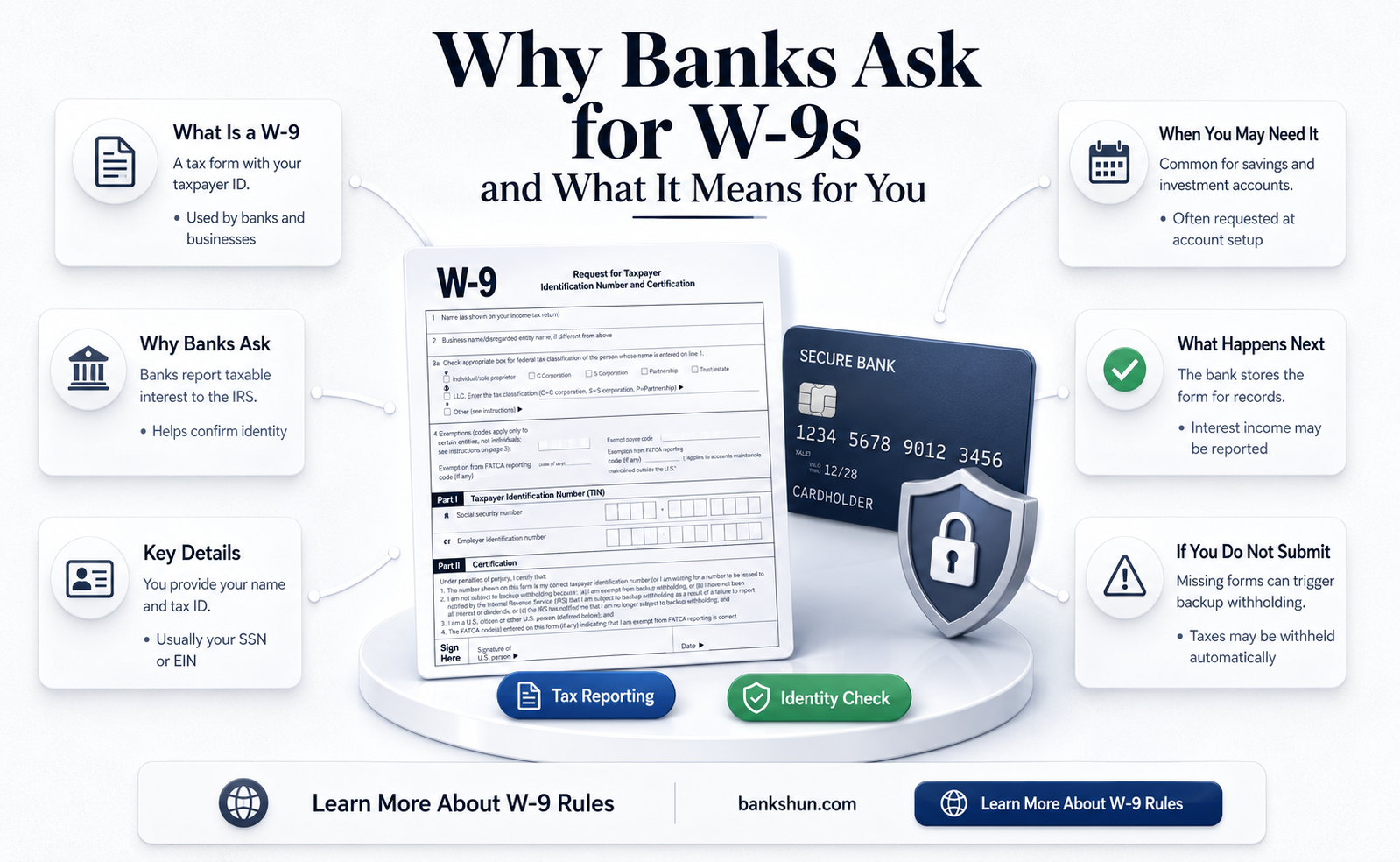

Banks may request a W-9 form from customers to comply with Internal Revenue Service (IRS) regulations. A W-9 form is used by financial institutions to collect the tax identification numbers of individuals or entities. This information is then reported to the IRS, which helps prevent tax evasion. Typically, banks request a W-9 form when they issue income, such as interest or dividends, to a customer. Foreign banks may also request a W-9 form to comply with the Foreign Account Tax Compliance Act (FATCA), which requires them to report information on accounts held by US taxpayers.

| Characteristics | Values |

|---|---|

| Why banks ask customers for W-9s | To collect the tax ID numbers of individuals or other entities |

| To comply with the Foreign Account Tax Compliance Act (FATCA) | |

| To confirm the customer's name, tax ID number, address, account number, and balance | |

| To prevent backup withholding of interest earned for non-US account holders | |

| To generate a report to send to the US government | |

| To report information to the IRS about payments made to the customer | |

| To issue a 1099 form to report income to the IRS | |

| When banks ask for W-9s | When they issue income to the customer, typically in the form of interest or dividends |

| When the customer's tax ID number does not match IRS records | |

| When the bank needs to comply with CIP verification and KYC/AML compliance rules |

Explore related products

What You'll Learn

![]()

Foreign banks and FATCA reporting

Banks and other financial institutions often request W-9 forms from their customers. These forms are used to collect the customer's tax ID number, which is then reported to the IRS. This is particularly relevant for foreign banks in relation to the Foreign Account Tax Compliance Act (FATCA).

FATCA is a US law that aims to combat tax evasion by US persons holding accounts and assets in foreign institutions. It requires these foreign financial institutions (FFIs) to report directly to the IRS information about financial accounts held by US persons. This includes not only banks but also investment entities, brokers, and certain insurance companies. FATCA requires foreign banks to notify the US government about accounts held by Americans, including pensions, stocks, partnership interests, mutual funds, foreign-issued life insurance, and foreign real estate.

To comply with FATCA, foreign banks need to collect and report specific information about their US account holders. This includes the name, tax ID number, address, account number, and account balance of all American account holders. FATCA also requires FFIs to search their customer databases for individuals suspected of being US persons and to disclose their names, addresses, transactions, and Tax Identification Numbers (TINs). Some accounts, such as retirement savings and other tax-favored products, may be excluded from reporting.

FATCA has been controversial due to its extraterritorial implications, with critics arguing that it forces foreign financial institutions to become extensions of the IRS and jeopardizes the privacy rights of non-US citizens. There have been reports of foreign banks refusing to open accounts for Americans due to the reporting requirements and penalties associated with FATCA. However, supporters of FATCA argue that it has received international support because of its effectiveness in detecting and combating tax evasion.

In addition to FATCA reporting, individuals with foreign accounts may also need to submit additional reports to the IRS, such as the Report of Foreign Bank and Financial Accounts (FBAR) or Form 8938, depending on the value of their foreign assets. US taxpayers with foreign financial assets exceeding certain thresholds (typically $50,000 for individuals living in the US and $200,000 for those living abroad) must report this information on Form 8938, which is attached to their annual income tax return.

Understanding CD in Banking: What Does It Mean?

You may want to see also

Explore related products

![]()

Backup withholding

When opening a new account, making an investment, or receiving payments reported on Form 1099, individuals or entities must provide their taxpayer identification number (TIN) to the respective institution. In turn, the institution issues a Form W-9, Request for Taxpayer Identification Number and Certification, or a similar form. The individual or entity must enter their TIN on the form.

If your Form 1099 shows an amount withheld under the backup withholding rules, report the amount as federal income tax withheld on your income tax return for the year you received the income. If you operate as a partnership or subchapter S corporation, any backup withholding can only be claimed by the partners and shareholders.

Factors that necessitate backup withholding include:

- Incorrect taxpayer identification number (TIN)/ITIN/ATIN on Form W-9

- Failure to provide the TIN in the required manner

- IRS directive to withhold for under-reported interest or dividends (after four notices over at least 120 days)

- Failure to certify exemption from backup withholding for under-reported interest and dividends

The Oldest Bank in the USA: A Historical Perspective

You may want to see also

Explore related products

![]()

Interest and dividend income

Banks and other financial institutions may request a W-9 form from customers who are earning interest or dividend income. This includes foreign banks, investment companies, brokers, and insurance companies. These institutions use the W-9 form to collect the customer's tax identification number (TIN) and report information to the Internal Revenue Service (IRS) based on the Foreign Account Tax Compliance Act (FATCA).

FATCA requires foreign financial institutions to report information on accounts held by US taxpayers or entities primarily owned by US taxpayers. This includes the name, tax ID number, address, account number, and balance of all American account holders. By requesting a W-9 form, foreign banks can obtain the necessary information to comply with FATCA requirements.

When a customer earns interest or dividend income, the bank typically issues a 1099 form (such as a 1099-INT or 1099-DIV) to report this income to the IRS. The W-9 form ensures that the bank has the customer's correct TIN to include on the 1099 form. Without the W-9 form, the bank may not be able to report the income accurately, which could lead to issues with the IRS.

It's important to note that the 60-day exemption from backup withholding does not apply to interest and dividend payments. If a customer does not provide their TIN within 60 days of receiving an "awaiting-TIN" certificate, the bank must begin backup withholding on interest and dividend payments. This means that the bank will withhold a portion of these payments and remit them to the IRS on the customer's behalf.

Were Louisville Bank's Armed Guards Effective?

You may want to see also

Explore related products

![]()

Non-compliance and red flags

Non-compliance with W-9 requests can have significant consequences for both individuals and businesses. For individuals, failure to submit a W-9 form to a foreign bank may result in the bank's inability to report your account to the IRS, as required by the Foreign Account Tax Compliance Act (FATCA). This could lead to the bank closing your account or sending a non-compliance report to the IRS, which may result in further scrutiny and potential red flags for the account holder.

Similarly, businesses that do not collect and verify W-9 forms from their vendors risk non-compliance with IRS regulations, particularly when reporting payments of $600 or more. Inaccurate or missing vendor information can lead to fines and penalties, as the IRS imposes penalties for inaccuracies in information returns. By collecting W-9 forms, businesses can cross-check vendor details, address discrepancies, and maintain accurate records, reducing the likelihood of IRS audits and potential red flags.

For U.S. persons with foreign accounts, non-compliance with W-9 requirements can trigger additional consequences. If the aggregate total of all foreign financial accounts exceeds $10,000 during the year, U.S. citizens, resident aliens, and certain entities must file a Report of Foreign Bank and Financial Accounts (FBAR) electronically. Failure to do so can result in further scrutiny and potential penalties from the IRS.

Additionally, under FATCA, foreign financial institutions (FFIs) are required to report all U.S. account holders who are specified U.S. persons. If an FFI fails to provide the required documentation or certification, a withholding agent must withhold 30% of any withholdable payment. This highlights the importance of complying with W-9 requests to avoid unnecessary withholding and potential issues with the IRS.

In summary, non-compliance with W-9 requests can lead to a range of issues, including account closures, non-compliance reports, IRS scrutiny, fines, and penalties. To avoid these red flags, individuals and businesses should prioritize providing or collecting W-9 forms, respectively, to ensure accurate and up-to-date information is reported to the IRS and other relevant authorities.

The Fate of Christopher & Banks: What Happened?

You may want to see also

Explore related products

![]()

Substitute forms

The IRS allows for the use of substitute W-9 forms, provided their content is substantially similar to the official IRS Form W-9 and meets certain certification requirements. The substitute form must contain the payee's name and TIN and be signed and dated under penalties of perjury by the payee or a person authorized to sign for them.

The certifications on the substitute form must clearly state that:

- The payee is not subject to backup withholding due to failure to report interest and dividend income

- The payee is a U.S. person

- The FATCA code (if any) indicating that the payee is exempt from FATCA reporting is correct

The substitute form may also incorporate other business forms customarily used, such as account signature cards. The signature requirements for the substitute form can be met in two ways. Firstly, by using a separate signature line just for the certifications. Secondly, by using a single signature line for all provisions, in which case the certifications must be highlighted, boxed, printed in bold, or presented in a way that makes the language stand out.

Additionally, the following statement must be presented in a manner that stands out and appears immediately above the single signature line: "The IRS does not require your consent to any provision of this document other than the certifications required to avoid backup withholding."

Did Lannisters Repay the Iron Bank?

You may want to see also

Frequently asked questions

Banks request a W-9 form when they issue income to customers, typically in the form of interest or dividends. They use the form to collect the customer's tax ID number.

If you don’t submit a W-9, the bank may not be able to make a report to the IRS. In this case, the bank may close your account or send a noncompliance report to the IRS, which could result in further issues.

No, it seems that not all banks ask customers for W-9s. This may be because they already have the customer's correct SSN/ITIN on file.

![Out of the Box with Easy Blocks( Fun with Free-Form Piecing)[OUT OF THE BOX W/EASY BLOCKS][Paperback]](https://m.media-amazon.com/images/I/512d9Mi4v1L._AC_UL320_.jpg)