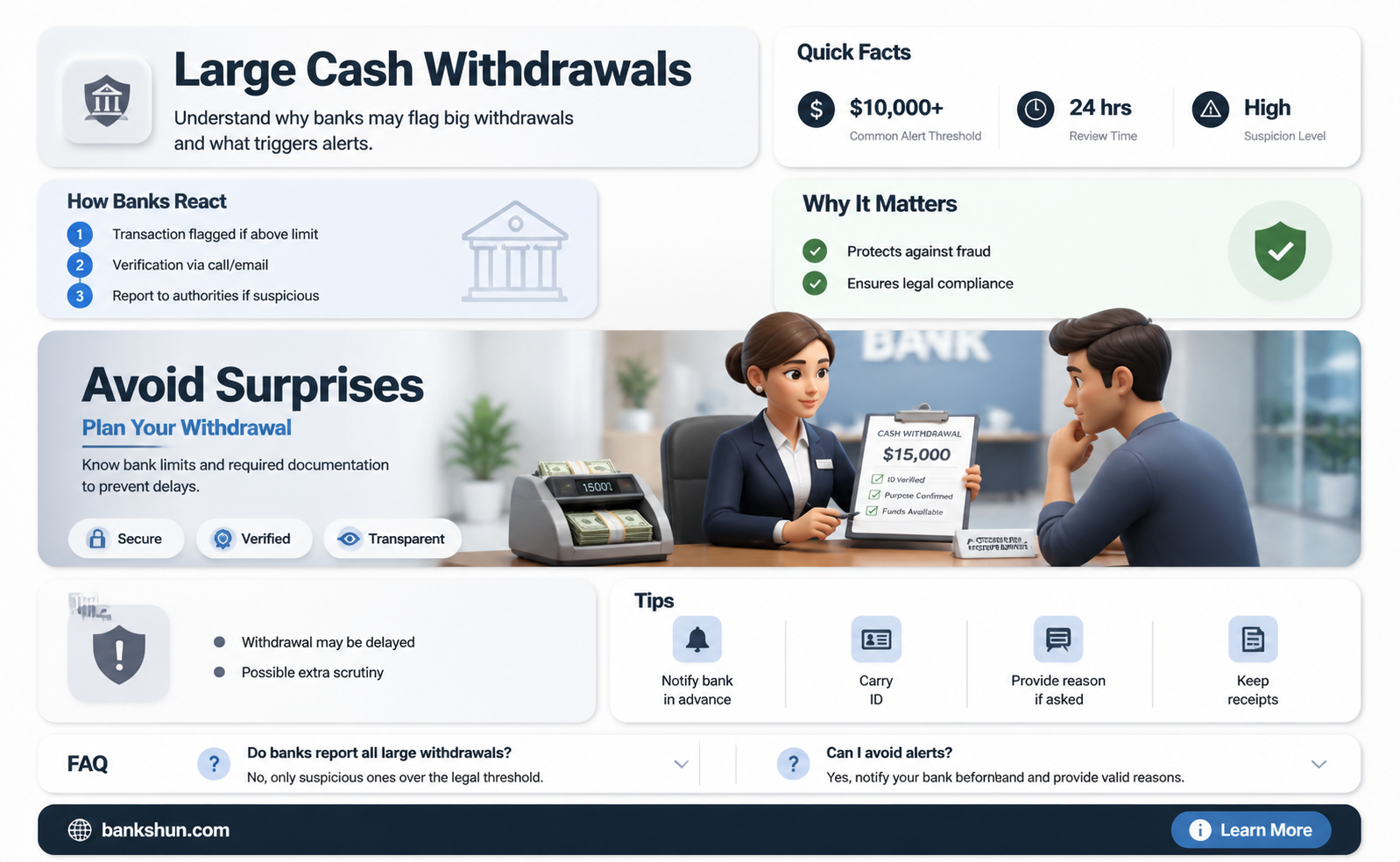

Banks are required to be vigilant about large cash withdrawals due to the risk of money laundering and other financial crimes. In the US, transactions of $10,000 or more must be reported to the IRS, and banks may request advance notice for such withdrawals. While there are no laws prohibiting individuals from withdrawing and carrying large amounts of cash, it is uncommon and can arouse suspicion from banks and authorities. To avoid scrutiny, individuals may structure transactions to stay below the $10,000 threshold, but this practice is illegal and can lead to money laundering charges. Ultimately, large cash withdrawals are not inherently dishonest, but they may require additional explanations and documentation to ensure compliance with anti-money laundering regulations.

| Characteristics | Values |

|---|---|

| Amount that triggers suspicion | $10,000 |

| Amount that triggers investigation | $5,000 |

| Reasons for suspicion | Using large amounts of cash when most people would use common money transfer services |

| Reasons for suspicion | "I hate banks" is a suspicious explanation for having cash |

| Reasons for investigation | Money laundering |

| Reasons for investigation | Fraud |

| Reasons for investigation | Embezzlement |

| Reasons for investigation | Structuring: breaking up large withdrawals to avoid reporting requirements |

| Reasons for investigation | Disguising cash so it cannot be associated with the underlying crime |

Explore related products

What You'll Learn

- Withdrawals of $10,000 or more require reporting to the IRS

- Banks may ask for more details to protect customers from fraud

- Withdrawing just under $10,000 can be seen as suspicious

- Withdrawing large sums of cash is uncommon and may be judged

- Large cash withdrawals may be a warning sign of money laundering

![]()

Withdrawals of $10,000 or more require reporting to the IRS

Banks are required to report cash deposits of at least $10,000 to the federal government. This requirement was established by the Bank Secrecy Act, passed by Congress in 1970, and adjusted with the Patriot Act in 2002. The law aims to curb money laundering and other illegal activities. As a result, withdrawals of $10,000 or more are also subject to reporting.

When an individual withdraws $10,000 or more in cash, the bank or credit union will report it to the Internal Revenue Service (IRS). The IRS will then typically share this information with local and state authorities. This reporting is done through Form 8300, which is used to report cash payments over $10,000 received in a trade or business. The form must be filed within 15 days of receiving the cash, and a copy must be kept for five years.

Form 8300 is required for any individual, company, corporation, partnership, association, trust, or estate that receives more than $10,000 in cash in a single transaction or related transactions. This includes businesses such as dealers in jewelry, furniture, boats, aircraft, or automobiles; pawnbrokers; attorneys; real estate brokers; insurance companies; and travel agencies. Tax-exempt organizations may also need to report certain transactions, although they are not required to file Form 8300 for charitable cash contributions.

It is important to note that even if an individual makes cash deposits over several days that add up to $10,000 or more, they will still be reported. This applies regardless of whether the deposits are made across multiple banks. Additionally, suspicious activity detected by the bank or institution in excess of $5,000 is also required to be reported. While voluntary, individuals can also choose to report suspicious transactions below $10,000 through Form 8300 without informing the customer.

While withdrawing large amounts of cash may raise suspicions, there are legitimate reasons for doing so. For example, a professional gambler may withdraw a large sum of cash to use for their trade and then deposit their winnings a few days later. Providing a reasonable explanation for the withdrawal can help alleviate suspicions. However, a vague or non-explanation, such as "I just hate banks," may lead to assumptions of unsavory activities.

The Federal Reserve Bank: Its Role and Responsibilities

You may want to see also

Explore related products

![]()

Banks may ask for more details to protect customers from fraud

Banks are required by law to report cash transactions over $10,000 to federal authorities. This includes both deposits and withdrawals. This requirement was established as part of the Bank Secrecy Act in 1970 and was adjusted by the Patriot Act in 2002 to curb money laundering and other illegal activities. Banks also report suspicious transactions below $10,000 by filing currency transaction reports.

While large cash transactions may be flagged by banks, there are legitimate reasons for using large amounts of cash. For example, a professional gambler may withdraw a large sum of cash every Thursday and deposit it back into their account on Monday. However, providing a vague or non-explanation for large cash transactions, such as "I just hate banks," is likely to raise suspicions.

Banks have a responsibility to protect their customers from fraud and identity theft. To this end, they employ various security measures, such as monitoring accounts for unusual activity and requiring strong passwords for online banking. If a bank detects unusual activity, it may contact the customer to confirm their identity before allowing them to complete actions online. Banks will also restrict access to online banking and require further proof of identity if necessary.

It's important to note that banks will never request sensitive information like passwords, PINs, or full Social Security numbers through unsolicited channels. If a customer suspects they have fallen victim to a fraudulent scheme, they should immediately contact their bank using the publicly available customer service number and provide all pertinent information. By taking proactive security measures and staying vigilant, banks and customers can work together to foster a safer banking environment.

The US Bank Tower: A History of Construction

You may want to see also

Explore related products

![]()

Withdrawing just under $10,000 can be seen as suspicious

Banks and financial institutions are required to file a Currency Transaction Report (CTR) with the Financial Crimes Enforcement Network (FinCEN) when a customer makes a cash withdrawal of $10,000 or more. This report is not illegal, but it does bring the transaction under scrutiny, and even lawful transactions may be investigated by authorities.

To avoid having a CTR filed, customers may deliberately withdraw amounts just under the $10,000 threshold. However, this can appear suspicious, and banks may still choose to report these transactions or any cases of transactions totaling $10,000 annually. Additionally, suspicious activity in excess of $5,000 may also be reported.

Providing a reasonable explanation for withdrawing a large amount of cash can help reduce suspicions. For example, a professional gambler may withdraw a large amount of cash every Thursday and deposit it back on Monday. However, providing a non-explanation like "I just hate banks" may lead to assumptions of covering up something unsavory.

M&T Bank: Understanding the Name and Its History

You may want to see also

Explore related products

![]()

Withdrawing large sums of cash is uncommon and may be judged

Banks are required to file a Currency Transaction Report (CTR) for any cash transaction over $10,000, which is submitted to the Financial Crimes Enforcement Network (FinCEN). This is not an indication of illegal activity, but it does bring the transaction under scrutiny. Even if the intentions behind the withdrawal are entirely lawful, the authorities may still investigate. This is because large cash withdrawals are often associated with criminal activity, such as money laundering, fraud, tax evasion, or embezzlement.

To avoid the reporting requirements, some people may deliberately withdraw amounts just under the $10,000 threshold. However, this practice, known as "structuring," is illegal and can lead to severe penalties. Banks and federal authorities may become suspicious if they notice a pattern of transactions that total $10,000 or more annually. Therefore, it is important to be aware that legitimate reasons for large cash withdrawals do exist, and providing a reasonable explanation for the withdrawal can help to alleviate suspicions.

For example, some individuals may prefer using physical cash as it helps them visualize their spending and keep track of their budget. This practice, known as "cash stuffing" or the "envelope budgeting method", involves withdrawing cash and dividing it into envelopes for different spending categories. However, carrying large amounts of cash can also put individuals at risk of loss or theft, so it is important to only carry the amount needed for the day's purchases and store the rest in a safe place.

Best Banks with No Overdraft Fees: Avoid Those Charges!

You may want to see also

Explore related products

![]()

Large cash withdrawals may be a warning sign of money laundering

Banks are required by law to report cash withdrawals of $10,000 or more to federal authorities. This requirement was established under the Bank Secrecy Act of 1970 and amended by the Patriot Act in 2002. The law aims to curb money laundering and other illegal activities. As a result, large cash withdrawals may be a warning sign of money laundering.

Money laundering is a process that involves disguising the source of illegally obtained funds to make them appear legitimate. It typically involves three stages: placement, layering, and integration. Criminals use various methods to launder money, including bulk cash smuggling, cash-intensive businesses, bank capture, invoice fraud, and the use of casinos and other gambling venues.

Large cash withdrawals could indicate money laundering if the individual making the withdrawal does not have a legitimate source of income that would justify such a large amount of cash. Additionally, if the withdrawal is made in a way that appears suspicious, such as being just under the $10,000 reporting threshold or being split into multiple smaller withdrawals over several days, it could be a warning sign of money laundering.

Financial institutions play a crucial role in detecting and preventing money laundering. They are required to have anti-money laundering programs in place, which include monitoring for suspicious activity and reporting it to the authorities. Banks may also be fined for breaches of money laundering regulations, as seen in the cases of HSBC and BNP Paribas, which were fined $1.9 billion and $8.9 billion, respectively.

While large cash withdrawals can be a warning sign of money laundering, it is important to note that there are also legitimate reasons for individuals to withdraw large amounts of cash. For example, some people may prefer dealing in cash for personal or business reasons, or they may be withdrawing cash for a major purchase or investment. Therefore, while large cash withdrawals may raise a red flag, it is essential to consider all the facts and circumstances before jumping to conclusions.

Institutional Sales: A Rewarding Banking Career?

You may want to see also

Frequently asked questions

Yes, large cash withdrawals can be a cause for suspicion as they may indicate financial scams, money laundering, or other illicit activities. Banks have a responsibility to prevent financial crimes and are required to report cash transactions over a certain threshold (often $10,000) to authorities.

Typically, any cash withdrawal of $10,000 or more is considered a large cash withdrawal and may require advance notice to your bank. Withdrawals near but below this threshold may also be flagged as suspicious.

If you make a large cash withdrawal, your bank will likely ask for more details to understand the purpose of the withdrawal. You may be required to fill out certain forms, provide identification, and disclose the source of funds.

Withdrawing a large amount of cash is not inherently illegal, and as long as you have a legitimate reason and can provide satisfactory explanations, you should not face any issues. However, attempting to structure transactions to avoid reporting requirements or providing false information can lead to money laundering charges and other serious consequences.

While there is no need to be discouraged from accessing your own money, it is essential to be transparent and provide valid reasons for your large cash withdrawal. Being evasive or failing to disclose the purpose of the withdrawal may lead to further scrutiny or reporting to authorities.