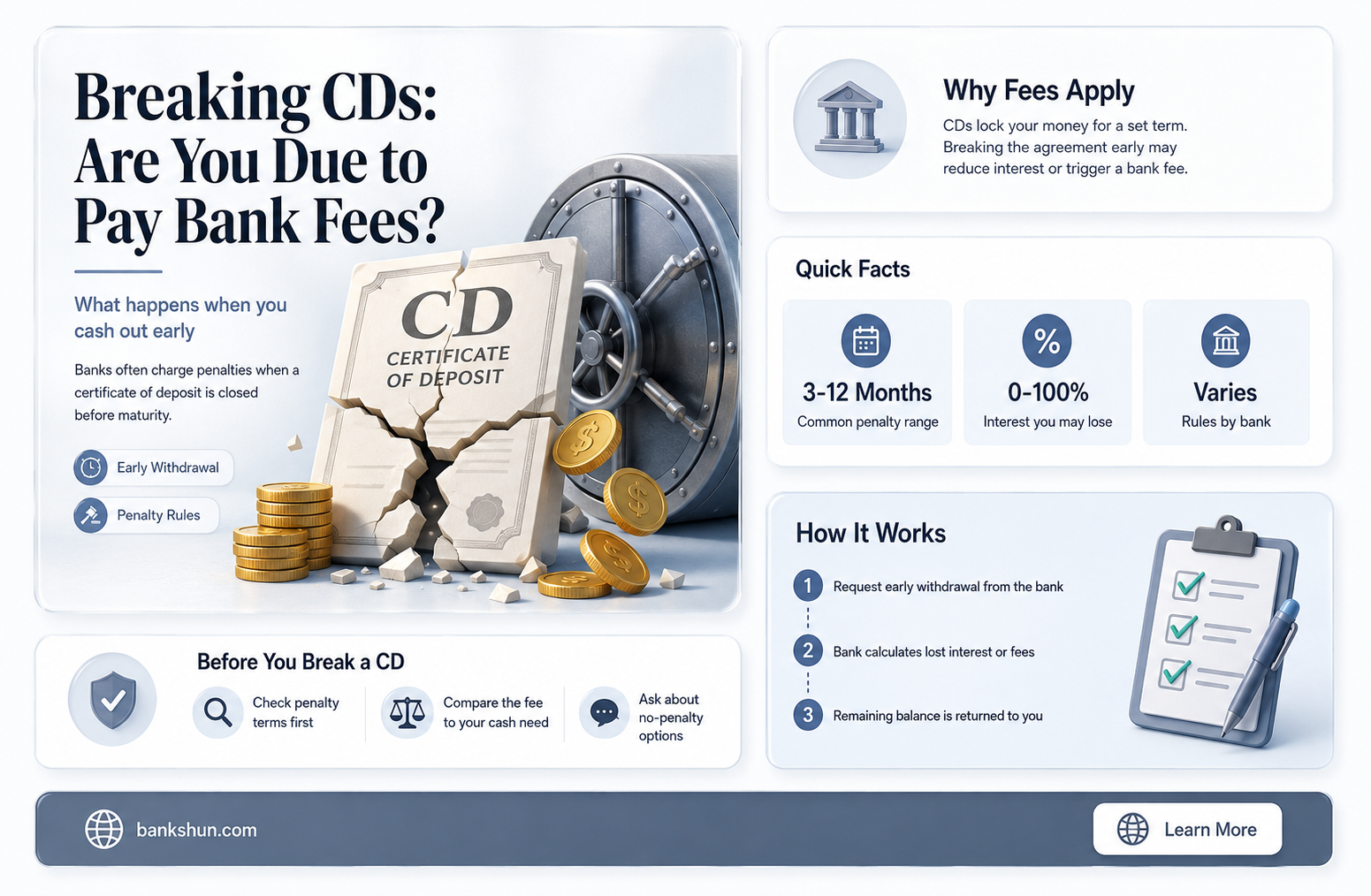

Certificates of deposit (CDs) are a popular investment product for savers looking for a guaranteed return on their money. They are safe, low-risk accounts offering competitive interest rates that remain fixed for the CD's term. While CDs are a great way to save money, there are some fees associated with them that can cut into your earnings. One of the most common CD fees is the early withdrawal penalty. When you take funds out of your CD account before the maturity date, many CDs charge a fee equal to several months' interest. This is because CDs, unlike other bank accounts, require you to lock up a fixed sum of money for a set period of months or years. So, breaking the seal is what can cost you.

| Characteristics | Values |

|---|---|

| Type of fee | Early withdrawal penalty |

| Fee amount | Varies by bank; typically several months' interest |

| Fee calculation | Not typically written as a fixed dollar amount or percentage of a transaction; calculated based on the CD term and the number of days or months of interest |

| Fee avoidance | Choose a no-penalty CD, shorter-term CDs, or employ strategies such as CD laddering |

| Other fees | Monthly maintenance fees, broker fees, monthly service fees |

Explore related products

What You'll Learn

![]()

Early withdrawal fees

The exact fee charged will depend on the specific terms of your CD and the bank you are using. Some banks may also allow partial withdrawals, in which case you will only pay a fee on the portion of money and interest you withdraw early. It is important to carefully read the terms and conditions of your CD account to understand the early withdrawal fees that may apply.

There are strategies you can use to avoid paying early withdrawal fees. One option is to choose a shorter-term CD, as these typically have lower penalties than longer-term CDs. You can also consider a no-penalty CD, which does not charge a fee for withdrawing before maturity, although these are less common than regular CDs. Another strategy is to use a CD ladder, where you open multiple CDs with staggered term lengths. This provides you with access to some savings in case of emergencies while still earning the high returns of long-term CDs.

It is worth noting that breaking a CD early may be worth it in certain situations, such as when you need funds right away to cover a large, unexpected expense. In such cases, you can consider liquidating your CD early, but be prepared to pay the associated early withdrawal penalty.

Understanding Rule 144: Are Bank-Issued Securities Exempt?

You may want to see also

Explore related products

![]()

Monthly maintenance fees

When it comes to breaking CDs, monthly maintenance fees can be a concern. These fees are typically charged by banks and credit unions for maintaining CD accounts, and they can eat into your earnings over time. However, it's important to note that not all banks charge monthly maintenance fees for CDs. In fact, some institutions, like BECU, explicitly advertise the absence of monthly maintenance fees for their CDs, allowing customers to retain more of their money.

The presence or absence of monthly maintenance fees can vary depending on the specific bank and the type of CD being offered. For example, brokered CDs purchased from different issuing banks may have different fee structures compared to traditional bank CDs. It's always a good idea to carefully review the terms and conditions of a CD account before opening one, as different banks have different policies regarding fees, and some charges can be quite significant. Understanding the details can help you make an informed decision and avoid unexpected costs.

While monthly maintenance fees are not typically the most common type of CD fee, early withdrawal penalties are often a more significant concern for CD holders. These penalties occur when you withdraw funds from your CD account before the maturity date, and they can result in a fee equivalent to several months' worth of interest. Federal law sets a minimum penalty for early withdrawals, but there is no maximum penalty, so these fees can add up quickly. Reviewing the specific terms of your account agreement is crucial to understanding the potential fees associated with early withdrawals.

To avoid monthly maintenance fees and other CD-related charges, it's essential to conduct thorough research and planning. Understanding the various fees associated with different CD options can help you make an informed decision when choosing a CD account. Additionally, selecting a CD term that aligns with your savings goals and timeline can help you avoid early withdrawal penalties. By staying informed and proactive, you can maximize your earnings and make the most of your CD investments while minimizing unnecessary expenses.

In summary, while monthly maintenance fees may not be a universal feature of CD accounts, they are certainly something to be aware of when considering breaking CDs. By understanding the fee structure and carefully reviewing the terms and conditions of different CD offerings, you can make informed choices that minimize fees and maximize the benefits of your investments. Remember that different banks have different policies, so it's always worth asking a bank representative for clarification if you're unsure about any potential charges.

Are Bank Transfers to Roth IRA Free of Charge?

You may want to see also

Explore related products

![P1HARMONY DISHARMONY:BREAK OUT 2nd Mini Album [ BREAK OUT / FREAK OUT ] RANDOM ver. CD+88p Photo Book+Folding Poster(On pack)+Standing Photo Card+etc K-POP SEALED+TRACKING CODE](https://m.media-amazon.com/images/I/415YNzLnOQS._AC_UY218_.jpg)

![The Penalty [Blu-ray]](https://m.media-amazon.com/images/I/91fZ8MEHZ4L._AC_UY218_.jpg)

![]()

Broker fees

Brokered CDs are certificates of deposit provided through brokerages and issued by banks. Brokered CDs can be sold on the secondary market before maturity, but this often incurs a transaction fee. Broker-assisted trades placed over the phone or online often come with an additional fee.

For example, Vanguard Brokerage charges a $25 broker-assisted fee for secondary trades placed over the phone. Fidelity charges a $1 per CD trading fee for CDs with a $1,000 par value. Charles Schwab charges $1 per $1,000 in CD value for secondary market transactions, with a $10 minimum and $250 maximum.

Brokered CDs may cost more to obtain than bank CDs due to transaction costs. Some brokerages may charge fees for asset management, financial planning, and other services. Brokered CDs can be purchased commission-free, but sales on the secondary market typically require a transaction fee.

It is important to carefully review the terms and conditions of brokered CDs to understand the associated fees and costs. Different brokerages have different policies and fee structures, so it is essential to compare options before choosing a broker.

Banking Apps on Public Wi-Fi: Safe or Not?

You may want to see also

Explore related products

![]()

No-penalty CDs

Several banks offer no-penalty CDs with varying terms and conditions. For example, Marcus by Goldman Sachs provides three no-penalty CD terms: seven, 11, and 13 months. Withdrawals are permitted seven days after funding the account, and there are no hidden fees or minimum balance requirements to earn the stated Annual Percentage Yield (APY). Similarly, Ally offers an 11-month no-penalty CD with no minimum opening deposit, and you can withdraw your balance and interest after the first six days of funding.

Colorado Federal Savings Bank also provides an 11-month no-penalty CD, but it requires a $5,000 minimum deposit. Penalty-free withdrawals are allowed after seven days. CIT Bank, a subsidiary of First Citizens Bank, offers an 11-month no-penalty CD and eight terms of regular CDs. Bank of America, one of the largest banks in the US, has a flexible 12-month no-penalty CD with a competitive rate. This CD allows you to withdraw interest and your entire balance before maturity without penalty after the first seven days.

NTB Banks: A National Presence?

You may want to see also

Explore related products

![]()

Partial withdrawals

Certificates of deposit (CDs) are fixed-income investments that generally pay a set rate of interest over a fixed time period. While CDs offer a safe and low-risk avenue for investments with competitive interest rates, there are associated fees that one must be aware of. Many banks and credit unions charge fees for opening and maintaining CD accounts, which can eat into your earnings. These include early withdrawal fees, monthly maintenance fees, and broker fees.

The penalty for early withdrawals can be steep, sometimes costing between 90 and 365 days' interest. Generally, the longer the term of the CD, the higher the penalty for early withdrawal. This means that if you withdraw funds early, you may lose most or even all of your earnings. To avoid this penalty, it is advisable to choose a term that aligns with your savings goals and timeline. CDs typically have terms ranging from a few months to several years, so you can select one that suits your needs.

There are strategies to access cash early without incurring penalties, such as CD laddering or choosing a no-penalty CD. CD laddering involves spreading your funds across multiple CDs with different maturity dates. This allows you to access funds as each CD matures, rather than feeling pressured to withdraw from a single long-term CD and pay a hefty penalty. No-penalty CDs offer the benefits of traditional CDs, including locked-in interest rates, but without the early withdrawal penalty. However, it's important to remember that no-penalty CDs often earn lower interest rates than traditional CDs.

In summary, while partial withdrawals are not explicitly addressed, early withdrawal fees are a significant consideration when investing in CDs. These fees can vary depending on the terms of your account and the timing of your withdrawal. To avoid penalties, it is recommended to choose an appropriate term and consider strategies like CD laddering or no-penalty CDs.

Wells Fargo ATM Access for Advisors

You may want to see also

Frequently asked questions

Yes, most banks charge an early withdrawal fee for cashing out a certificate of deposit (CD) before the maturity date. This fee is usually based on the annual percentage yield (APY) the CD pays and can be equal to several months' interest.

A CD or certificate of deposit is a type of deposit account that's payable at the end of a specified amount of time, known as the term. CDs generally pay a fixed rate of interest and can offer a higher interest rate than other types of deposit accounts.

The early withdrawal penalty for CDs varies by bank and can depend on the CD term. Longer CD terms, such as four and five years, typically have higher penalties than shorter terms. For example, Wells Fargo charges a penalty of one month's interest for terms less than 90 days and 12 months' interest for terms over 24 months.

You can avoid paying early withdrawal fees on CDs by choosing a term that fits your savings goal and timeline. CDs with shorter terms provide earlier access to funds. No-penalty CDs also allow you to withdraw funds before maturity without incurring a penalty, but they are less common than regular CDs.

Yes, many banks and credit unions charge fees for opening and maintaining CD accounts, including monthly maintenance fees and broker fees. However, these fees can be avoided by researching the terms and conditions of different banks before opening a CD account.