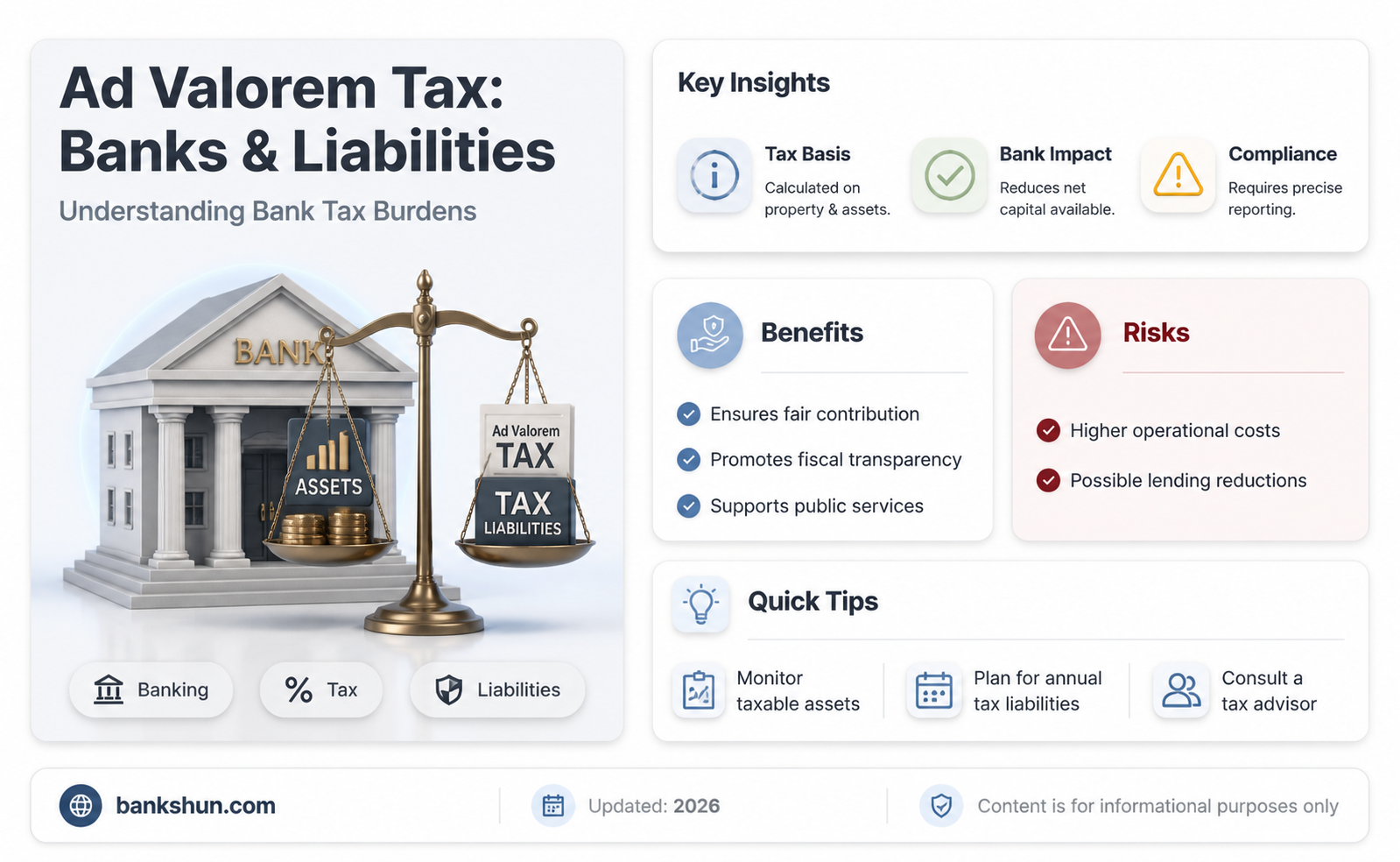

Ad valorem tax is a tax imposed on the value of a product or service, commonly referred to as according to value in Latin. It is applied to various transactions and properties, such as real estate, vehicles, and business equipment. The tax rate is typically calculated as a percentage of the assessed value, also known as the fair market value, of the item being taxed. This form of taxation is used by local and state governments to fund public services and projects, such as schools, parks, and infrastructure. While ad valorem taxes are a significant source of revenue for these governments, they can also lead to issues such as tax avoidance and regressive taxation. Understanding the impact of ad valorem taxes on banks and other financial institutions is crucial for evaluating their overall economic implications.

| Characteristics | Values |

|---|---|

| Definition | A tax whose amount is based on the value of a transaction or of a property |

| Other Names | Value-added tax (VAT), sales tax, property tax |

| Calculation | Multiplying the ad valorem assessment by the ad valorem tax rate |

| Tax Rate | Typically 20% on supplies of goods and services |

| Exemptions | Certain goods and services, religious entities, governments, and nonprofit groups |

| Usage | Third largest source of government revenues |

| Application | Property, sales, and import duty taxes |

| Examples | Municipal property taxes, vehicle registration fees, inheritance tax, and tariffs |

Explore related products

What You'll Learn

![]()

Ad valorem property tax

Ad valorem is a Latin phrase that means "according to value". Ad valorem property tax is a levy imposed on the assessed value of the property being taxed. It is typically imposed annually on the property owner by a municipality or other government entity.

BMO Harris Bank: What Does the Name Stand For?

You may want to see also

Explore related products

![]()

Ad valorem value-added tax (VAT)

Ad valorem, a Latin phrase, means "according to value". Ad valorem value-added tax (VAT) is one of the three types of ad valorem tax, the other two being property tax and sales tax. Ad valorem tax is levied based on the assessed value of the assets, goods, or services being taxed.

The value-added tax (VAT) is levied on the added value that results from each exchange. It is charged at the standard rate of 20% on supplies of goods and services. It is a tax on consumer spending. Certain goods and services are exempt from VAT, and others are subject to VAT at a lower rate of 5% (the reduced rate) or 0% ("zero-rated"). VAT is an indirect tax, meaning the consumer who bears the burden of the tax is not the entity that pays it. The consumer ultimately pays the entire VAT paid by the other businesses in the prior stages.

The modern variation of VAT was first implemented by Maurice Lauré, joint director of the French tax authority, who implemented VAT on 10 April 1954 in France's Ivory Coast colony. Assessing the experiment as successful, France introduced it domestically in 1958. Following the creation of the European Economic Community in 1957, the Fiscal and Financial Committee set up by the European Commission in 1960 under the chairmanship of Professor Fritz Neumark made its priority objective the elimination of distortions to competition caused by disparities in national indirect tax systems. This led to the EEC issuing two VAT directives, adopted in April 1967, providing a blueprint for introducing VAT across the EEC.

As of 2020, more than 160 countries collect VAT. VAT can be accounts-based or invoice-based. All VAT-collecting countries except Japan use the invoice method. Using invoices, each seller pays VAT on their sales and passes the buyer an invoice that indicates the amount of tax paid excluding deductions (input tax). Buyers who add value and resell the product pay VAT on their sales (output tax). The difference between output tax and input tax is the amount paid to the government (or refunded, in the case of a negative amount).

Joseph A. Bank Suit Sale: Dates and Deals Revealed

You may want to see also

Explore related products

![]()

Ad valorem sales tax

Ad valorem is a Latin phrase that means "according to value". Ad valorem taxes are based on the assessed value of the item being taxed. The most common ad valorem taxes are property taxes levied on real estate, but they can also be assessed as a component of car registration. They may extend to tax applications such as import duty taxes on goods from abroad.

Ad valorem taxes are typically calculated on an annual basis, such as local property taxes, unlike transactional taxes, which are charged at the time of the transaction. An example of a transactional tax is sales tax. However, many jurisdictions consider transactional taxes as a type of ad valorem tax.

Ad valorem property taxes are usually levied by municipalities but they may also be levied by other local government entities such as counties, school districts, or special taxing districts. Property owners can be subject to ad valorem taxes levied by more than one entity, such as by both a municipality and a county. Ad valorem property taxes are typically a major, if not the primary, revenue source for both state and municipal governments. Municipal property ad valorem taxes are commonly referred to as "property taxes".

Saint Denis Bank: Location and Services

You may want to see also

Explore related products

![]()

Ad valorem inheritance tax

Ad valorem tax, derived from the Latin phrase "ad valorem", meaning “according to value”, is a tax imposed based on the value of a transaction or property. The most common ad valorem taxes are property taxes levied on real estate, but they can also be applied to personal property, such as cars, boats, or other major assets. These taxes are typically calculated as a percentage of the property's fair market value, which is determined by the marketplace and assumes a willing buyer and seller with reasonable knowledge of the property.

Ad valorem taxes can be imposed annually, as in the case of property taxes, or at the time of a transaction, such as with sales tax or value-added tax (VAT). In some cases, ad valorem taxes can be linked to significant events, such as inheritance. For example, in Georgia, the Title Ad Valorem Tax (TAVT) applies to vehicles inherited or purchased from an estate. If a vehicle is in the annual ad valorem tax system, an individual inheriting it has the option to continue with the annual ad valorem tax or pay a one-time TAVT at a reduced rate of 0.5% of the fair market value of the vehicle.

While ad valorem taxes are often associated with property and transactions, they can also take other forms. For instance, in some countries, stamp duty is imposed as an ad valorem tax. Additionally, ad valorem tariffs are taxes applied to foreign goods imported into a country, calculated as a fixed percentage of the product's value.

It is worth noting that ad valorem taxes are a significant source of revenue for state and municipal governments, particularly in jurisdictions without a personal income tax. These taxes help finance public institutions and various projects that serve society.

Understanding the Legal Tender Status of Bank of England Notes

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![]()

Ad valorem tax on banks' property

Ad valorem is a Latin phrase that means "according to value". An ad valorem tax is a levy imposed on the value of a transaction or property. It is typically imposed at the time of a transaction, such as in the case of a sales tax or value-added tax (VAT).

Ad valorem tax may also be imposed annually, as in the case of property tax. This is the most common form of ad valorem tax. It is levied on the taxpayer's personal and commercial property, including real property or real estate, and personal property such as motor vehicles, business equipment, and other major personal property.

Ad valorem property taxes are usually levied by local jurisdictions such as counties, cities, school districts, or special taxing districts, also known as special purpose districts. Property owners can be subject to ad valorem taxes levied by more than one entity, such as by both a municipality and a county. These taxes are a major, if not the primary, source of revenue for state and municipal governments.

Ad valorem tax on property is calculated as a percentage of the assessed value of the property, commonly referred to as the fair market value. This is the estimated sales price of the property assuming a transaction between a willing buyer and a willing seller, both with reasonable knowledge of all pertinent facts about the property, and neither party being compelled to complete the transaction.

Banks, as property owners, are subject to ad valorem tax on their real estate holdings. This would include any improvements to the land, such as buildings and other man-made structures.

The Mysterious Disappearance of Robin Banks in New Jersey

You may want to see also

Frequently asked questions

Ad valorem is Latin for "according to value". Ad valorem tax is levied based on the assessed value of the assets, goods, or services being taxed. It is imposed depending on the monetary value of a property or transaction.

There are three types of ad valorem tax: property tax, value-added tax (VAT), and sales tax.

Ad valorem tax is calculated as a percentage of the assessed value of the property, goods, or services. The percentage rate is referred to as the tax rate or the levy rate.

Ad valorem tax is imposed on the monetary value of a property or transaction. Banks are not exempt from monetary transactions and owning property, therefore, they are subject to ad valorem tax.

![TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)