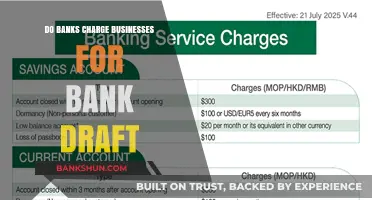

Banks charge fees for a variety of reasons, including account maintenance, overdrafts, and ATM usage. These fees can vary from monthly maintenance fees of $4 to $25 to overdraft charges of up to $35 per transaction. Additionally, using out-of-network ATMs can result in charges from both the bank and the ATM provider, typically ranging from a few dollars to $2.50 per transaction. Banks may also charge fees for international purchases and paper statements. While some banks charge a fee for card replacement, others offer this service for free. In recent years, some merchants have added a 3-4% fee to debit/credit card purchases to offset the fees charged by banks for their services. This practice is more common among small businesses and is seen as an allowable business expense. However, it is important to note that processing fees on debit card transactions are illegal in the US. Overall, understanding the various bank fees and how to avoid them can help individuals manage their finances more effectively.

| Characteristics | Values |

|---|---|

| Bank maintenance fee | Charged to keep the account safe and ready to use |

| Overdraft fee | Charged when the account holder spends more money than they have in their account |

| International transaction fee | Charged when a card is swiped outside the country |

| ATM fee | Charged when using an out-of-network ATM |

| Card replacement fee | Charged when a card is lost or stolen |

| Paper statement fee | Charged when a customer requests to receive paper statements |

| Prepaid card fee | Charged for holding or using a prepaid card, including activation, maintenance, and transaction fees |

| Processing fee | Charged by some merchants to offset the fees charged by banks for card transactions |

Explore related products

![iPhone Charger Fast Charging,[MFi Certified] 2Pack 20W Type C Fast Charger Block with 6FT USB C to Lightning Cable Compatible for iPhone 14/13/12/11 Pro Max/Xs Max/XR/X,iPad (Yellow)](https://m.media-amazon.com/images/I/61kSDFC+5gL._AC_UY218_.jpg)

What You'll Learn

![]()

Foreign transaction fees

When making purchases abroad, it is important to be aware of the potential for foreign transaction fees. These fees can add up quickly, especially for extended trips or large purchases. To avoid these fees, it is recommended to shop around for credit and debit cards that do not charge foreign transaction fees. Cards such as those issued by Capital One, Discover, Charles Schwab Checking, and Capital One 360 are known for not charging foreign transaction fees. Additionally, some card issuers may waive foreign transaction fees for certain types of transactions or if you meet certain requirements, such as having a minimum balance in your account.

It is always a good idea to carefully review the terms and conditions of your card to understand the fees associated with foreign transactions. By being aware of these fees and planning ahead, you can make informed decisions and potentially save money on your purchases while travelling or shopping online with foreign merchants.

Are Bank Transfers to Roth IRA Free of Charge?

You may want to see also

Explore related products

![[4 Pack] USB C Charger Block Fast Charging Multiport Adpater [PD 20W USB-C & QC 3.0 USB-A Port] for i Phone 17/16/15/14/13/12/11/X/8, i Pad, Galaxy, Google, Galaxy & More](https://m.media-amazon.com/images/I/51eAnSUfXSL._AC_UY218_.jpg)

![INIU USB C to USB C Cable, 240W Fast Charging [6.6ft, 2-Pack] Type C Charger Cord, Braided USBC Phone Charger Cable for iPhone 17 16 15 Pro Max Samsung S25 S24 Laptops MacBook iPad Air Switch etc.](https://m.media-amazon.com/images/I/814lZbU+YYL._AC_UY218_.jpg)

![]()

Monthly account fees

Banks may charge a monthly maintenance fee, also known as a monthly service charge, to cover their operating costs. These fees are automatically withdrawn from your account and typically range from $5 to $25 per month, although some accounts with additional features may charge higher fees. Banks often waive these fees if you maintain a certain minimum balance or meet other requirements such as linking your checking and savings accounts or setting up direct deposits.

Some banks, such as Capital One, offer checking accounts with no monthly fees. Additionally, some institutions, like Fidelity, are 0% fee institutions. It's important to carefully review the terms and conditions of your account to understand any potential monthly account fees and how to avoid them.

Overdraft fees are another common charge. These occur when you spend more money than you have in your account, and they can be costly, typically ranging from $30 to $35 per transaction. Banks may also charge for overdraft protection, which allows you to access linked accounts or lines of credit to cover overdrafts. To avoid overdraft fees, you can set up low-balance alerts, carefully monitor your account, or opt for overdraft protection if offered by your bank.

In addition to monthly maintenance and overdraft fees, banks may charge various other fees. These include wire transfer fees, foreign transaction fees, ATM fees, account inactivity fees, and fees for stop payments or replacement cards. It's important to be aware of the specific fees associated with your account to effectively manage your finances and avoid unnecessary charges.

The Owner of Fidelity Bank: A Profile

You may want to see also

Explore related products

![]()

Overdraft fees

An overdraft fee is a charge that occurs when you don't have enough money in your account to cover a transaction, but the bank pays it anyway. This is often referred to as overdraft protection. The cost of overdraft fees varies by bank, but they typically range from $35 per transaction. Some banks also charge continuous overdraft fees or daily overdraft fees.

To avoid overdraft fees, it is essential to keep careful track of your account balance. Many banks offer tools to help you monitor your balance, such as mobile apps, alerts, and virtual financial assistants. Additionally, you can opt out of overdraft protection, which means that if you use your debit card and don't have sufficient funds, the bank will not cover the purchase, and your transaction will be declined.

Some banks offer accounts with no overdraft fees, such as the Bank of America Advantage SafeBalance Banking® account. Another option is to link multiple accounts with overdraft protection, allowing you to transfer funds from a linked backup account to cover purchases and payments.

It is worth noting that banks are required by federal law to disclose any fees associated with a deposit account. Therefore, it is essential to review the account opening disclosure and fee schedule provided by the bank to understand the potential charges.

Old NZ Bank Notes: Still Legal?

You may want to see also

Explore related products

![]()

ATM fees

Banks often charge fees for ATM transactions. These fees can vary depending on the bank and the type of account you have. On average, ATM fees are $4.77 per transaction, but they can range from $4.16 in Boston to $5.33 in Atlanta. These fees are a combination of charges from the bank and the ATM owner. Out-of-network ATM transactions usually result in two fees: a surcharge from your bank for using a non-network machine and a small fee from the ATM operator.

There are several ways to avoid paying ATM fees. One way is to use ATMs within your bank's network, which are usually free to use. Many banks offer ATM locators on their websites or mobile apps to help you find nearby fee-free ATMs. Some banks partner with networks like MoneyPass, Allpoint, or the Global ATM Alliance, providing access to thousands of fee-free ATMs. Getting cash back at checkout when using a debit card at a store is another way to avoid ATM fees.

If you are travelling outside of the US, you may incur additional ATM fees. Foreign transaction fees can be charged by your bank for using international ATMs, and these can add up quickly. Some banks charge lower international transaction fees, so it is worth shopping around for different options before travelling internationally.

Umbrellas at TIAA Bank Stadium: What's the Deal?

You may want to see also

Explore related products

![]()

Card replacement fees

It is important to note that card replacement fees may differ depending on the type of card and the reason for replacement. For example, some banks may charge a higher fee for expedited or rush replacement services, while others may offer free replacement for lost or stolen cards. Additionally, certain premium cards with significant annual fees, such as metal cards, may also have higher replacement fees associated with them.

To avoid unnecessary costs, it is recommended to review the policies of your bank or credit card company regarding card replacement fees. In some cases, they may waive the fee or offer alternatives, such as digital card information for online purchases, while a new physical card is being processed and shipped. Being proactive and inquiring about card replacement policies can help individuals make informed decisions and potentially save money in the event of card loss, theft, or damage.

While card replacement fees are an additional cost to consider, it is worth noting that card replacement is a necessary service provided by financial institutions to ensure the security and functionality of their customers' accounts. By offering replacement cards, banks and credit card companies help individuals maintain access to their funds and continue making purchases securely.

To summarise, card replacement fees vary across different financial institutions, with some charging as little as \$5 and others up to \$25. However, there are also institutions that waive these fees entirely, emphasising the importance of understanding the specific policies of your bank or credit card company. By staying informed and proactive, individuals can effectively manage their finances and minimise unnecessary expenses associated with card replacement.

Banks: Back in Business or Still Recovering?

You may want to see also

Frequently asked questions

Banks do not typically charge fees for store purchases. However, some banks may charge a fee for international purchases or transactions made outside of the U.S. Additionally, certain banks may charge monthly fees for maintaining a checking or savings account.

Some merchants, particularly small businesses, add fees to debit/credit card purchases to offset the processing fees charged by the credit card companies or banks. These fees are usually between 3-4% of the purchase amount.

To avoid bank fees, consider the following:

- Maintain a minimum balance in your account.

- Set up a monthly direct deposit.

- Choose a bank with no monthly fees.

- Use in-network ATMs to avoid withdrawal charges.

- Opt-out of overdraft protection to prevent overdraft fees.

Common bank fees include monthly maintenance fees, overdraft fees, ATM fees, and international transaction fees. Some banks may also charge for paper statements or replacement cards.