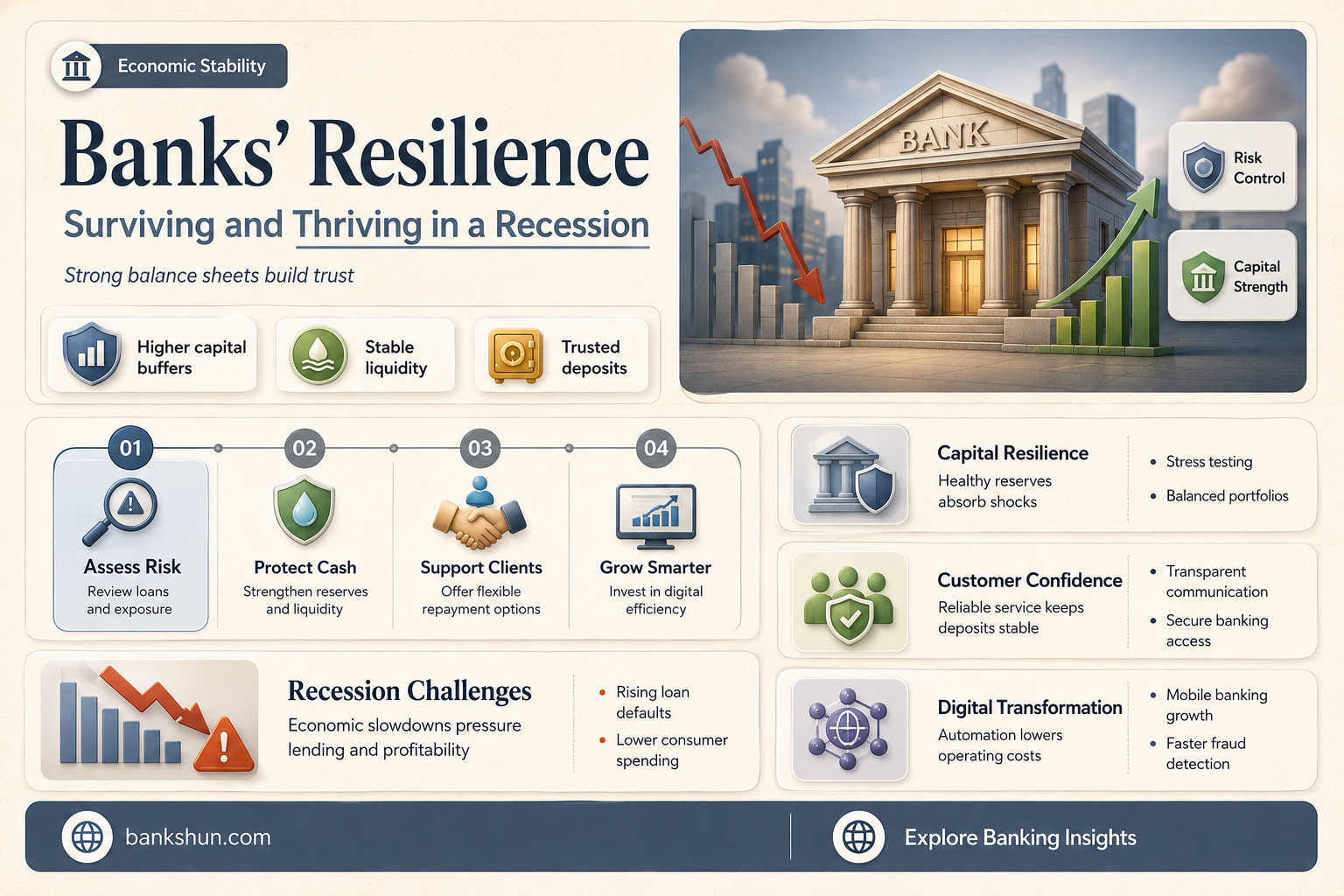

Banks are susceptible to economic downturns, and bank stocks may face challenges during recessions due to increased loan defaults and reduced consumer spending. However, some banks may be better positioned to weather recessions, such as large, well-capitalized banks with diversified revenue streams. While bank stocks can be vulnerable during economic downturns, they can also provide opportunities for investors who carefully assess the financial health and revenue diversification of specific banks. Additionally, certain sectors, like consumer banking, have been known to be resilient during recessions. Furthermore, policies like FDIC insurance protect consumers' deposits, ensuring that their money remains secure even if a bank fails during a recession.

Explore related products

What You'll Learn

![]()

Banks' profitability during a recession

Bank stocks have historically been sensitive to economic downturns, as recessions can create significant challenges for financial institutions. During recessions, consumers and businesses may struggle to meet their loan obligations, leading to higher rates of loan defaults, which directly impact banks' profitability. Additionally, banks tend to experience reduced consumer spending and lower interest rates during recessions, further affecting their profitability.

However, it is important to note that not all banks are equally affected by recessions. Large, well-capitalized banks with diversified revenue streams, such as those offering investment and wealth management services, may be better positioned to weather economic downturns compared to smaller banks that rely heavily on traditional lending. These larger banks have stronger capital reserves, making them more resilient in challenging economic conditions.

The impact of recessions on bank profitability can also depend on the severity of the economic downturn. During mild recessions or inflationary environments, banks can benefit from higher interest rates and increased lending margins. However, during deep recessions, the pro-cyclicality of bank profit increases, leading to more significant decreases in profitability. Each percentage contraction of real GDP during severe recessions results in a quarter of a percentage point decrease in the return on total bank assets.

While bank stocks may face challenges during recessions, some investors still view them as attractive investments during these periods. US banks, in particular, have demonstrated resilience, continuing to operate at strong levels of profitability even during challenging times. Additionally, community bank stocks have the potential for significant upside during and after a recession, making them an appealing investment opportunity for some.

In summary, while banks may experience reduced profitability during recessions due to loan defaults and decreased consumer spending, the impact varies across different types of banks and the severity of the economic downturn. Large, diversified banks tend to be better positioned, and investors can find opportunities in specific bank stocks, especially in the US market.

Tyra Banks' Dancing in Coyote Ugly: Did It Happen?

You may want to see also

Explore related products

![]()

Impact on bank employees

A recession can have a significant impact on bank employees, and the effects can vary depending on the specific bank, department, and role. During an economic downturn, banks often experience reduced revenue due to lower interest rates, decreased consumer spending, and increased loan defaults. This can lead to cost-cutting measures, including layoffs and hiring freezes. While some banks may be better positioned to weather the recession than others, the impact on employees can still be substantial.

In terms of specific departments and roles, investment banking and wealth management tend to be heavily affected by recessions. There may be layoffs in these areas as deal flow dries up and revenue declines. However, certain roles within banks, such as credit analysts and other support functions, may be retained even during a recession as they are crucial to the bank's operations.

The impact of a recession on bank employees can also vary depending on their seniority and indispensability within the organization. High-level positions, such as VPs and directors, are often retained as they are key to generating revenue. On the other hand, junior and more disposable employees may be at a higher risk of losing their jobs or experiencing reduced hiring opportunities.

Additionally, a recession can affect the job search and career advancement prospects for bank employees. Large banks may significantly slow down their hiring processes or implement hiring freezes. This can make it challenging for job seekers to find opportunities within these organizations. However, it is important to note that some industries and companies may thrive during a recession, creating alternative career paths for those affected by the downturn in banking.

Overall, a recession can have far-reaching consequences for bank employees, including layoffs, reduced hiring, and limited career mobility. The impact can vary depending on the specific circumstances of the bank, the employee's role and seniority, and the overall health of the economy. While challenging, a recession may also present opportunities for those who can adapt their skill sets and position themselves in industries that are more resilient to economic downturns.

Varo Bank: Real or Prepaid?

You may want to see also

Explore related products

![]()

Safety of money in bank accounts

Banks are generally considered a safe place to keep your money during a recession. While bank stocks may face challenges during recessions due to increased loan defaults and lower interest income, your money is likely to be safe in a bank account. This is because governments implement policies to protect people's money. For example, in the US, the Federal Deposit Insurance Corporation (FDIC) was created by Congress to protect bank depositors and boost public confidence in the country's financial system. The FDIC insures deposits up to $250,000 per depositor, per account ownership category, at a federally insured financial institution. This limit is also applicable to joint accounts, where up to $500,000 is protected.

It is important to note that the FDIC only covers certain types of accounts, including checking and savings accounts, certificates of deposit (CDs), cashier's checks, money orders, and money market deposit accounts (MMDA). Accounts that are not covered by the FDIC include stocks, bonds, money market funds, US Treasury securities (T-bills), annuities, life insurance policies, and the contents of safe deposit boxes.

To ensure the safety of your money during a recession, you can consider diversifying your accounts by spreading your funds across several banks or using different types of accounts, such as high-yield savings accounts, money market accounts, or CDs. These accounts offer low-risk options while still allowing you to earn interest. Additionally, you can look for banks that are part of an enhanced FDIC insurance program, like IntraFi Network Deposits, to further protect your deposits.

While your money is generally safe in a bank during a recession, it is always a good idea to stay informed and take proactive steps to protect your finances if you are concerned about an economic downturn.

Sewer Services: Red Bank, NJ's Top Choice

You may want to see also

Explore related products

![]()

Bank stocks as a smart investment during a recession

Bank stocks have historically been sensitive to economic downturns. During recessions, consumers and businesses may struggle to meet their loan obligations, leading to higher rates of loan defaults, which directly impact banks' profitability. Recessions can also cause reduced consumer spending and lower interest rates, further affecting banks' bottom lines.

However, not all banks are equally vulnerable to economic downturns. Large, well-capitalized banks with diversified revenue streams, such as those that offer investment and wealth management services, may be better positioned to weather recessions compared to smaller banks that rely heavily on traditional lending. Additionally, investment banking tends to hold up better during recessions than commercial banking. Banks with a strong history of managing risks and generating profits can be excellent long-term investments.

The performance of bank stocks during a recession can also depend on the broader economic context. For example, Canadian bank stocks have historically outperformed the broader S&P/TSX Composite during recessions. The best time to invest in Canadian banks is often in the midst of a recession, as they tend to demonstrate medium- to long-term strength.

Furthermore, banks typically outperform during a recession after underperforming in the lead-up to it. This is because banks tend to build up reserves during a downturn, and once the recession is over, they release these reserves back into earnings, driving strong stock performance. Therefore, buying bank stocks during a recession can be a smart investment strategy, provided that one carefully assesses each bank's financial health and revenue diversification.

While investing in bank stocks during a recession can offer opportunities, it is important to remember that no stock is entirely recession-proof, and the performance of bank stocks can vary depending on numerous factors. A financial advisor can help analyze and manage recession-resistant investments for your portfolio.

POD in Banking: What Does It Mean?

You may want to see also

Explore related products

![]()

Banks' resilience during economic downturns

Banks are susceptible to economic downturns, with bank stocks facing challenges during recessions. Recessions can create significant challenges for financial institutions, with consumers and businesses struggling to meet their loan obligations, leading to higher rates of loan defaults. This directly impacts banks' profitability, as does lower interest income. However, large, well-capitalized banks with diversified revenue streams may be better positioned to weather recessions compared to smaller banks that rely heavily on traditional lending. These larger banks may offer investment and wealth management services, providing a buffer during tough economic times.

During the 2008 financial crisis, banks suffered considerable losses due to high levels of mortgage defaults, and many layoffs occurred. However, some banks with strong capital cushions made it through the pandemic relatively unscathed. While bank stocks may face difficulties during economic downturns, some sectors are considered more recession-resistant, including consumer staples, utilities, and healthcare. These sectors provide essential goods and services that remain in demand regardless of economic conditions.

Consumer banking is generally more resilient than investment banking during recessions. This is because consumers tend to prioritize bank deposits during economic downturns, and higher yields benefit consumer banks. In contrast, investment banking depends on deal flow, which can dry up during a recession.

From an investment perspective, bank stocks are sometimes considered recession-proof, and investors often seek these out to protect their portfolios. While no stock is entirely recession-proof, investing in banks with a strong history of managing risks and generating profits can be a wise long-term strategy. The best time to invest in banks is often during a recession when valuations are depressed. Once the recession ends, banks release reserves back into earnings, driving strong stock performance.

To protect their finances during a recession, individuals can consider using two different banks or choosing a bank with enhanced FDIC insurance, which protects deposits of up to $250,000 per depositor.

Santander and Fifth Third Bank: Any Relation?

You may want to see also

Frequently asked questions

Your money will likely be secure in a bank account during a recession. Policies like FDIC insurance in the US keep up to $250,000 safe in individual bank accounts, even if the bank goes under.

Bank stocks typically underperform heading into a recession. However, once a recession hits, banks tend to outperform. It is recommended to assess each bank's financial health and revenue diversification before investing.

While banks may suffer losses and layoffs during a recession, some roles are indispensable, such as analysts who review loans and annual reviews.