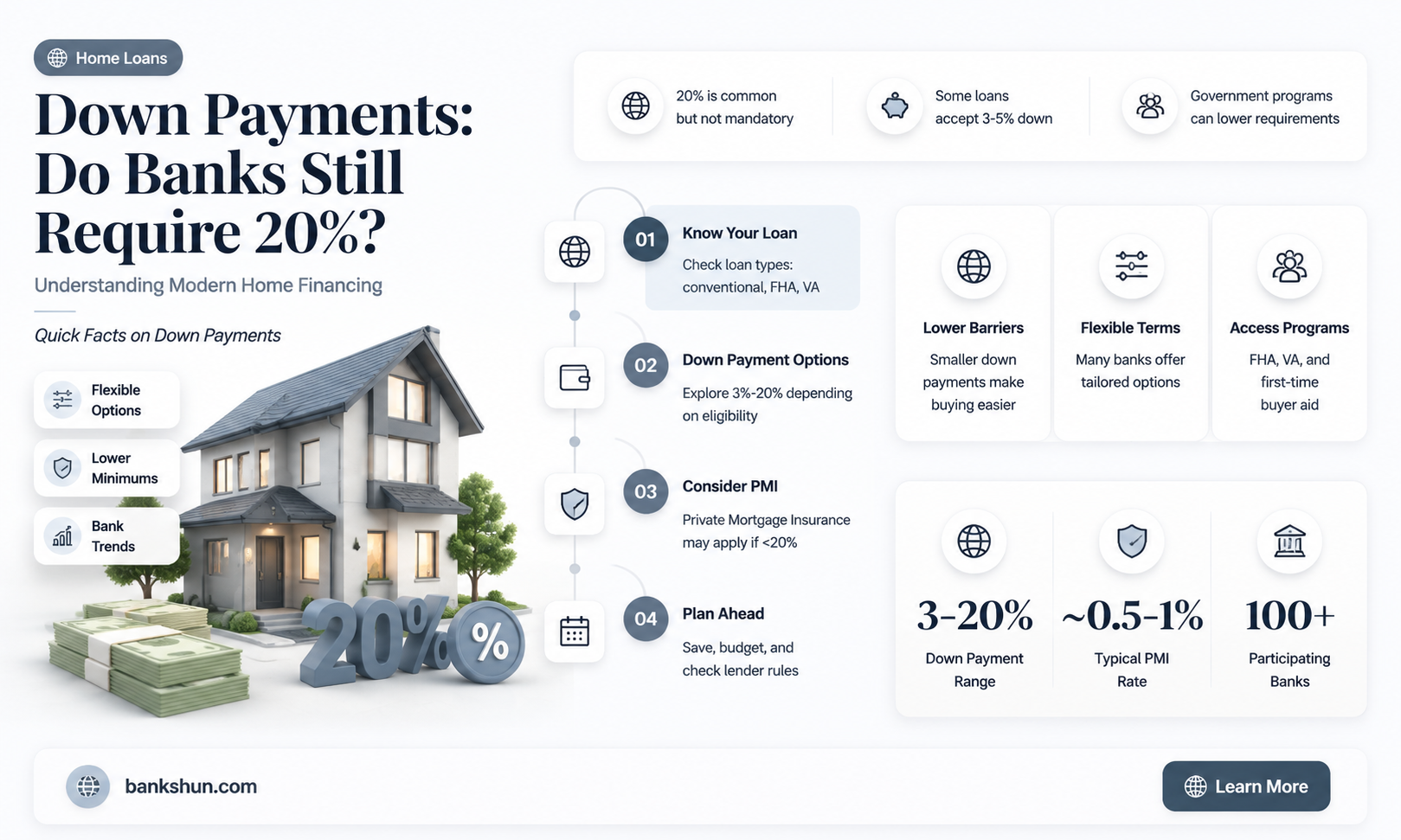

While a 20% down payment is not a requirement for buying a home, it is a widely circulated myth. Financial advisors and real estate experts recommend a 20% down payment to lower the risk of owning a home and build equity. However, this may not always be feasible, and there are several low or no down payment options available for prospective homeowners.

Explore related products

What You'll Learn

![]()

A 20% down payment is not necessary to buy a home

While a 20% down payment was the traditional standard for purchasing a home, it is not a requirement. In fact, many homebuyers are able to secure a home with as little as 3% down payment or even no down payment at all. The amount you need to put down depends on various factors, including the loan type and your financial goals.

The 20% down payment rule is a myth. The average down payment for first-time buyers is between 6% and 13%. There are loan programs that allow you to put down as little as zero. However, a smaller down payment means a more expensive mortgage over the long term, with higher monthly payments and interest rates. With less than 20% down, you will likely have to pay for private mortgage insurance (PMI), which can be expensive.

If you put down less than 20%, you will need to make monthly PMI payments on top of your regular mortgage. These insurance payments can eventually be waived once you've built up 20% equity in your home. However, if you can afford it, a 20% down payment has its benefits. You will have a smaller loan size, lower monthly payments, and no mortgage insurance.

If you don't have a large down payment saved up, there are still plenty of options available. Down payment assistance programs are available from state and local governments to help first-time homebuyers with down payment costs. It's important to consider your financial goals and shop around for the best option.

Central Banks' Stock Market Intervention: What's the Plan?

You may want to see also

Explore related products

![]()

Smaller down payments may require private mortgage insurance

While a 20% down payment is not required to buy a home, smaller down payments often require a few extra steps. Lenders issuing conventional home loans typically require private mortgage insurance (PMI) if the down payment is under 20%. PMI is a type of insurance that protects the lender in case the borrower defaults on the loan. It is an additional monthly cost that is rolled into your mortgage payment and protects only the lender, not you.

PMI can be beneficial for homebuyers as it can help them qualify for a loan that they might not otherwise be able to get. However, it is important to note that PMI does not protect the buyer in any way and can increase the cost of the loan. The cost of PMI is risk-based and varies from state to state and lender to lender. It is calculated as a percentage of the mortgage loan amount and typically ranges from 0.58% to 1.86% annually.

There are ways to make a down payment of less than 20% without paying PMI premiums. One option is to consider a different type of loan, such as an FHA loan, VA loan, or USDA loan, which charge mortgage insurance differently from conventional loans. Another option is to explore special first-time homebuyer loans without PMI. Additionally, once your home's value has increased sufficiently to lower your loan-to-value ratio (LTV) below 80%, you may be able to request PMI cancellation from your lender.

In some cases, it may make sense to put less than 20% down on a house. For example, if you are buying a house that is well below what you can afford, the risk of owning a home is already fairly low. Additionally, if you are in a rising housing market, there is less need to have a large down payment as the house can be expected to increase in value over time, increasing your equity.

FDIC Insurance: Will Banks Lower the Coverage?

You may want to see also

Explore related products

![]()

A larger down payment is recommended in a flat or declining housing market

While a 20% down payment is not required to buy a home, it is a common misconception that persists across age groups and educational levels. Financial advisors and real estate experts often recommend a 20% down payment to lower the risk of owning a home. However, this advice is not always practical, and there are several low or zero-down payment options available for prospective homeowners.

For example, consider a scenario where property values in your local market are decreasing by 10% per year. If you make a 5% down payment, you will have negative equity of 5% in the first year and 15% in the second year. On the other hand, a 20% down payment would give you positive equity of 10% in the first year, even with the market depreciation. This equity position provides a safety net and protects you from potential losses if you need to sell your home in the short term.

Additionally, a larger down payment can lead to a smaller home loan balance, resulting in lower mortgage rates and less interest expense over the life of the loan. It demonstrates your ability to obtain a mortgage, making your offer more attractive to sellers. It also reduces the need for private mortgage insurance (PMI), which is typically required by lenders when the down payment is under 20%.

However, it's important to note that saving for a large down payment can delay your entry into the housing market, especially in a rapidly rising market. It may be challenging to keep up with increasing home prices, and there could be drawbacks, such as the opportunity cost of keeping your money in a low-interest savings account during the saving period. Therefore, it's essential to consider market conditions and your financial circumstances when deciding on the down payment amount.

Citizens Bank Park: Delicious Food, Great Baseball

You may want to see also

Explore related products

![]()

There are many low down payment options for first-time buyers

While financial advisors and real estate experts recommend making a down payment of 20% or more on a house, it is not always necessary. In fact, according to the National Association of Realtors, the median down payment for first-time buyers is 9%. There are several low down payment options available for first-time buyers, especially in the US.

Firstly, the Conventional 97 program allows for a 3% down payment. This program is available from most mortgage lenders and is limited to loan sizes of a certain amount, excluding jumbo-conforming loans. Additionally, it is only available for single-family homes. Another option is the USDA Rural Housing Loan, also known as the Section 502 loan, which is available in both rural and suburban areas and does not require a down payment. For veterans of the US Armed Services, the Department of Veterans Affairs offers a no-money-down VA loan with 100% financing and sensitive underwriting standards that take into account the unique circumstances of military families. FHA loans, such as the CalPLUS FHA program, also offer low down payment options and can be combined with other programs for closing cost assistance.

State and local agencies, nonprofits, and employers also offer various programs to assist first-time homebuyers with down payments. For example, the Bank of America Community Homeownership Commitment® provides affordable mortgages, grant programs, and resources for modest-income and first-time homebuyers. Similarly, Wells Fargo offers low down payment options and grants to assist with down payments and closing costs.

It is important to note that smaller down payments often require additional steps, such as purchasing private mortgage insurance (PMI) to protect the lender in case of default. However, by exploring the different options available, first-time buyers can find low down payment alternatives that fit their financial situation and make homeownership a reality.

World Bank's Move: Laos' Economic Future?

You may want to see also

Explore related products

![]()

A 20% down payment is ideal to avoid mortgage insurance

While a 20% down payment is not mandatory when buying a home, it is often recommended. There are several advantages to a 20% down payment, including avoiding private mortgage insurance (PMI), reducing your loan amount, lowering monthly payments, and providing more financial security and flexibility.

Private mortgage insurance is a type of insurance that lenders commonly require when homebuyers make a down payment of less than 20% of the home's value. This insurance protects the lender in case the borrower defaults on the loan. It is typically added to the monthly mortgage payment, increasing the overall cost of the loan. By making a 20% down payment, you can eliminate the need for PMI and save money in the long run.

However, it is important to note that there are alternative loan options available that do not require a 20% down payment and also avoid PMI. These include government-backed mortgage programs, such as FHA loans, VA loans, USDA loans, and jumbo loans, which charge mortgage insurance differently from conventional loans. Additionally, some lenders offer loan products without PMI, but they may charge higher interest rates.

The decision to make a 20% down payment depends on various factors, including your financial situation, the housing market trends, and your ability to qualify for different loan programs. If a 20% down payment would deplete your savings, you may consider a smaller down payment option that allows you to keep funds for emergencies, home repairs, or other expenses.

In a flat or declining housing market, a large down payment is generally recommended to lower the risk of owning a home. On the other hand, in a rising housing market, the need for a large down payment is reduced, as the home's value is expected to increase over time, building equity without requiring a higher initial investment.

Green Dot's Banking Partners: Who's Behind the Scenes?

You may want to see also

Frequently asked questions

No, not all banks require a 20% down payment on a house. While it is a common misconception, there are many options for lower-down-payment home loans.

A 20% down payment provides a comfortable equity cushion, lowers the risk of owning a home, reduces the loan amount, and lowers monthly payments.

Yes, there are several alternatives to a 20% down payment. First-time buyers, on average, put down only 13%. There are also government-backed mortgage programs that allow for down payments of less than 5%. Additionally, certain loans, such as VA loans and USDA loans, do not require any down payment.

A lower down payment may result in higher monthly payments and the need for private mortgage insurance (PMI), which increases the overall cost of the loan.