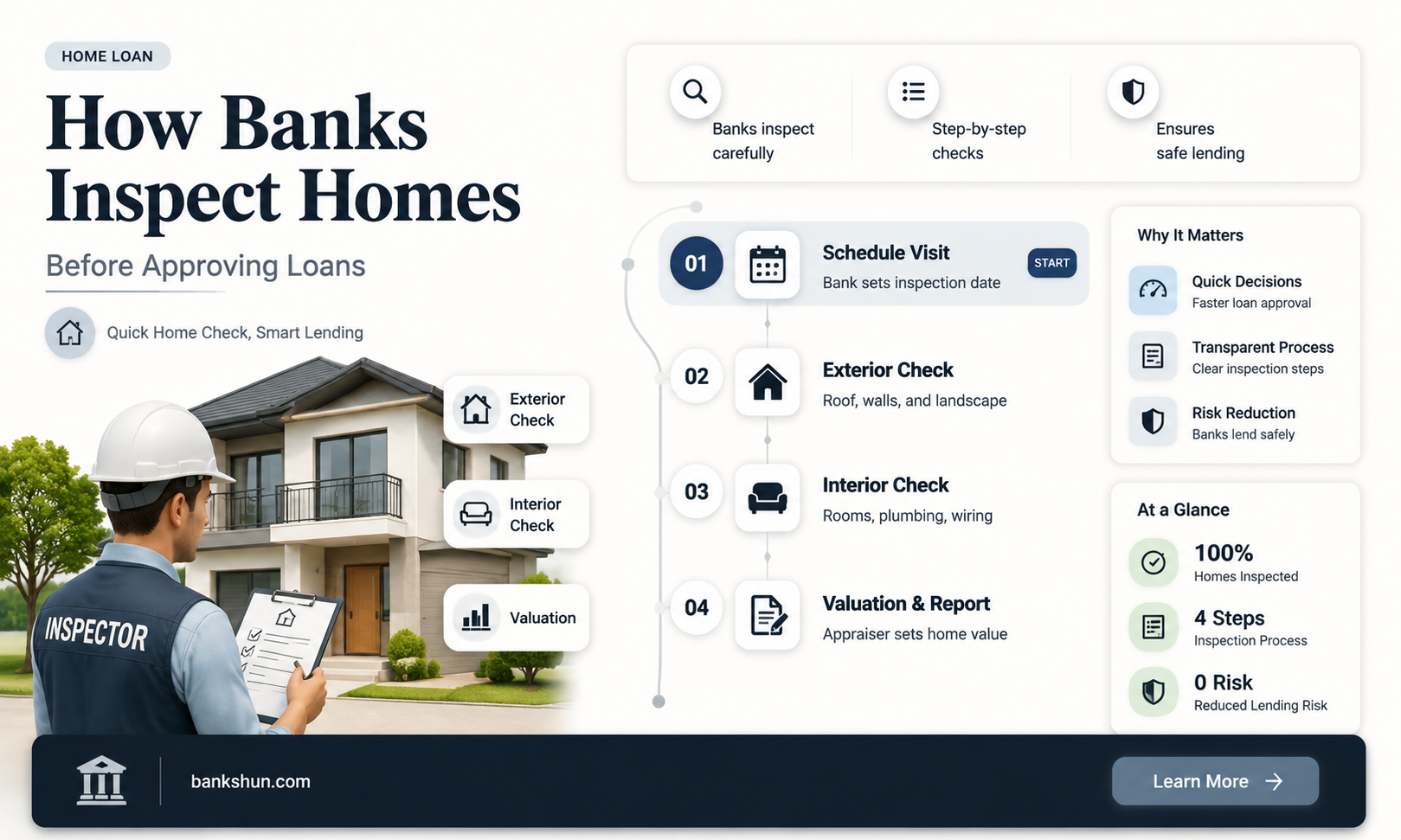

A home inspection is a thorough and objective examination of a house to ensure it is safe, secure, and habitable. Typically, a home inspection is not required by mortgage lenders, but it is highly recommended to uncover any hidden issues. A home inspection is necessary when buying a home, and it is wise to consider getting one even if your lender does not demand one. In the case of mortgages backed by government agencies, such as the Federal Housing Administration (FHA), both home inspections and appraisals are typically required. Lenders may also request an inspection if they believe a property has the potential to fall below its appraised value or if there are concerns about the landlord's financial situation. Commercial landlords are also subject to inspections by lenders to ensure their investment is being maintained.

| Characteristics | Values |

|---|---|

| Purpose of inspection | To ensure the bank's investment is being taken care of and to assess the risk associated with the loan |

| Who initiates the inspection | The bank or the lender |

| When is it done | Periodically, even after the mortgage is secured |

| Who gets inspected | Commercial landlords or tenants in rented properties |

| Inspection duration | 2-4 hours, depending on the size of the home |

| What is inspected | Interior and exterior of the house, basic structure, systems, plumbing, electrical systems, appliances, doors, windows, chimneys, vents, etc. |

| What is not inspected | Sewage systems, recreational facilities, seasonal additions to the house |

| Who conducts the inspection | A licensed home inspector, general contractor, or buyer representative |

Explore related products

What You'll Learn

![]()

Banks may inspect to ensure their investment is protected

Banks may require home inspections to ensure their investment is protected. This is particularly true for commercial landlords, where inspections are common. Banks may also require inspections for rented properties, to ensure that the property is being maintained to a standard that will protect the bank's investment if the landlord defaults on the loan.

Inspections are also common for mortgages backed by government agencies, such as the Federal Housing Administration (FHA). FHA inspectors may review the location and structure of the property to determine its market worth. They will also assess whether the property meets health and safety standards.

Mortgage lenders generally don't require a home inspection, but they may ask for one in rare cases, especially if there are potential issues with the property. For example, if there is a risk of wood-destroying organisms like termites, or if there are structural defects. Lenders want to ensure they are not originating a home loan that is too risky.

Home inspections are a wise move for buyers, as they can uncover hidden issues with a property, such as mechanical, plumbing, or pest problems. They can also highlight potential future problems and give buyers an upper hand in negotiations if issues are found.

Israel's Assault on West Bank: Understanding the Conflict

You may want to see also

Explore related products

![]()

A home inspection is not always required for a mortgage

A home inspection is not always mandatory when applying for a mortgage, but it is highly recommended. While a home inspection is necessary when buying a home, mortgage lenders generally only require an appraisal report to assess the home's value and market worth. This evaluation is not as comprehensive as a home inspection, which covers the property's structural integrity, plumbing, electrical systems, and potential safety risks.

The need for a home inspection depends on factors such as the mortgage type, lender guidelines, and state regulations. Mortgages backed by government agencies, such as the Federal Housing Administration (FHA), typically require both home inspections and appraisals. FHA inspectors may review the location and structure to determine the property's market worth. On the other hand, conventional loans do not usually mandate a home inspection as part of the loan approval process.

Lenders offering conventional mortgages still have certain requirements to ensure the property is a sound investment. While an appraisal evaluates the property's value, a home inspection focuses on its state for the buyer's advantage. A home inspection can uncover hidden issues, such as mechanical, plumbing, and pest problems, and identify potential future problems. It can also provide buyers with leverage in price negotiations if significant issues are found.

In some cases, lenders may urge an inspection if they foresee potential problems. Factors such as the age of the property, location, and loan type specifics may prompt a closer look. Additionally, state laws can influence whether lenders require a home inspection, as some states have regulations mandating specific types of property assessments for real estate transactions.

Although not always required, opting for a home inspection can provide peace of mind and help buyers make informed decisions about their future homes. It is essential to consider the long-term advantages of investing in an inspection to align with financial objectives and ensure confidence in the property's integrity.

Capital One Cafe Banks: Where Are They Located?

You may want to see also

Explore related products

![]()

An inspection can uncover hidden issues like plumbing and pests

A home inspection is generally not required by lenders or banks when applying for a mortgage. However, it is highly recommended to schedule an inspection before proceeding with the mortgage application. This is because an inspection can uncover hidden issues like plumbing and pest problems, which can help buyers avoid costly repairs down the line.

Plumbing issues can range from minor leaks to severe problems that require the entire system to be replaced. Inspectors may note minor issues, such as a leaky faucet or a hose not being tightened, which can be easily fixed. However, if left unchecked, these minor issues can lead to bigger problems, such as water damage, which can be very costly to repair. Inspectors may also flag the presence of certain types of pipes, such as Polybutylene Plastic supply pipes, which are prone to leaks and failures.

Pest issues, such as termites, can also be uncovered during a home inspection. Termites can cause severe damage to wooden structures, and the average cost of remediation is $1,000 to $10,000. A separate pest control report may be required to certify that the property is free from destructive organisms like termites and fungi.

In addition to plumbing and pest issues, a home inspection can also reveal electrical issues, roofing problems, and structural defects. A home inspector will provide a written summary of the inspection and inform the client of any issues found. This report can be used to negotiate with the seller to fix the issues or lower the price of the home.

While a home inspection is not always required by banks or lenders, it is a valuable tool for buyers to ensure they are fully aware of any potential problems with the property. This can help buyers make informed decisions and avoid costly repairs in the future.

Car Title Ownership: Where Does the Bank Stand?

You may want to see also

Explore related products

![]()

A lender may request an inspection if a property is older

A bank or lender may request a home inspection for a variety of reasons. While it is not a requirement for mortgage approval, lenders may request an inspection to assess the risk associated with the loan, determine the property's current market value, and verify the information provided by the borrower. This is particularly common in Section 8 housing and commercial properties.

Lenders may also request an inspection if there is documentation indicating that repairs or inspections were previously done, as they will want to ensure that any issues have been addressed. In some cases, lenders may require additional repairs to be made by a licensed contractor, which can delay the closing process.

Older homes, in particular, may be subject to a lender-requested inspection due to potential issues with septic tanks, asbestos, or other environmental hazards that could affect the property's value. If a lender believes that a property has the potential to fall below its appraised value, they may not approve the mortgage. In such cases, a home inspection report can be used to lower the selling price or negotiate with the seller.

Additionally, lenders may perform periodic inspections of rented properties to ensure that the property is being maintained according to their standards, especially if the landlord is in a financially precarious situation. These inspections help to protect the bank's investment and maintain the value of the property in case the landlord defaults on the loan. Overall, while not always required, home inspections are highly recommended before finalizing a mortgage application to uncover any hidden issues and ensure a fair purchase price.

Purchasing Debt: A Guide to Buying Debt from Banks

You may want to see also

Explore related products

![]()

A bank may inspect a property long after a mortgage is secured

Lenders want to ensure their investment is being taken care of, and inspections help them assess the risk associated with the loan and verify the information provided by the borrower. While a home inspection is not always mandatory when applying for a mortgage, it is highly recommended to uncover any hidden issues, such as mechanical, plumbing, or pest problems. This can also give buyers an upper hand in negotiations if significant problems are found.

In some cases, lenders may ask for a home inspection based on factors such as the property's age, location, or potential issues. For example, if there are concerns about wood-destroying organisms like termites, a Wood-Destroying Organisms (WDO) report may be requested. Additionally, government-backed mortgages, such as those from the Federal Housing Administration (FHA), typically require both home inspections and appraisals.

Appraisals provide an unbiased professional opinion of a home's value, while inspections focus on its state for the buyer's advantage. Although they are different, an appraisal may sometimes highlight issues that would also be discovered in a home inspection. Ultimately, whether it is a bank inspection or an appraisal, the goal is to ensure that the property is worth the money and that the loan is not too risky for the lender.

Alissa and FaZe Banks: Relationship Status Update

You may want to see also

Frequently asked questions

No, banks do not require a home inspection, as they only care about the home's market value. However, they may require a home appraisal to determine the home's value and whether it is a risky investment.

A home inspection is recommended to uncover any hidden issues with the property, such as mechanical, plumbing, or pest problems. It can also be used as leverage to negotiate a lower selling price.

A home inspection is typically performed after an accepted offer to purchase has been signed. It is recommended to include an inspection clause in the sales contract, making the final purchase contingent on the findings of the inspection.