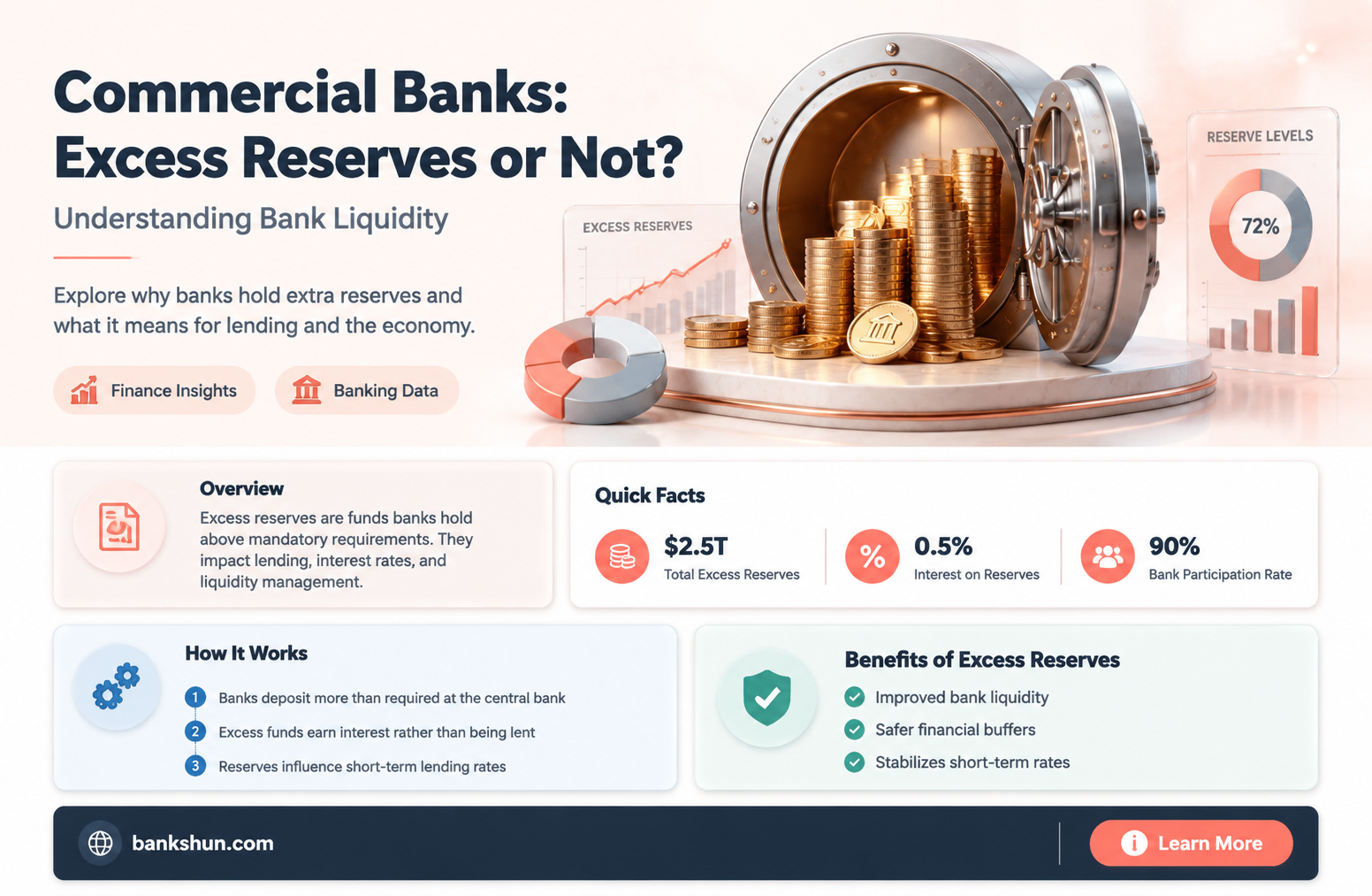

Excess reserves are the additional cash that a bank keeps on hand and declines to lend out. They are held by a bank or financial institution above the reserve requirements set by a central bank. The central bank sets the reserve requirements for commercial banks as a percentage of the deposit liabilities that a commercial bank holds. The Federal Reserve discontinued reserve requirements in 2020, thus eliminating excess reserves. However, banks can still voluntarily hold reserves at the Fed, which pays them interest in a program called Interest on Reserve Balances (IORB).

| Characteristics | Values |

|---|---|

| Definition | Excess reserves are the additional cash that a bank keeps on hand and declines to lend out. |

| Purpose | Excess reserves are a safety buffer to prevent panic if customers find out a bank cannot meet immediate demands. |

| History | Banks have been required by law to hold some reserves for a long time, but they have historically held very little in excess reserves. |

| Interest | Before 2008, banks were not paid interest for holding excess reserves. |

| Interest | In 2008, the Federal Reserve was authorized to pay interest on excess reserves, incentivizing banks to hold more reserves. |

| Monetary Policy | The central bank can use the Interest on Excess Reserves (IOER) rate as a tool for monetary policy. |

| Liquidity | Excess reserves provide additional liquidity buffers for banks. |

| Credit Rating | A higher level of excess reserves can lead to a higher credit rating for financial institutions. |

| Opportunity Cost | Holding excess reserves may lead to an opportunity cost if higher returns could be earned by investing the funds elsewhere. |

| Inflation | Some sources claim that interest on excess reserves helps to guard against inflationary pressures. |

| Federal Reserve | The Federal Reserve discontinued reserve requirements in 2020, eliminating excess reserves. Banks can now voluntarily hold reserves and receive interest through the Interest on Reserve Balances (IORB) program. |

Explore related products

What You'll Learn

![]()

The incentive to hold excess reserves

Banks are incentivized to hold excess reserves for several reasons. Firstly, excess reserves provide a safety buffer for banks, protecting them from sudden loan losses or significant cash withdrawals by customers. Banks can voluntarily hold reserves at the Fed, which pays them interest in a program called Interest on Reserve Balances (IORB). The Federal Reserve implements Interest on Excess Reserves (IOER) to adjust banks' holdings of excess reserves and influence the monetary supply.

The Financial Services Regulatory Relief Act of 2006 authorized the Federal Reserve to pay banks an interest rate for the first time, creating an incentive for banks to hold reserves with a central bank. This rule was originally scheduled to come into effect on October 1, 2011, but the Great Recession accelerated its implementation, with the Emergency Economic Stabilization Act of 2008 bringing it forward to October 1, 2008. As a result, banks became more willing to hold reserves, and excess reserves hit a record $2.7 trillion in August 2014.

The implementation of interest on reserves (IOR) has had a significant impact on banks' incentives to hold excess reserves. Prior to October 2008, reserves paid no interest, and banks had little incentive to hold excess reserves as they would forgo potential income. Instead, they would make loans or invest in other holdings such as bonds. With the introduction of IOR, banks could earn interest on their excess reserves, reducing the opportunity cost of holding them. This led to a significant increase in the amount of reserves in the banking system, as banks chose to hold onto their excess reserves instead of lending them out.

The level of interest paid on excess reserves can be adjusted by the Federal Reserve to influence the incentives for banks to hold reserves. By increasing the interest rate, the Federal Reserve can encourage banks to hold more excess reserves, which can help stabilize the financial system. During economic downturns, the central bank can lower the IOER rate to promote commercial banks to reduce their excess reserves and increase the money supply in the economy.

The Friendship Between Sasha Banks and Bayley: Still Strong?

You may want to see also

Explore related products

![]()

The impact of excess reserves on inflation

Excess reserves refer to the cash held by a bank or financial institution above the reserve requirement set by a central bank. For commercial banks, excess reserves are measured against standard reserve requirement ratios set by central banking authorities. These required reserve ratios set the minimum liquid deposits (e.g. cash) that must be in reserve at a bank, with any amount above this being considered excess.

On the other hand, some economists argue that paying interest on excess reserves can increase the supply of short-term debt and lead to higher bond yields. Additionally, a large volume of excess reserves can impair the liquidity of the funds market. If banks begin lending out their excess reserves, it may become necessary for policymakers to tighten policy quickly to contain inflationary pressure.

In the United States, the Federal Reserve's response to the financial crisis of 2007-2008 and the Great Recession led to a dramatic increase in the supply of reserves in the banking system. While prices have risen only modestly, base money (reserves plus currency) has grown substantially. This has raised questions about the potential limits of the Federal Reserve's ability to continue increasing the supply of reserves while maintaining its inflation-targeting policy.

In summary, while excess reserves can provide additional liquidity and safety for the banking system, they can also impact lending growth and monetary policy. Central banks must carefully manage the level of excess reserves to balance the need for economic stability and inflation control.

Big Banks' Interest in Gold and Silver

You may want to see also

Explore related products

![]()

The opportunity cost of holding excess reserves

Excess reserves refer to the cash held by a bank or other financial institution above the reserve requirement set by a central authority. For commercial banks, this is measured against standard reserve requirement ratios set by central banking authorities. These required reserve ratios set the minimum liquid deposits (e.g. cash) that must be held in reserve, with any additional amounts considered excess.

Before 2008, banks in the U.S. were not paid interest for holding excess reserves. The 2008 Global Financial Crisis led to the decision that the Federal Reserve is authorized to pay a rate of interest to banks on their excess reserves, known as Interest on Excess Reserves (IOER). This incentivizes banks to hold excess reserves, which reduces the money supply. The central bank can use the IOER rate as a tool of monetary policy, raising it to incentivize banks to hold more excess reserves, and lowering it to encourage banks to reduce their excess reserves and increase lending.

While holding excess reserves may lead to higher opportunity costs, it also provides benefits to the bank. Excess reserves provide extra liquidity and safety for the banking system, protecting against unexpected events such as large loan losses or significant cash withdrawals. Additionally, a financial institution can earn a higher credit rating by increasing its level of excess reserves.

Lockbox Banking: Secure Storage, Easy Access

You may want to see also

Explore related products

![]()

The role of the central bank in setting reserve requirements

The central bank of a country plays a pivotal role in setting reserve requirements for commercial banks. The reserve requirement is the minimum amount that a commercial bank must hold in liquid assets, typically determined as a percentage of the deposit liabilities of the bank. This is also known as the cash reserve ratio or reserve ratio. The reserve ratio is an important tool for a country's monetary authority to influence the money supply and implement monetary policy.

The central bank ensures that commercial banks have sufficient cash on hand to meet withdrawal demands and prevent bank runs. By setting reserve requirements, the central bank can limit or expand lending activities, thereby controlling the country's money supply. In some jurisdictions, like the European Union, the central bank does not mandate reserves to be held during the day, while others, like the United States, have eliminated reserve requirements altogether.

The central bank also acts as the "lender of last resort," providing funds to banks facing short-term liquidity shortfalls. This role was particularly crucial during the 2008 financial crisis, where the government intervened to restore confidence in the banking system. The central bank's ability to lend is enhanced by the end of the gold standard, which ensures modern central banks using fiat currency will not run out of reserves to lend.

Additionally, the central bank can influence reserve levels by paying interest on excess reserves, incentivising commercial banks to hold higher reserves, which reduces the money supply. This tool of monetary policy can be adjusted to encourage or discourage excess reserves, depending on economic goals.

In summary, the central bank's role in setting reserve requirements is a critical function to maintain public confidence in the banking system, ensure liquidity, and influence the country's monetary policies. The specific actions and tools employed by the central bank can vary depending on the economic context and the jurisdiction in which it operates.

FDIC: What It Means and Why It Matters

You may want to see also

Explore related products

![]()

The benefits of excess reserves for financial stability

Excess reserves refer to the cash held by a bank or financial institution above the reserve requirement mandated by a central bank or regulatory authority. These reserves are designed to provide a safety buffer for banks, protecting them against unexpected events such as sudden large loan losses or significant cash withdrawals by customers. Holding excess reserves can enhance a bank's financial stability and bring several benefits.

Firstly, excess reserves provide additional liquidity to the banking system. Banks are required to hold a minimum amount of reserves to ensure sufficient liquidity for normal operations, including customer withdrawals. By maintaining excess reserves, banks can better manage their liquidity and cover short-term transactions. This reduces the risk of a bank run, where customers simultaneously withdraw funds, and improves overall financial stability.

Secondly, excess reserves can lead to higher credit ratings for financial institutions. Banks with larger excess reserves are perceived as more financially stable and secure. This increased creditworthiness can enhance their standing in the financial industry and attract more customers.

Additionally, excess reserves can help banks seize unforeseen opportunities or address last-minute outflows. Similar to how individuals may set aside emergency funds, banks can use excess reserves to take advantage of unexpected investment opportunities or cover unexpected expenses. This flexibility allows banks to be more agile and responsive to market changes.

Moreover, the existence of excess reserves can influence monetary policy and interest rates. By adjusting the interest rates paid on excess reserves, central banks can impact the interbank lending market and control the overall money supply. This tool allows central banks to curb lending growth and adjust economic activity without directly altering reserve quantities.

Finally, excess reserves can provide protection against inflationary pressures. Interest paid on excess reserves can help guard against inflation, as higher interest rates can curb spending and borrowing. This, in turn, can contribute to price stability and a more stable economic environment.

Wells Fargo: FDIC Insurance and Your Money

You may want to see also

Frequently asked questions

Excess reserves are the additional cash that a bank keeps on hand and declines to lend out. They are held by a bank in excess of a reserve requirement set by a central bank.

Commercial banks hold excess reserves to protect the banking system by providing additional liquidity buffers. They also serve as a safety net in the event of sudden loan losses or significant cash withdrawals by customers.

Central banks incentivize commercial banks to hold excess reserves by offering interest on these reserves. This interest is known as Interest on Excess Reserves (IOER).

Excess reserves can be used as a tool for monetary policy. By raising the IOER rate, central banks incentivize commercial banks to hold more excess reserves, which reduces the money supply. Conversely, lowering the IOER rate encourages commercial banks to reduce their excess reserves, leading to an expansionary monetary policy.