Bank transfers are a quick, safe, and reliable way to send money, but sometimes they can be delayed or need to be reversed. There are several reasons why a bank transfer may be delayed, including incorrect payment details, compliance checks, and varying processing speeds between banks. International transfers can be especially prone to delays due to intermediary banks and differing regulatory requirements. While it is difficult to reverse a bank transfer once the recipient has accepted it, there are rare cases where it can be done, usually due to errors on the bank's part. In the US, ACH transfers and wire transfers are the two main types of bank transfers, with ACH transfers typically being slower but more commonly used for commercial transactions.

| Characteristics | Values |

|---|---|

| Can bank transfers be reversed? | Yes, but only in specific circumstances, such as incorrect account numbers or duplicate transfers. |

| Time limit for reversal | Within 30 minutes for international remittance, according to the Dodd-Frank Wall Street Reform and Consumer Protection Act. |

| ACH returns | Can be returned within 2 days for commercial accounts and 60 days for consumer accounts. |

| ACH transfer networks | Nacha, FedACH, Fedwire, CHIPS |

| Delays | Possible due to compliance checks, exchange rates, cut-off times, holiday schedules, weekend closures, time zones, and intermediary banks. |

Explore related products

What You'll Learn

![]()

Bank transfer errors and reversals

Bank transfers are a popular and convenient way to transfer money between financial institutions. However, mistakes can happen, and sometimes, the sender or recipient may need to reverse the transfer.

If you notice something incorrect after submitting an authorization request, you can call your bank to stop the transaction from occurring. This is known as an authorization reversal. It is preferable over a future chargeback or refund. The earlier you catch the error, the better your chances of reversing the transaction.

If the transfer has already gone through, it is possible to initiate a wire transfer reversal by the bank to reject the transaction. However, if the money was sent to the wrong account and not dismissed, nothing can be done. If the recipient's bank has already accepted the order, it is too late to reverse it.

There are some circumstances in which disputing a wire transfer is possible, and they usually relate to an error on the bank's part, such as:

- A mistake in the account number

- A duplicate transaction

- The beneficiary received more than the entitled amount

ACH (Automated Clearing House) transfers can be reversed under specific circumstances, typically within 1-5 business days. Reversals require valid justification and proper documentation. The receiving bank and account holder can dispute the reversal request, making recovery uncertain.

To prevent mistakes, it is important to double-check all information, including the recipient's name, bank account number, and routing number. Confirm the details of the wire transfer with the sender before initiating the transfer. Use a secure and reputable bank or money transfer service to initiate wire transfers to prevent fraudulent activity.

International bank transfers may take longer due to the involvement of intermediary banks, compliance checks, exchange rates, and varying cut-off times, holiday schedules, and time zones.

Which Banks are in Trouble and Why?

You may want to see also

![]()

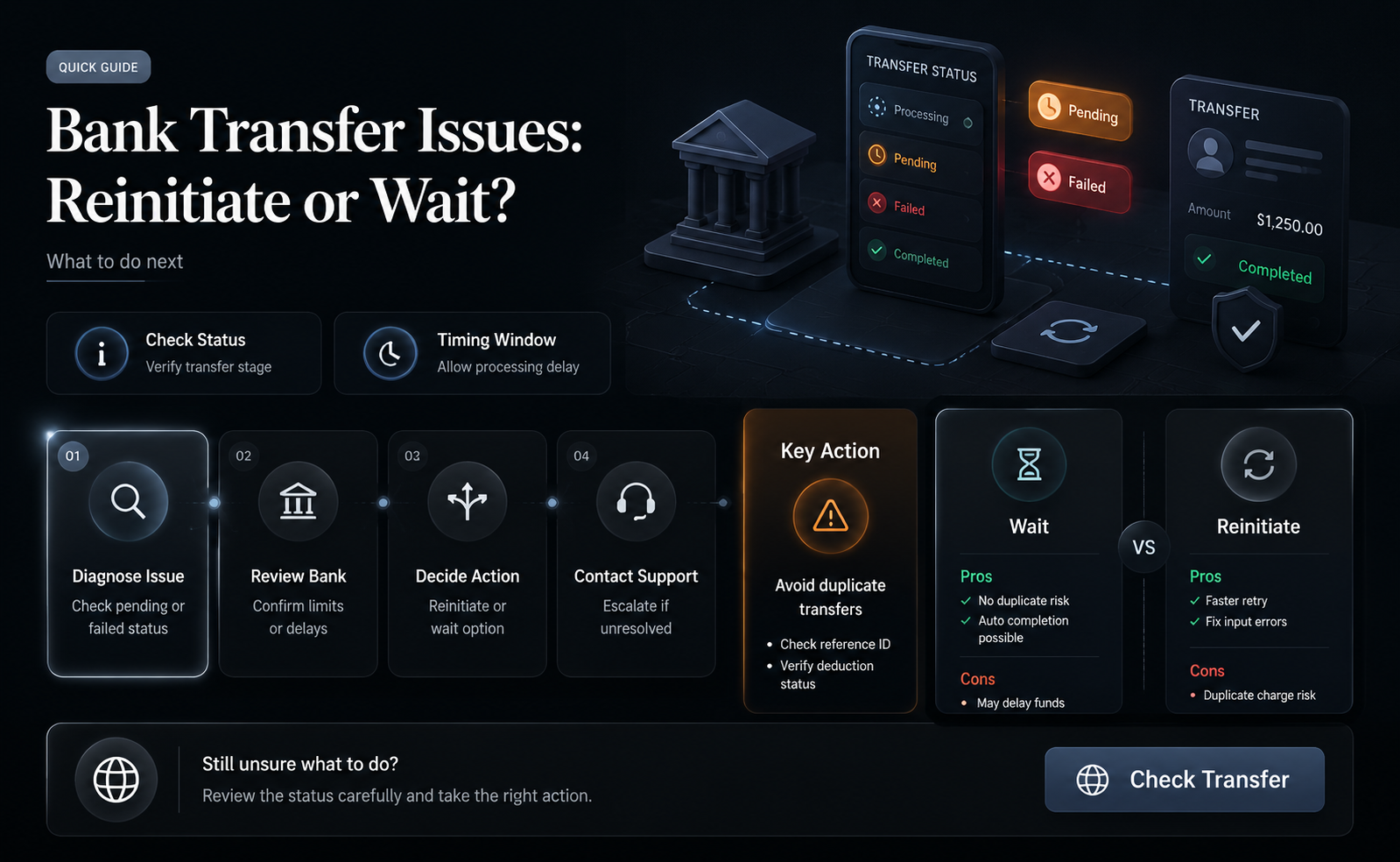

Time limits for reinitiating transfers

When it comes to reinitiating bank transfers, there are time limits and specific circumstances that apply. Generally, bank transfers can take anywhere from one to five business days to be completed, depending on the method used and the institutions involved.

For ACH transfers, there is a specific timeframe within which reinitiating transfers must occur. According to Nacha rules, a returned transfer can only be reinitiated within 180 days of the original transfer's settlement date. This timeframe ensures that the resolution remains within the ACH network. After this 180-day period, any issues must be addressed outside of the ACH network.

For corporate accounts, ACH debits can typically be returned within two business days, while consumer accounts have a 60-day window for returns. These timeframes may be extended in cases where an ACH debit is disputed as unauthorized, allowing the originating bank to request proof of authorization.

It's important to note that wire transfers are typically quick and challenging to reverse once completed. While there are rare instances where wire transfers can be reversed due to errors or fraud, the process is generally not guaranteed.

Additionally, Bank of America provides specific cutoff times for transfers. Transactions made before 10:45 pm ET on a business day will reflect the same day's date, while transfers made after this time will be included in the next day's transaction history. Transfers initiated on weekends or bank holidays will also reflect the next business day's date.

Monthly Bank Fees: Who Charges and How Much?

You may want to see also

![]()

International bank transfer requirements

International bank transfers can be quick, safe, and reliable, especially for large transactions, as the funds are made available to the recipient right away. However, there are several requirements that must be met to ensure a smooth transfer.

Firstly, it is crucial to gather accurate information about the recipient. This includes the recipient's name, address, bank name, SWIFT BIC, bank account number, and the International Payments System Routing Code, if applicable. Providing incorrect recipient details often results in delays or even failed transfers.

Secondly, the sender must ensure they have the necessary information and access to perform the transfer. For online transfers, this may include enrolling in a secured transfer service, providing a mobile number, and setting up two-factor authentication with an authorization code. Additionally, the sender's debit card number and PIN may be required to initiate the transfer.

Thirdly, international transfers often involve intermediary banks, especially when transferring to less common countries or when dealing with less connected banking systems. These third-party banks may have their own cut-off times, holiday schedules, weekend closures, and time zones, which can impact the transfer's speed. Additionally, each intermediary bank will conduct compliance checks and apply their exchange rates, potentially affecting the overall cost of the transfer.

Finally, it is important to be aware of the time limitations on cancelling or reversing international transfers. While some banks allow transfers to be cancelled within a certain timeframe (such as 30 minutes) after initiation, others consider transfers final and irreversible once they have been processed. Therefore, it is crucial to verify the details and act promptly in case of any issues.

International Bank Transfers: How Long Do They Take?

You may want to see also

![]()

Delays caused by incorrect payment details

Bank transfers can be delayed due to several factors, including incorrect payment details, which can cause significant hold-ups. Entering incorrect payment details can result in the payment being sent back or requiring manual correction by the bank. This often involves contacting the sender or recipient for clarification, which can delay the transfer process. To avoid such delays, it is essential to verify the recipient's account number, name, and bank information.

Incorrect account information, such as an invalid account number or routing number, is a common issue that can lead to delays. Banks may need to manually correct the error, and the transaction may be subject to additional security checks and algorithms. In some cases, a single typo in the recipient's account information can cause the transfer to fail to pass through the automated systems, necessitating manual intervention.

Another factor contributing to delays is incomplete account information. This could include a mismatch between the name of the sender and the beneficiary, especially when paying into a business account. Banks may flag such discrepancies and send the transfer for review, causing a delay in the processing time. Therefore, it is crucial to ensure that all details match the receiving bank's records to avoid investigations or corrections that may prolong the transfer.

International transfers also present challenges due to currency conversion delays. Banks may take extra time to convert currencies, especially if they are less liquid or require additional regulations. Moreover, the exchange rate between currencies can fluctuate, leading to potential discrepancies in the received amount. These factors can cause the recipient's bank to hold up the transfer, resulting in further delays.

In summary, incorrect or incomplete payment details are significant contributors to delays in bank transfers. To prevent these issues, it is essential to verify all recipient information, including account numbers, names, and bank details. Additionally, understanding the potential challenges associated with international transfers, such as currency conversions and exchange rate fluctuations, can help manage expectations regarding transfer timing. By being proactive and diligent in providing accurate information, individuals and businesses can minimize the chances of delays caused by incorrect payment details.

Life in the West Bank: Safe or Not?

You may want to see also

![]()

Faster alternatives to bank transfers

Bank transfers can be time-consuming due to the various processes involved, such as compliance checks, exchange rates, cut-off times, holiday schedules, and time zones. While they are a safe and reliable method of transferring money, they may not be the fastest option available. Here are some faster alternatives to traditional bank transfers:

Wire Transfers

Wire transfers are one of the quickest ways to transfer money electronically, whether domestically or internationally. They are initiated and processed by banks, ensuring the funds are available to the recipient immediately. For domestic wire transfers, you will need the recipient's routing number, account number, name, and possibly their address. While wire transfers can be expensive, with domestic fees averaging $26, they are a good option for sending large amounts quickly.

Automated Clearing House (ACH) Transfers

ACH transfers are a widely recognised and commonly used method for domestic bank transfers. They are often considered the safest payment option as they can be reversed in certain situations, such as when a payment is sent in error. ACH transfers are usually the cheapest option, with fees generally lower than wire transfers. However, they cannot be used for international transfers, and there are daily transfer limits, such as \$1,000 per transfer for next-day ACH transfers at Bank of America.

Third-Party Apps

Third-party platforms and apps, such as PayPal, Venmo, Cash App, and Zelle, offer fast and convenient ways to transfer money. These apps can be used for non-bank money transfers, socially engaging transfers, earning referral bonuses, and quick bank-to-bank transfers. While some of these apps have limits on transfer amounts, they provide a user-friendly and efficient alternative to traditional bank transfers.

International Money Transfer Services

Services like Western Union offer extensive worldwide networks of locations for sending and receiving money. They are particularly useful for international transfers, providing a global reach that may not be available through traditional bank transfers.

Digital Wallets

Digital wallets, such as PayPal, provide a secure and fast option for transferring money without using a bank. These platforms are continuously improving their services and security measures to ensure safe and swift transactions.

Which Banks Are Still Accepting PPP Applications?

You may want to see also

Frequently asked questions

Bank transfers can only be reversed under specific circumstances. If the bank made an error, such as inputting the wrong account number or sending a duplicate transfer, the transfer can be reversed. However, if the sender provides incorrect information, the transfer cannot be reversed.

Bank transfers may be delayed for various reasons, including incorrect payment details, compliance checks, and currency exchange rates. If your transfer is time-sensitive, consider using a faster payment method or an alternative platform such as PayPal or Venmo.

There are several ways to transfer money, including bank drafts, money orders, wire transfers, and internet money transfers. Wire transfers and internet money transfers are generally the fastest methods. In the US, ACH (Automated Clearing House) transfers and wire transfers are the two main categories.