Bank runs have been a feature of economic crises throughout history, with the most notable example being the Great Depression of the 1930s, which saw a wave of bank runs that contributed to a prolonged economic recession. A bank run occurs when a large number of depositors simultaneously withdraw their funds, typically due to a loss of confidence in the bank's solvency. While this phenomenon is often associated with commercial banks, it is important to recognize that it can also occur in other financial institutions that perform similar functions, such as money market mutual funds and investment banks, which are collectively known as the shadow banking sector. The vulnerability of banks to runs is intrinsically linked to their business model of maturity transformation, where short-term deposits are used to fund long-term loans, resulting in a liquidity mismatch.

| Characteristics | Values |

|---|---|

| Definition | A bank run occurs when a large number of depositors simultaneously withdraw their funds, fearing that the bank will be unable to repay their deposits in full and on time. |

| Causes | Depositors' loss of confidence in the bank's ability to repay their deposits, often due to economic crises, negative news, or a drop in asset values. |

| Impact | Banks may be forced to sell their assets hastily and at a loss, leading to insolvency and potential collapse. |

| Prevention | Techniques include higher reserve requirements, government bailouts, supervision and regulation, central banks acting as lenders of last resort, and deposit insurance. |

| Examples | Great Depression (1929-1933), 2008 Financial Crisis, Silicon Valley Bank (2023), Washington Mutual Bank (2008), Wachovia Bank (2008) |

| Solutions | Emergency lending facilities, creating a new type of low-cost deposit contract, suspending depositors' withdrawal ability, "narrow banking" with very safe and liquid assets. |

Explore related products

What You'll Learn

![]()

Bank runs and the Great Depression

Bank runs have been a feature of financial crises throughout history, and they played a significant role in the Great Depression of the 1930s. The Great Depression was a severe worldwide economic depression that began with the Wall Street stock market crash in October 1929. This event triggered a wave of bank runs that contributed to the economic downturn and prolonged the depression.

In the context of the Great Depression, a bank run occurred when a large number of anxious depositors lost confidence in the security of their money and rushed to withdraw their deposits in cash. This sudden influx of withdrawal requests forced banks to quickly liquidate loans and sell their assets, often at a loss, to meet the demands for cash. The inability to mobilize bank reserves during these crises further exacerbated the problem. The Federal Reserve System, which was created to act as a lender of last resort, struggled to provide the necessary support, leading to a failure to prevent deflation, according to former U.S. Federal Reserve Chairman Ben Bernanke.

Bank runs during the Great Depression were particularly common in U.S. states with laws allowing banks to operate only a single branch. This structure dramatically increased the risk compared to banks with multiple branches, especially when these single-branch banks were located in areas economically dependent on a single industry. The first wave of banking panics began in the Southern United States in November 1930, triggered by the collapse of banks in Tennessee and Kentucky, which brought down their correspondent networks. New York City, Boston, Chicago, and other major cities also experienced significant bank runs during this period.

The economic damage caused by these bank runs was substantial. The chain of bankruptcies that followed starved domestic businesses and consumers of capital, leading to a long economic recession. The cost of cleaning up a systemic banking crisis can be significant, with fiscal costs and economic output losses averaging 13% and 20% of GDP, respectively, for important crises.

To prevent and mitigate the impact of bank runs, various techniques have been implemented, including higher reserve requirements, government bailouts, supervision and regulation of commercial banks, deposit insurance systems, and the organization of central banks as lenders of last resort. These measures aim to ensure that banks have sufficient liquidity to withstand sudden withdrawal demands and protect the broader economy from the disruptive effects of bank runs.

Explore the Frost Bank Center's Massive Seating Capacity

You may want to see also

Explore related products

![]()

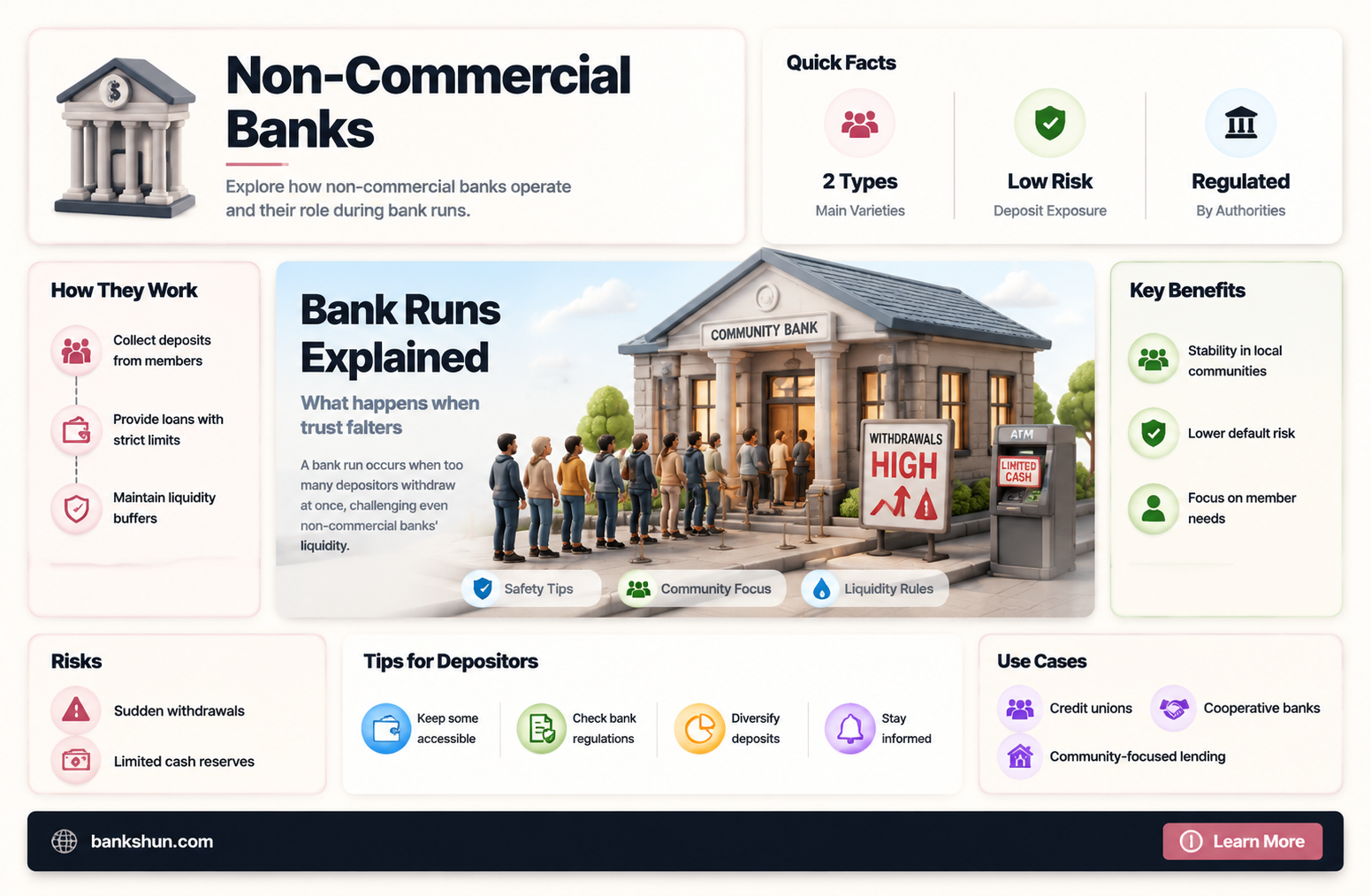

Preventing bank runs

A bank run occurs when a large number of customers simultaneously withdraw their money from deposit accounts due to concerns about the bank's financial stability. This can push an institution into bankruptcy if it cannot maintain a regulatory equity requirement. Bank runs can bring down banks and cause a more systemic financial crisis.

To prevent bank runs, the following measures can be taken:

- Banks can work with authorities to access short-term liquidity, satisfy demands, or raise equity to meet demands. They can borrow money from other banks or the central bank to prevent bankruptcy.

- Central banks can act as lenders of last resort, providing loans to illiquid but solvent financial institutions during times of crisis.

- Deposit insurance can be implemented to reduce the frequency of bank runs by reducing the incentive for depositors to withdraw their money at the first sign of trouble. The Federal Deposit Insurance Corp. (FDIC) in the US, for example, guarantees bank deposits up to $250,000 per depositor, per bank.

- Financial regulators can raise the equity requirements for banks, requiring them to shoulder a greater fraction of any losses in asset value or any runs on uninsured deposits. This would increase "self-insurance" against loss and change bank incentives.

- Banks can proactively slow down the process of a bank run by employing tactics such as having employees and their relatives make long queues and perform slow transactions. In the digital banking era, "technical issues" can be used to delay or stop transactions.

- Institutions can implement measures to safeguard the soundness of their operations, such as loaning out money to struggling banks to prevent a wave of bankruptcies and negative cascading effects on the banking system.

- Governments can implement policies such as higher reserve requirements for banks, supervision and regulation of commercial banks, and providing government bailouts to struggling institutions.

Discover Bank Headquarters: Address and Location

You may want to see also

Explore related products

$70.19 $89.99

![]()

The Diamond-Dybvig model

In the model, banks facilitate savers who prefer liquid accounts with immediate access to their deposits and borrowers who seek long-maturity loans for investments. Banks can profit from this arrangement by charging higher interest rates on loans than they pay on deposits. However, individual depositors may have sudden and unpredictable needs for cash, leading them to demand liquid accounts.

The model suggests that if a depositor expects other depositors to withdraw their funds, the rational response is to rush to withdraw their own deposits first. This creates a situation where the expectation of a bank run becomes a self-fulfilling prophecy. As more depositors anticipate others withdrawing their funds, they are incentivized to rush to withdraw their own, potentially causing the bank to collapse.

To prevent bank runs, Diamond and Dybvig propose government-backed deposit insurance as a solution. By guaranteeing depositors compensation in the event of a bank run, there is no incentive for them to participate in one. This approach, however, removes a source of market discipline as insured depositors no longer closely monitor the bank's financial health.

How Government Shutdowns Affect Banks and Credit Unions

You may want to see also

Explore related products

![]()

Deposit insurance

The history of deposit insurance in the United States is worth noting. The FDIC, established after the 1933 banking crisis during the Great Depression, was the second national deposit insurance scheme globally, following Czechoslovakia. The FDIC provides resources to help unbanked households open accounts and offers tools like the Electronic Deposit Insurance Calculator to help depositors understand their coverage.

Overall, deposit insurance plays a crucial role in mitigating the impact of bank runs and protecting depositors' funds. By ensuring that depositors' money is safe, even in the event of a bank failure, deposit insurance helps to maintain stability and trust in the financial system.

Banks Sending 1099s: What You Need to Know

You may want to see also

Explore related products

$56.56 $95

![]()

Central banks as lenders of last resort

A lender of last resort (LoLR) is a financial entity, usually a country's central bank, that acts as a provider of liquidity to financial institutions that cannot obtain sufficient liquidity in the interbank lending market. In other words, a lender of last resort provides emergency credit to financial institutions that are struggling financially and near collapse.

Since the beginning of the 20th century, most central banks have been providers of lender-of-last-resort facilities. Their functions usually also include ensuring liquidity in the international markets. The objective is to prevent economic disruption as a result of financial panics and bank runs spreading from one bank to another due to a lack of liquidity in the first one.

There is no universal agreement on whether a nation's central bank should be its lender of last resort. Some argue that having a lender of last resort encourages moral hazard, meaning banks can take excessive risks knowing that they will be bailed out. However, proponents of these practices state that the threat of not having a lender of last resort is even more risky and would be a greater threat to the financial system, as seen during the 2008 financial crisis.

Central banks that act as lenders of last resort include the Federal Reserve in the United States, the European Central Bank in the European Union, and the International Monetary Fund's supplemental reserve facility.

The Bank of the US: A Historical Perspective

You may want to see also

Frequently asked questions

A bank run occurs when a large number of depositors simultaneously withdraw their funds, typically due to a loss of confidence in the bank's ability to repay their deposits. This can cause the bank to become insolvent and lead to a systemic financial crisis.

No, while commercial banks are the most well-known type of bank to experience runs, other entities in the shadow-banking sector, such as money market mutual funds and investment banks, can also be subject to runs.

Bank runs are often triggered by negative news or a significant drop in asset values, which causes depositors to worry about the bank's solvency. This can be exacerbated by the sale of assets at a loss, as the bank attempts to meet withdrawal demands, leading to further concerns and withdrawals.

There are several techniques to prevent or reduce the impact of bank runs, including higher reserve requirements, government bailouts, supervision and regulation, the organization of central banks as lenders of last resort, and deposit insurance systems.

Yes, in March 2023, Silicon Valley Bank experienced a bank run caused by venture capitalists. Within one business day, customers withdrew about $42 billion, leading to the bank's collapse and the seizure of its assets by regulators.