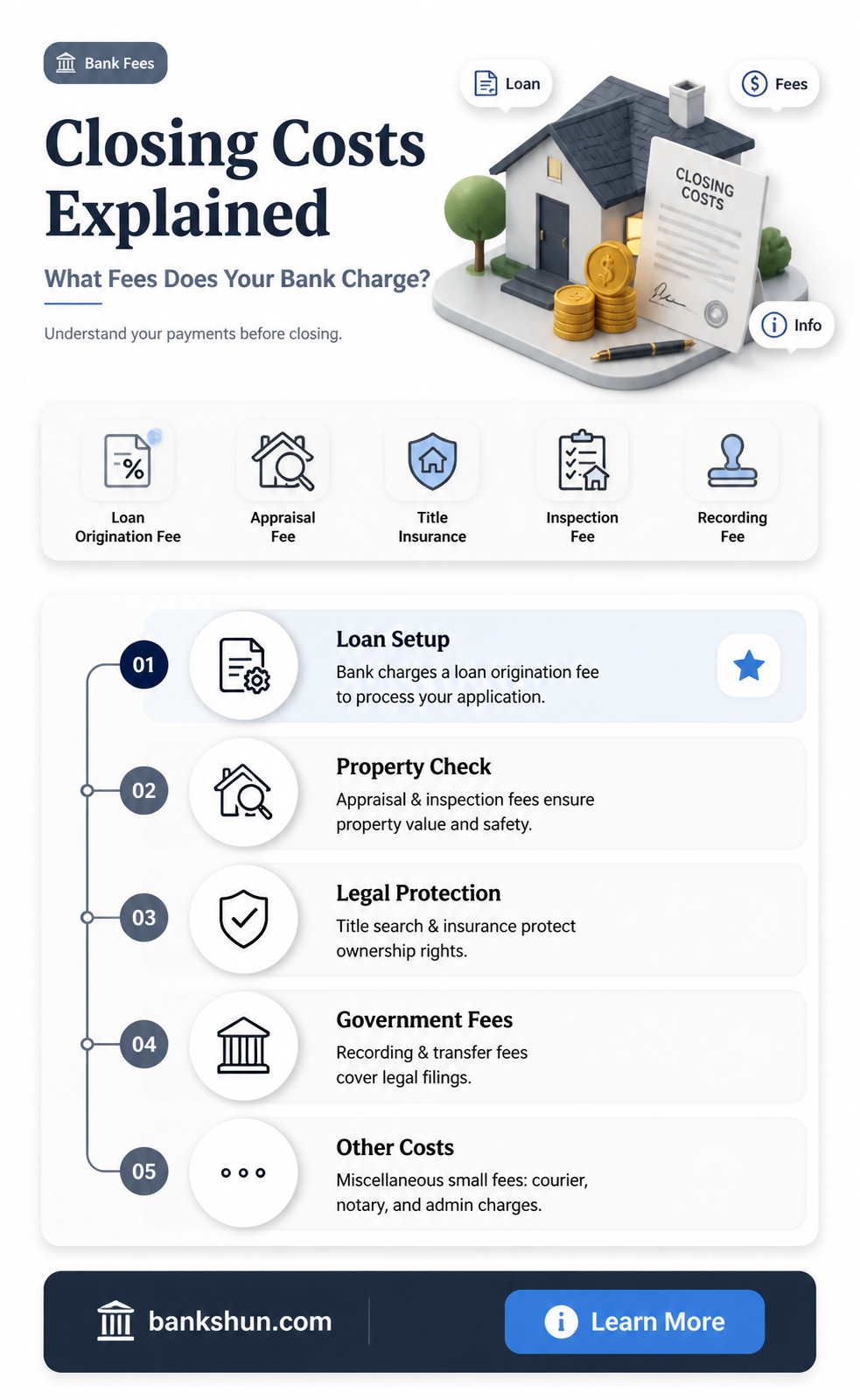

Closing costs are fees and expenses paid when you close on your mortgage and secure a loan for your home. They are typically 2 to 6 percent of the loan amount and can include title insurance, attorney fees, appraisals, taxes, and more. These costs are paid to finalise a real estate transaction and can come as a surprise, especially for first-time buyers. Closing costs are generally paid by the buyer, but the seller may end up paying for some of these costs depending on the contract or state law.

| Characteristics | Values |

|---|---|

| Definition | Fees and expenses paid when you secure a loan for your home, beyond the down payment |

| Cost | 2-6% of the loan amount |

| Components | Title insurance, attorney fees, appraisals, taxes, processing and underwriting fees, etc. |

| Discounts | Lenders may offer discounts or fee waivers, especially if you're an existing customer |

| Payment methods | Cashier's check, upfront payment, or via an escrow account |

| Timing | Closing costs are paid when you close on your mortgage |

| Variability | Closing costs vary depending on the type of loan, location, and lender |

| Disclosure | Lenders are required by law to provide an itemized list of closing costs within 3 business days of application |

Explore related products

What You'll Learn

- Closing costs are fees and expenses paid when securing a loan for a home

- They are usually 3-5% of the loan amount

- They include title insurance, attorney fees, appraisals, taxes, etc

- Lenders must provide an itemized list of closing costs within three business days of a mortgage application

- Buyers can reduce closing costs by opting for lenders that offer discounts

![]()

Closing costs are fees and expenses paid when securing a loan for a home

Closing costs are the fees and expenses paid when securing a loan for a home. They are paid when you close on your mortgage and generally amount to 3-5% of the loan amount, although they can range from 2-6%. These costs are separate from the down payment and include title insurance, attorney fees, appraisals, taxes, and more.

Closing costs can come as a surprise, especially for first-time buyers, so it is important to be aware of them and prepare for them. Early in the mortgage application process, you will receive a Loan Estimate (LE) that will give you an idea of the closing costs you will encounter. By law, lenders must provide this itemized list within a few days of submitting your application.

The specific closing costs you'll need to pay depend on the type of loan you borrow, the lender, and where you live. Some common closing costs include fees for processing and underwriting the loan, which typically run about 0.5-1% of the loan amount. Courier fees, credit reporting fees, and survey fees may also be included.

You will receive your final Closing Disclosure listing your closing costs at least three business days before closing your loan. This document will outline the final costs you need to cover and how much you owe. Generally, you will be asked to pay via cashier's check.

The Banking Industry: What's Happening and Why?

You may want to see also

Explore related products

![]()

They are usually 3-5% of the loan amount

Closing costs are the fees and expenses you pay when you close on your mortgage or home loan. They are usually incurred when you buy or refinance a home. These costs are generally 3-5% of the loan amount, although they can vary significantly and may even reach 6% of the loan amount in some cases. They may include title insurance, attorney fees, appraisals, taxes, and more.

Some lenders charge an application or origination fee to process your loan request, which is usually a percentage of the amount loaned (often 1%). Prepaid interest is another cost that represents the funds for the initial payment of interest on your loan, varying depending on the closing date. Processing and underwriting the loan typically run about 0.5-1% of the loan.

It is important to note that closing costs can be negotiated, and there are ways to reduce them. For example, you can look for lenders that offer discounts or use a no-closing-cost loan. Additionally, you can apply for down payment assistance, especially if you are a first-time homebuyer.

Who is Kaysan? Unraveling the Mystery of His Identity with Banks

You may want to see also

Explore related products

![]()

They include title insurance, attorney fees, appraisals, taxes, etc

Closing costs are fees and expenses paid when you secure a loan for your home, separate from the down payment. They are typically paid by the buyer, but there are exceptions where the seller may pay some or all of the closing costs. Closing costs can be broken down into three main categories: lender fees, third-party fees, and prepaid items.

Lender fees are the charges to process your mortgage, including underwriting and application fees. Third-party fees include title insurance, attorney fees, and appraisals. Title insurance is a form of property insurance to cover any losses or damages that could occur to the borrower's house and belongings. Title search fees are also included here, which is the cost of a background check on the title to ensure there are no unpaid mortgages or tax liens on the property. Attorney fees are determined by the state and the company you use. Appraisals help confirm the fair market value of your home.

Prepaid items include prepaid interest, property taxes, and homeowners insurance. Prepaid interest covers the interest that accrues on your loan from the closing date until the last day of the month. Property taxes are paid upfront for six months, and the amount is based on a fixed percentage of the assessed value of your home. Homeowners insurance must be purchased before closing and can be lowered by shopping around for the best rate.

FDIC Insurance: Which Banks Offer the Highest Coverage?

You may want to see also

Explore related products

![iPhone Charger Fast Charging,[MFi Certified] 2Pack 20W Type C Fast Charger Block with 6FT USB C to Lightning Cable Compatible for iPhone 14/13/12/11 Pro Max/Xs Max/XR/X,iPad(White)](https://m.media-amazon.com/images/I/61efNzZpXML._AC_UY218_.jpg)

![TAKAGI for iPhone Charger, [MFi Certified] Lightning Cable 3PACK 6FT Nylon Braided USB Charging Cable High Speed Transfer Cord Compatible with iPhone 14/13/12/11 Pro Max/XS MAX/XR/XS/X/8/iPad](https://m.media-amazon.com/images/I/71+XQs7+JFL._AC_UY218_.jpg)

![iPhone Charger Fast Charging 2 Pack Type C Wall Charger Block with 2 Pack [6FT&10FT] Long USB C to Lightning Cable for iPhone 14/13/12/12 Pro Max/11/Xs Max/XR/X,AirPods Pro](https://m.media-amazon.com/images/I/61D9UFpTAEL._AC_UY218_.jpg)

![]()

Lenders must provide an itemized list of closing costs within three business days of a mortgage application

When applying for a mortgage, it is important to understand the costs involved. Lenders are required to provide an itemized list of closing costs, also known as a Closing Disclosure, within three business days of receiving a mortgage application. This document outlines the fees and expenses associated with obtaining a loan for a home, beyond the down payment.

The Closing Disclosure provides borrowers with a comprehensive overview of the costs they can expect to incur. These costs can include origination fees, mortgage points, application fees, and other third-party fees. Origination fees typically range from 0.5% to 1% of the loan amount and cover administrative costs associated with the mortgage application. Mortgage points, on the other hand, can be purchased to reduce the interest rate on the loan, with one point equalling 1% of the loan amount.

It is important for borrowers to carefully review the Closing Disclosure to ensure that all costs match their expectations. This includes checking that the loan amount, interest rate, estimated taxes, insurance, and closing costs align with the Loan Estimate provided earlier in the process. If there are any discrepancies or unexpected changes, borrowers should contact their lender or settlement agent immediately for clarification.

In addition to the Closing Disclosure, borrowers can also request a Loan Estimate from multiple lenders to compare different loan options. This document provides important information about the loan terms, costs, loan size, interest rate, and payment schedule. By obtaining Loan Estimates from several lenders, borrowers can make informed decisions about which loan and lender best suit their needs.

Overall, understanding closing costs is crucial when applying for a mortgage. By reviewing the itemized list of closing costs provided by lenders within three business days of application, borrowers can make informed decisions, identify any discrepancies, and ensure they are comfortable with the financial commitments involved in obtaining a home loan.

Understanding Bank Chargebacks: Your Money, Your Rights

You may want to see also

Explore related products

![[Apple MFi Certified] 6Pack 3/3/6/6/6/10 FT iPhone Charger Nylon Braided Fast Charging Lightning Cable Compatible iPhone 14 Pro/13 mini/13/12/11 Pro MAX/XR/XS/8/7/Plus/6S/SE/iPad](https://m.media-amazon.com/images/I/81UCkObyu5L._AC_UY218_.jpg)

![i Phone Charger Fast Charging-20W USB-C Block with 6 Ft Cord [MFi Certified] Compatible with i Phone 14/13/12/11/X Series, i Pad & More [3 Pack]](https://m.media-amazon.com/images/I/61Xyj806LoL._AC_UY218_.jpg)

![[Apple MFi Certified] iPhone Charger, 6Pack(3/3/6/6/6/10 FT) Lightning Cable Apple Charging Fast High Speed USB Compatible 14/13/12/11 Pro Max/XS MAX/XR/XS/X/8-multicolor](https://m.media-amazon.com/images/I/713u0uCrc3L._AC_UY218_.jpg)

![]()

Buyers can reduce closing costs by opting for lenders that offer discounts

Closing costs are the fees associated with creating a loan and buying a home. Buyers tend to pay many of the closing costs, but sellers are also responsible for some. These costs are typically 2 to 5% of the total loan amount and include fees for the appraisal, title insurance, and origination of the loan.

If you're getting a mortgage from your bank, ask for a discount or fee waiver since you're an existing customer. You can also explore down payment assistance programs, especially if you're a first-time homebuyer. Many cities, counties, and states offer these programs to help cover closing costs.

It's important to compare offers from different lenders and get estimates on the same day to ensure accuracy. Additionally, you can shop around for lower-priced vendors for services like pest inspections, surveys, and title searches. However, be aware that independently selected vendors may change their pricing before closing, resulting in unexpected cost increases.

Chromebooks: Secure Choice for Online Banking?

You may want to see also

Frequently asked questions

Closing costs are fees and expenses paid when you close on your mortgage. They include appraisal fees, title fees, homeowner's insurance, and more.

Closing costs are charged by the lender and can include fees for processing and underwriting the loan. They may also be government requirements or dependent on the situation.

Closing costs typically range from 2% to 6% of the loan amount. They can vary depending on the type of loan, location, and other factors.

Closing costs are paid on the closing day, when you sign the final paperwork and receive the keys to your new home.

Yes, there are ways to reduce closing costs. You can look for lenders that offer discounts or ask for a discount if you're already a customer. You can also apply for down payment assistance or use a no-closing-cost loan.

![Ximytec iPhone 14 13 12 11 Charger Fast Charging [MFi-Certified], 20W Type-C Fast Charger Blocks with 6FT USB C to Lightning Cables Compatible with iPhone 14/13/ 12/11/ XS/XR/X/ 8 /iPad (2Pack)](https://m.media-amazon.com/images/I/51szWBozLKL._AC_UY218_.jpg)