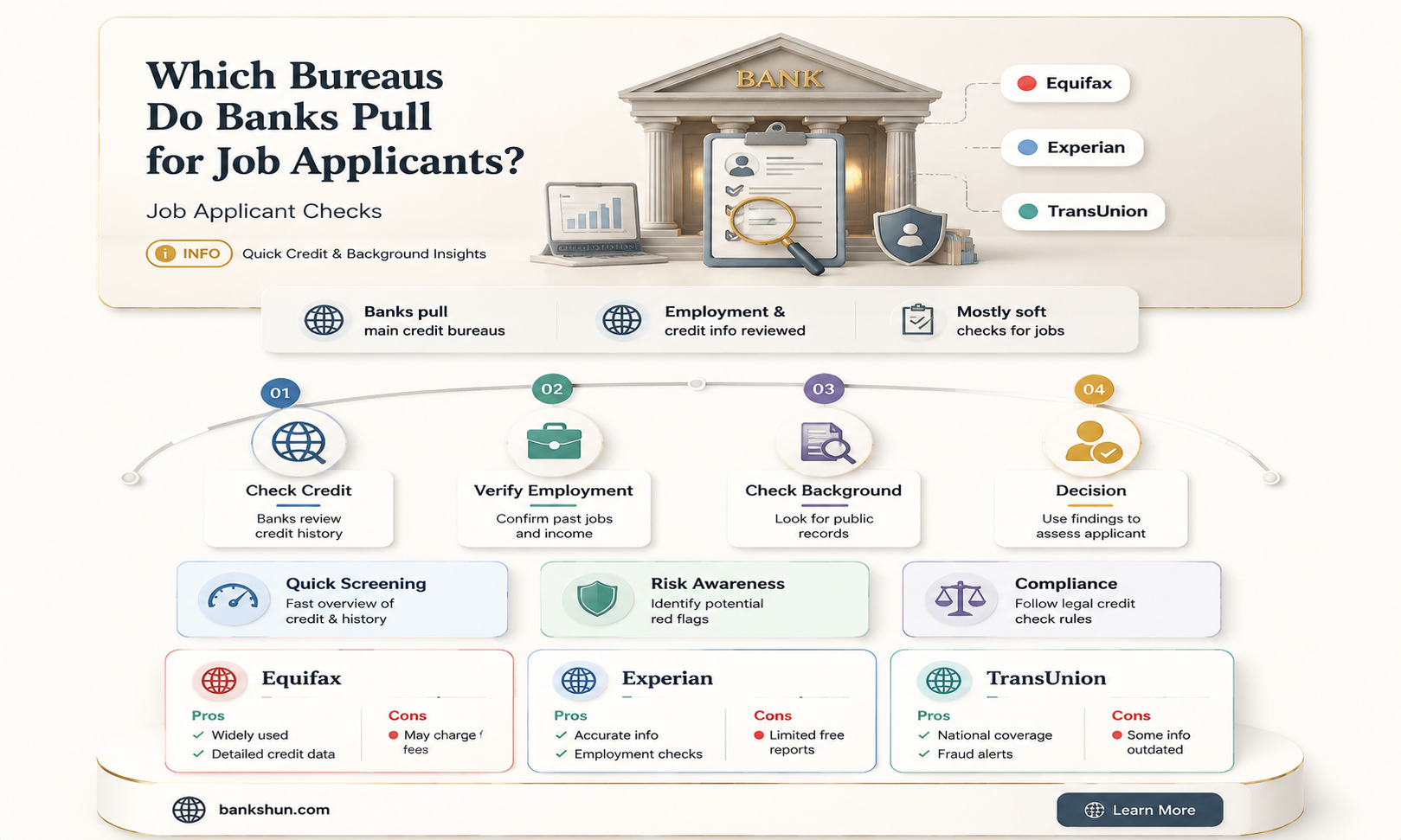

When applying for a job at a bank, it's important to be aware that banks will often review your credit report as part of their hiring process. This is because your credit report provides a detailed record of your credit history, which can be a factor in assessing your suitability for a position, particularly those involving handling finances. In the US, there are three major credit bureaus or credit reporting agencies: Equifax, Experian, and TransUnion. Different banks may have preferences for which bureau they use, and it can also vary depending on the state and the specific position you're applying for. Knowing which bureau a bank uses can help you time your applications to increase your approval odds. While your credit report is a significant factor, banks also consider other aspects of your application, such as your skills, experience, and qualifications.

| Characteristics | Values |

|---|---|

| Number of credit bureaus in the U.S. | 3 |

| Names of the credit bureaus | Equifax, Experian, TransUnion |

| Credit bureaus used by Citi | Equifax, Experian, TransUnion |

| Credit bureaus used by American Express | Equifax, Experian, TransUnion |

| Credit bureaus used by Chase | Equifax, Experian, TransUnion |

| Credit score models used by credit bureaus | FICO, VantageScore |

Explore related products

![]()

Credit card applications

When applying for a credit card, the card issuer will pull a credit report from one or more of the three major credit bureaus—Equifax, Experian, and TransUnion—to determine your creditworthiness. A good credit score indicates that you are reliable with payments and a lower-risk investment, while a poor credit score may lead to higher interest rates or a rejected application.

Some card issuers, such as Capital One, pull credit reports from all three bureaus, while others, like Chase, primarily rely on Experian. Issuers may also consider your location when deciding which bureau to use. For instance, Wells Fargo typically pulls Experian credit reports but may also pull from Equifax in some states.

It's important to note that multiple credit applications in a short period can result in hard inquiries, potentially lowering your credit score and reducing your approval odds. Therefore, it's advisable to check your credit score and reports before applying for a credit card. Additionally, some card issuers offer pre-screening, pre-qualification, or pre-approval tools to help you assess your eligibility before performing a hard credit pull.

PNC Banks in Clermont, Florida: Locations and Services

You may want to see also

Explore related products

![]()

Credit scores

Some employers perform credit checks on potential hires, especially for roles that involve handling money or accessing private consumer data. However, it is important to note that employers do not have access to an individual's credit score. Instead, they can request a modified credit report that excludes certain information, such as age and credit score. This report includes details about debt, payment history, credit accounts, bankruptcies or liens, and certain work history.

The practice of employer credit checks is controversial, with critics arguing that it harms individuals who are building their credit or recovering from financial setbacks. It is also said to disproportionately impact minority job seekers and low-income workers, who tend to have lower credit scores and more late payments or accounts in collections.

Individuals can request a free credit report from each of the three main credit bureaus (Experian, Equifax, and TransUnion) once a year to review their financial history and address any discrepancies. Additionally, some personal finance websites offer free credit reports and scores that can be monitored regularly.

Local vs. Big Banks: Which is the Better Choice?

You may want to see also

Explore related products

![]()

Credit history

Credit checks are sometimes part of a job application screening process. A credit check for employment involves employers checking a modified version of an applicant's credit report or financial history. This includes credit accounts, payment history, debts, bankruptcies or liens, and certain work history. However, it does not include the applicant's credit score or personal information such as age.

Some critics argue that this practice is controversial and can harm certain groups of people, particularly minority job seekers and low-income workers. For example, Black and Latino consumers tend to have lower credit scores as a group due to the racial wealth gap and other forms of discrimination. Similarly, low-income workers are more likely to have late payments or accounts in collections on their credit reports.

In the context of jobs in banks, some sources suggest that a bad credit score or bankruptcy may not affect the hiring of a teller but could be a blocking factor for more senior roles such as personal bankers or upwards. However, other sources suggest that even for senior roles, a poor credit score may not be a deal-breaker and that other factors, such as any criminal history, are more important.

It is worth noting that there are legal restrictions on when an employer is allowed to use a credit check for employment. At the federal level, the Fair Credit Reporting Act (FCRA) outlines specific guidelines that employers must follow when conducting credit checks on prospective employees. Additionally, a handful of states, including California, Colorado, Connecticut, Delaware, Hawaii, Illinois, Maryland, Nevada, Oregon, Vermont, and Washington, have placed further limits on the use of credit checks in employment decisions.

Bank Guarantees: Legal in the United States?

You may want to see also

Explore related products

![]()

Credit bureaus

When applying for a new job at a bank, the bank may request to pull a credit report from one or more of the three major credit bureaus as part of the hiring process. These credit bureaus—Equifax, Experian, and TransUnion—are widely used by employers, credit card issuers, lenders, and consumers for various purposes. While some issuers have a preference for one bureau, others may pull reports from multiple bureaus.

Each credit bureau collects and maintains information about an individual's credit history, including their credit accounts, loans, public records, and credit inquiries. This information is then used to generate a credit report, which provides a detailed overview of an individual's financial history and creditworthiness.

It is important to note that the specific bureau used by a bank may vary depending on the state or region, or the specific position being applied for. Additionally, some banks may use multiple bureaus to gather a more comprehensive understanding of an applicant's credit history. Therefore, while banks do pull credit reports from credit bureaus during the hiring process, the specific bureau utilized may differ in each case.

Jill Wine Banks: A Bookish Insight

You may want to see also

Explore related products

![]()

Creditworthiness

A borrower deemed creditworthy is someone a lender considers financially responsible and reliable enough to make loan payments as agreed until a loan is repaid. Creditworthiness is determined by several factors, including repayment history, credit score, assets, and liabilities. A high credit score means high creditworthiness, while a lower score indicates lower creditworthiness. Credit scores are typically between 300 and 850, with higher scores indicating lower risk.

The Federal Reserve: Government Entity or Independent Actor?

You may want to see also

Frequently asked questions

No. While your credit report is a key part of your financial profile, it is not the only factor that determines your creditworthiness.

A credit bureau is a credit reporting agency that banks and credit card companies can pay to access your credit report. In the US, the three major credit bureaus are Equifax, Experian, and TransUnion.

A credit bureau has detailed information about your credit history, including your credit score. Your credit score is a number between 300 and 850 based on the information in your credit report.

A credit bureau can impact your job application if the employer checks your credit report as part of the hiring process. A negative credit report could indicate financial instability or irresponsible financial behaviour, which may be a concern for certain roles.

Yes, you can research or inquire about the bank's preferred credit bureau. However, keep in mind that some banks may use multiple bureaus or switch between them.