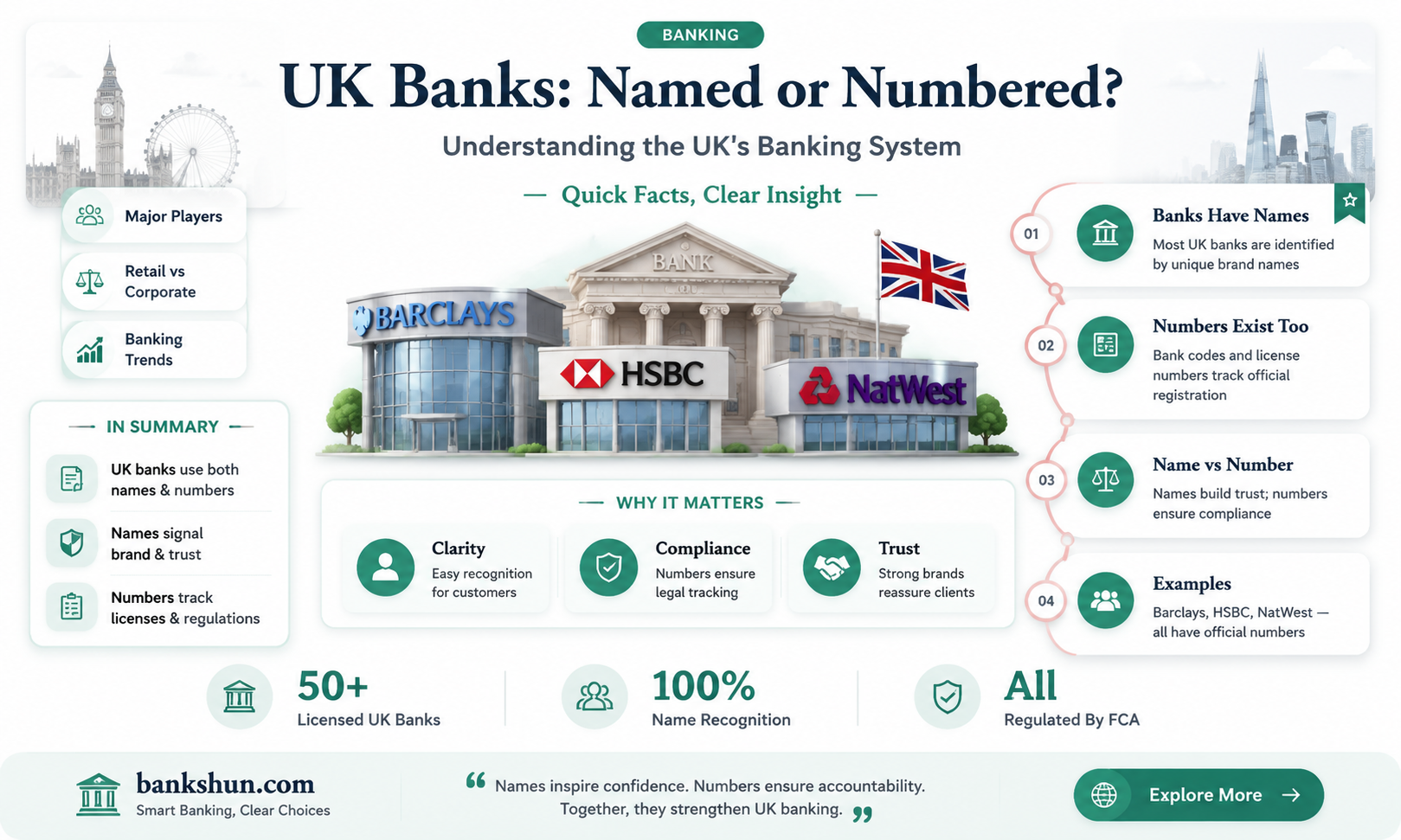

The United Kingdom has a diverse banking landscape, with a mix of private, international, and digital banks, as well as building societies. The retail and commercial banking markets are dominated by the Big Four banks: HSBC, Barclays, Lloyds Banking Group, and NatWest Group. These banks operate multiple brands in the UK and have a global presence. The UK also has numerous other banks, including Spanish-owned Santander UK, Standard Chartered, and digital banks like Revolut and Monzo. The central bank of the UK is the Bank of England, which oversees financial markets and infrastructure. As of 2024, there were 362 banks in the UK, with an average annual growth of 3.3% over the past five years.

| Characteristics | Values |

|---|---|

| Number of banks in the UK | 362 as of 2024, 374 as of 2025 |

| Number of Monetary Financial Institutions in the UK as of June 2024 | 328 |

| Number of banks headquartered in the UK as of June 2024 | 117 |

| Number of independent banks in the UK | Decreased during the 2008 financial crisis |

| Number of physical bank branches in the UK | Decreasing due to the rise of digital banking |

| Number of building societies in the UK as of 2021 | 42 |

| Number of banks authorised to accept deposits in the UK as of February 2025 | 152 |

| Number of banks considered part of the Big Four in the UK | 4 |

Explore related products

What You'll Learn

![]()

The UK's Big Four banks

The UK's banking sector is defined by a mix of established giants and fast-rising digital challengers. The "Big Four" banks in the UK are HSBC, Barclays, Lloyds Banking Group, and NatWest Group. These banks are considered the biggest and most popular in the country, dominating the retail and commercial banking sectors. They are also some of the largest banks in Europe in terms of market capitalization.

HSBC, the largest bank in the UK and Europe, offers a range of financial products and services, including current, savings, and foreign currency accounts, as well as credit cards, mortgages, and insurance products. With roots dating back to 1765, Lloyds Bank is another of the UK's 'Big Four' banks, offering various current accounts, premium accounts, and specialist accounts. Barclays, the second-largest bank in the UK, provides a wide range of financial products, including current and savings accounts, borrowing options, credit cards, investment options, and insurance products. As a multinational universal bank, Barclays has a long history, dating back to 1690. NatWest Group, which includes the Royal Bank of Scotland (RBS), offers a similar selection of current accounts and financial services.

The classification of the "Big Four" is primarily based on the total asset size of each bank's UK-based holding company. However, some people argue that Spanish-owned Santander UK should be included, making it the "'Big Five." The rise of digital challenger banks, such as Revolut, Monzo, and Starling Bank, has disrupted the traditional banking landscape, attracting customers with innovative mobile-first approaches and competitive fee structures. These digital banks are reshaping competition through customer-focused innovation, highlighting a shifting landscape driven by evolving consumer preferences and expectations.

Who is Friends With Whom? Sasha Banks and Alexa Bliss

You may want to see also

Explore related products

![]()

The Bank of England

As a regulator and central bank, the Bank of England does not offer consumer banking services. However, it does manage some public-facing services, such as exchanging superseded bank notes. The bank also offers liquidity support and other services to banks and financial institutions. Commercial banks keep a significant proportion of their cash reserves on deposit at the Bank of England, which they use to settle payments with each other.

Republican Policies: A Plot to Increase Bank Fees?

You may want to see also

Explore related products

![]()

Digital banks

The UK banking sector is undergoing a rapid transformation, driven by technological advancements, evolving consumer demands, and regulatory changes. The country's banks are actively embracing digital transformation, adopting technologies like AI, big data, and blockchain. Digital banks, also known as neobanks or disruptor banks, are mobile-first, app-based institutions with no physical branches. Their lower overhead costs allow them to offer competitive perks such as lower fees, higher interest rates, and personalized digital experiences.

Other notable digital banks in the UK include Atom Bank, one of the earliest digital-only banks in the country, and Monese, which caters specifically to international customers and promotes financial inclusivity. These digital banks provide users with features such as instant spending notifications, insights into spending habits, and the ability to lock their debit cards within the app in case of fraud.

The rise of digital banks in the UK has been facilitated by the widespread adoption of online banking, which has grown from 32% in 2007 to 87% in 2023. This shift towards digital banking has led to a decrease in the number of physical bank branches, with 40% of branches closing between 2012 and 2022.

Jos. A. Bank: A Brand Worth Trusting?

You may want to see also

Explore related products

![]()

Building societies

In the UK, building societies have become fewer in number due to demutualisation in the 1980s and 1990s, and subsequent takeovers by banks. There were 59 building societies in the UK at the start of 2008, falling to 42 by 2021. The five largest as of October 2020 were: Allied Irish Bank (GB) and First Trust Bank, owned by AIB Group; Bank of Ireland UK, owned by Bank of Ireland; Bank Sepah International plc, owned by Bank Sepah of Iran; and Leeds Building Society Ireland, a branch of a UK-based building society.

The Building Societies Association (BSA) represents 42 or 43 UK building societies, along with some larger credit unions.

Coin Counting at Fulton Bank: What Are Your Options?

You may want to see also

Explore related products

![]()

Banks with international operations

The UK banking sector is dominated by the Big Four banks: HSBC, Barclays, Lloyds Banking Group, and NatWest Group. All four banks operate more than one banking brand in the UK and internationally.

HSBC

HSBC is the largest bank in Europe and has a major focus on international markets. It offers international banking services to those living, studying, or investing abroad, allowing customers to manage their global accounts from one place online and make transfers between them with no HSBC fees. HSBC also provides international money transfers and allows customers to hold, send, and manage multiple currencies.

Barclays

Barclays is a multinational universal bank with a history dating back to 1690. It offers international banking services to clients with £100,000 or more in savings and/or investments across all their accounts. For those with £250,000 or more, Barclays provides a personal Relationship Manager to give bespoke, expert guidance on financial goals. Barclays offers international clients access to UK-regulated expert help with lending and investment solutions for both UK and overseas products.

Lloyds Banking Group

Lloyds Bank is one of the oldest banks in the UK, with roots dating back to 1765. It is part of the Lloyds Banking Group, which includes Lloyds TSB and HBOS (Halifax and the Bank of Scotland). Lloyds Bank offers a range of current accounts, including the Classic and Club Lloyds accounts, as well as premium and specialist accounts.

NatWest Group

NatWest Group offers a range of international banking services to customers moving outside the UK or relocating to the country. It has dedicated teams and contact numbers to assist new and existing customers with their international banking needs. NatWest is headquartered in Edinburgh and includes the Royal Bank of Scotland (RBS) as one of its major banks. RBS offers a selection of current accounts similar to those of its parent company.

Clearing Houses: Banking's Necessary Evil?

You may want to see also

Frequently asked questions

Yes, the UK has a diverse banking landscape with 328 Monetary Financial Institutions (MFIs) as of June 2024. The number of banks has been increasing, with 374 MFIs as of 2025.

The "Big Four" banks in the UK are HSBC, Barclays, Lloyds Banking Group, and NatWest Group. These banks are considered the largest and most dominant in the retail and commercial banking sectors.

In addition to the "Big Four," other major banks in the UK include Santander UK, Nationwide Building Society, Standard Chartered, and Royal Bank of Scotland (RBS).

The Bank of England is the central bank of the United Kingdom. It oversees financial markets, financial market infrastructure, and ensures financial stability.

Yes, the UK has a number of digital banks and alternative providers, such as Revolut, Monzo, and First Direct, which offer online and mobile banking services.