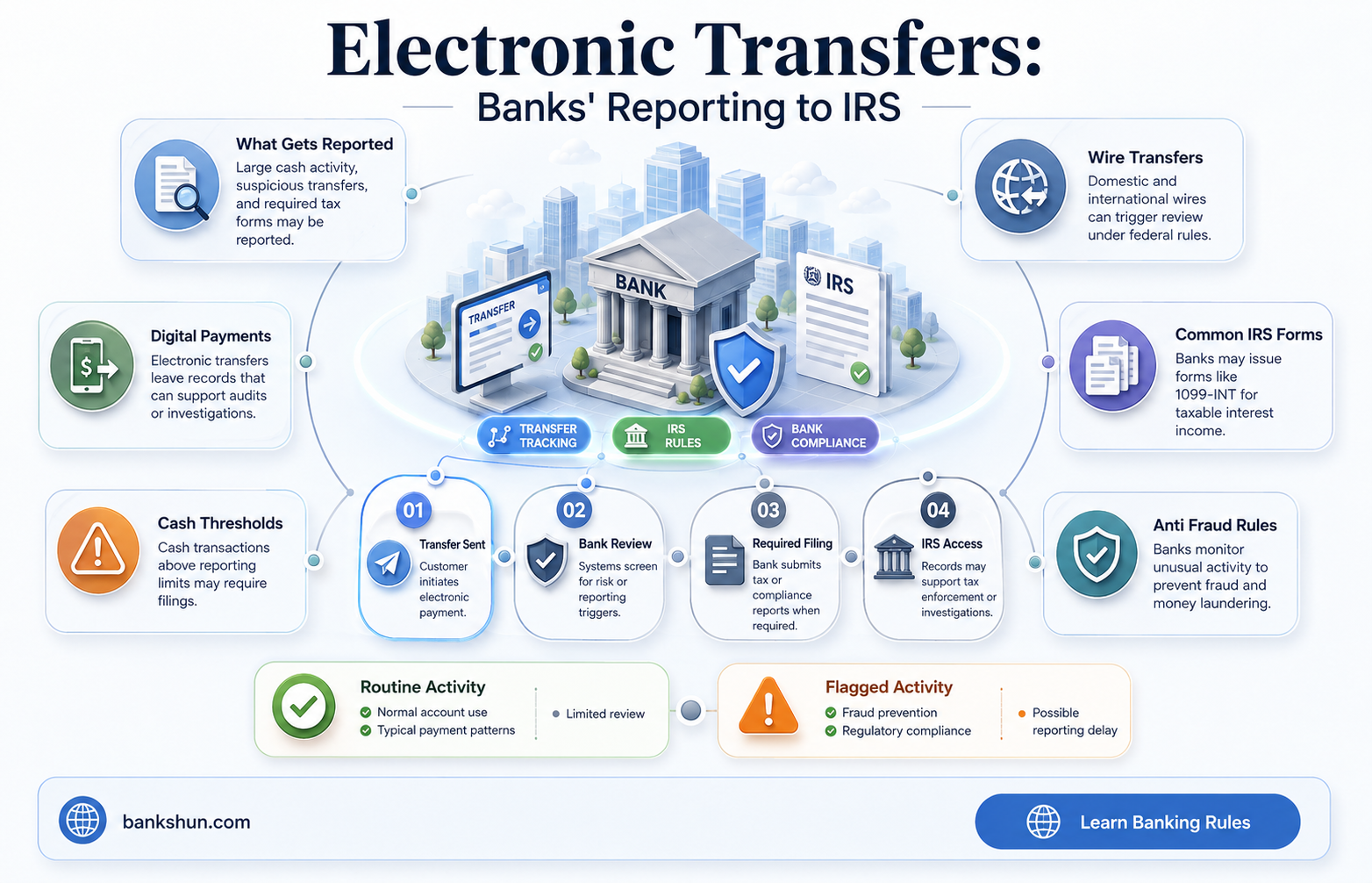

Banks generally do not report most transactions or balance information to the IRS unless they are specifically asked to do so. However, under the Bank Secrecy Act (BSA) of 1970, financial institutions are required to report certain transactions, including wire transfers over $10,000. This is done through a Currency Transaction Report (CTR), which includes details about the transaction's nature and the parties involved. The purpose of this requirement is to prevent money laundering and other criminal activities. Additionally, banks must report cash or cashier's check deposits exceeding $10,000 and any interest income they have paid to customers. While Zelle transfers are not reported on 1099-Ks, there is a proposal for increased bank reporting requirements, which would include total inflows and outflows for accounts with at least $10,000 in transactions.

| Characteristics | Values |

|---|---|

| Reporting of electronic transfers by banks | Banks generally do not report most transactions or balance information to the IRS unless specifically requested. |

| Reporting requirements | Banks must report cash or cashier's check deposits or withdrawals of more than $10,000. |

| Suspicious activity | Banks must report suspicious activity, particularly in excess of $5,000. |

| Zelle transfers | Zelle transfers are not reported on 1099-Ks as Zelle does not have custody of the funds and only transfers money between accounts. |

| Wire transfers | Wire transfers over $10,000 are subject to reporting under the Bank Secrecy Act (BSA) and the Currency and Foreign Transactions Reporting Act. |

| Currency Transaction Report (CTR) | Financial institutions must file a CTR for any transaction over $10,000, which includes information about the person initiating the transaction, the recipient, and the nature of the transaction. |

| Purpose of reporting | To prevent money laundering, tax evasion, and other criminal activities. |

Explore related products

What You'll Learn

![]()

Banks report electronic transfers over $10,000 to the IRS

Banks are required to report electronic transfers over $10,000 to the IRS under the Bank Secrecy Act (BSA) of 1970. This act mandates that financial institutions file a Currency Transaction Report (CTR) for any transaction exceeding $10,000. The CTR includes details about the person initiating the transaction, the recipient, and the nature of the transaction. The purpose of this legislation is to prevent money laundering and other criminal activities, such as tax evasion and terrorist financing.

It is important to note that banks do not routinely report most transactions or balance information to the IRS. However, they are required to report cash or cashier's check deposits, and any interest they have paid on a customer's balance. Additionally, if a customer makes structured deposits or withdrawals of smaller amounts to evade reporting requirements, the bank must report this as a suspicious activity.

While wire transfers over $10,000 are generally subject to reporting, there are some exceptions. For instance, transactions conducted by financial institutions on behalf of the US government or between financial institutions are not reported.

The IRS also receives information about transactions through other means, such as when a business reports cash receipts greater than $10,000 in a single transaction or related transactions using Form 8300. This form is used to report cash transactions over $10,000 and helps law enforcement combat various financial crimes.

Overall, while banks do report electronic transfers over $10,000 to the IRS, they do not routinely report all transactions. The reporting is primarily aimed at preventing financial crimes and ensuring compliance with tax laws.

Huntington Bank's Main Branch Location and Address

You may want to see also

Explore related products

![]()

International wire transfers are monitored by the IRS

The IRS requires financial institutions and money transfer providers to report international transfers that exceed a certain threshold, which is typically $10,000. This reporting requirement helps the IRS keep track of large sums of money moving across borders and can be done by the bank or money transfer service. If you are sending or receiving amounts above this threshold, it is your responsibility to report the transfers to the IRS. Failing to do so can result in fines and legal consequences.

In addition to the reporting requirements, the IRS also imposes tax obligations on certain international wire transfers. Any amount over $16,000 sent to a foreign bank account may be considered a taxable gift by the IRS. This means that you may need to pay taxes on the transferred amount. However, this may not apply if you are sending money to an overseas account in your own name. It is important to note that tax laws can be complex, and seeking specialist tax advice is recommended before making a large international wire transfer.

The Foreign Account Tax Compliance Act (FATCA) is another important piece of legislation related to international wire transfers. FATCA requires foreign financial institutions and non-financial entities to report all foreign accounts and assets held by US citizens. This helps the IRS identify individuals with financial activities outside of the US and ensure proper tax compliance.

It is worth noting that while the IRS closely monitors international wire transfers, the primary goal is to detect and prevent illegal activities. As long as individuals and businesses comply with the reporting requirements and tax obligations, they can confidently use international wire transfers as a convenient way to send and receive money globally.

Fishers Stores: US Banks Accessibility and Availability

You may want to see also

Explore related products

![]()

Transfers to foreign accounts over $16,000 are taxable

Banks are required to report electronic transfers over $10,000 to the Internal Revenue Service (IRS). This is to monitor international wire transfers and combat money laundering, tax evasion, drug dealing, terrorist financing, and other criminal activities.

If you are sending an international wire transfer over $10,000, your bank or financial institution will report it directly to the IRS. This is a legal requirement for US banks and other financial institutions that initiate wire transfers. It is important to note that the transfer itself is not taxable, but if the funds come from income, investments, or gifts, there may be tax obligations.

Now, if the transfer exceeds $16,000 and is sent to a foreign bank account, it is likely to be considered a taxable gift by the IRS. This means that the recipient of the transfer may be subject to the gift tax, which can range from 18% to 40% if the lifetime gifts exceed $12,920,000. However, this may not apply if you are sending the money to an overseas account in your own name. Additionally, if you have foreign financial assets worth at least $50,000, you must report them to the IRS along with your annual income tax return.

To ensure compliance with tax laws, it is recommended to seek specialist tax advice when planning to make a large payment overseas. This will help you understand your specific obligations and avoid potential legal repercussions, fines, or penalties.

Physical Banks: More Likely to Lend?

You may want to see also

Explore related products

![]()

Banks report deposits and withdrawals over $10,000

Banks are required to report any cash deposits or withdrawals over $10,000 to the Internal Revenue Service (IRS) within 15 days of the transaction. This is done by filing a Currency Transaction Report (CTR) or Form 8300. Form 8300 is used to report cash payments over $10,000 received in a trade or business, and it must be filed by both the bank and the individual or business making the transaction. The form can be filed electronically through the Financial Crimes Enforcement Network's BSA E-Filing System or by mail.

The requirement for banks to report large cash transactions is set by the Bank Secrecy Act, also known as the Currency and Foreign Transactions Reporting Act. The purpose of this legislation is to help the government monitor financial transactions that may be indicative of illegal activity, such as money laundering, purchases of illegal goods, or terrorism. While the $10,000 threshold specifically applies to cash transactions, banks are also required to report any suspicious transactions, including deposit patterns below $10,000.

In addition to cash deposits and withdrawals, banks must also report cash purchases of certain financial instruments, such as cashier's checks, treasurer's checks, bank drafts, traveler's checks, and money orders, with a face value of more than $10,000. This is done to prevent individuals from structuring transactions to avoid the $10,000 reporting threshold.

It is important to note that the reporting requirements may vary for different types of organizations. For example, tax-exempt organizations are generally not required to file Form 8300 for charitable cash contributions. However, they may need to report non-charitable cash payments over $10,000, such as rent received for their properties.

While individuals are not required to report wire transfers over $10,000 to the IRS, banks are responsible for reporting these transactions. Therefore, it is important to be aware that large transactions may trigger a review or audit of your financial records by the IRS.

AHC in Banking: What Does It Mean?

You may want to see also

Explore related products

![]()

Banks must report suspicious activity over $5,000

Banks and other financial institutions must report cash purchases of cashier's checks, treasurer's checks, bank checks, bank drafts, traveller's checks, and money orders with a face value of more than $10,000 by filing currency transaction reports. This is done by filing Form 8300, which provides valuable information to the Internal Revenue Service (IRS) and the Financial Crimes Enforcement Network (FinCEN) in their efforts to combat money laundering, tax evasion, drug dealing, terrorist financing, and other criminal activities.

Form 8300 must be filed when a person receives cash of more than $10,000 from the same payer or agent in a single lump sum or in two or more related payments within 24 hours. It is also required when multiple related transactions occur within a 12-month period, with each set of payments exceeding $10,000. For example, a car dealership does not need to file Form 8300 if a customer pays with a $7,000 wire transfer and a $4,000 cashier's check. However, if a customer purchases a vehicle for $9,000 in cash and later pays $1,500 in cash for accessories within 12 months, the dealer must file Form 8300 if the accessory purchase is related to the original vehicle purchase.

In addition to Form 8300, a written statement must be provided to each party whose name is included on the form by January 31 of the following year. This statement includes the name, address, contact person, and telephone number of the business, along with the aggregate amount of reportable cash. It is important to note that the statement must also indicate that this information has been furnished to the IRS.

While the focus is on cash transactions over $10,000, the IRS encourages voluntary reporting of suspicious activity, regardless of the dollar amount. This can be done by filing Form 8300 for transactions below $10,000, without notifying the customer. Additionally, casinos and card clubs must file a Suspicious Activity Report (SAR) for any suspicious transaction that may involve a violation of law or regulation, involving funds or assets of at least $5,000.

Therefore, while the threshold for reporting cash transactions is generally $10,000, banks and financial institutions must also report suspicious activities involving smaller amounts, specifically transactions over $5,000 that meet certain criteria, to the IRS.

Are You Allowed to Bring Battery Banks on Delta Flights?

You may want to see also

Frequently asked questions

Banks generally do not report electronic transfers to the IRS unless the transfer amount exceeds $10,000. In such cases, banks are required to file a Currency Transaction Report (CTR) under the Bank Secrecy Act. Additionally, banks may report transactions if they suspect any illegal activity or if the IRS specifically requests information during an audit.

Banks typically report cash or cashier's check deposits or withdrawals of more than $10,000. They may also report any interest paid to you on your balance (Form 1099-INT, Interest Income). Banks are mandated to report suspicious activity, especially if it involves large sums of money.

Yes, there are a few exceptions. Banks are not required to report transactions conducted by financial institutions on behalf of the US government or transactions between financial institutions. Additionally, certain payment services, such as Zelle, do not report transactions on 1099-Ks as they only transfer money between bank accounts without taking custody of the funds.