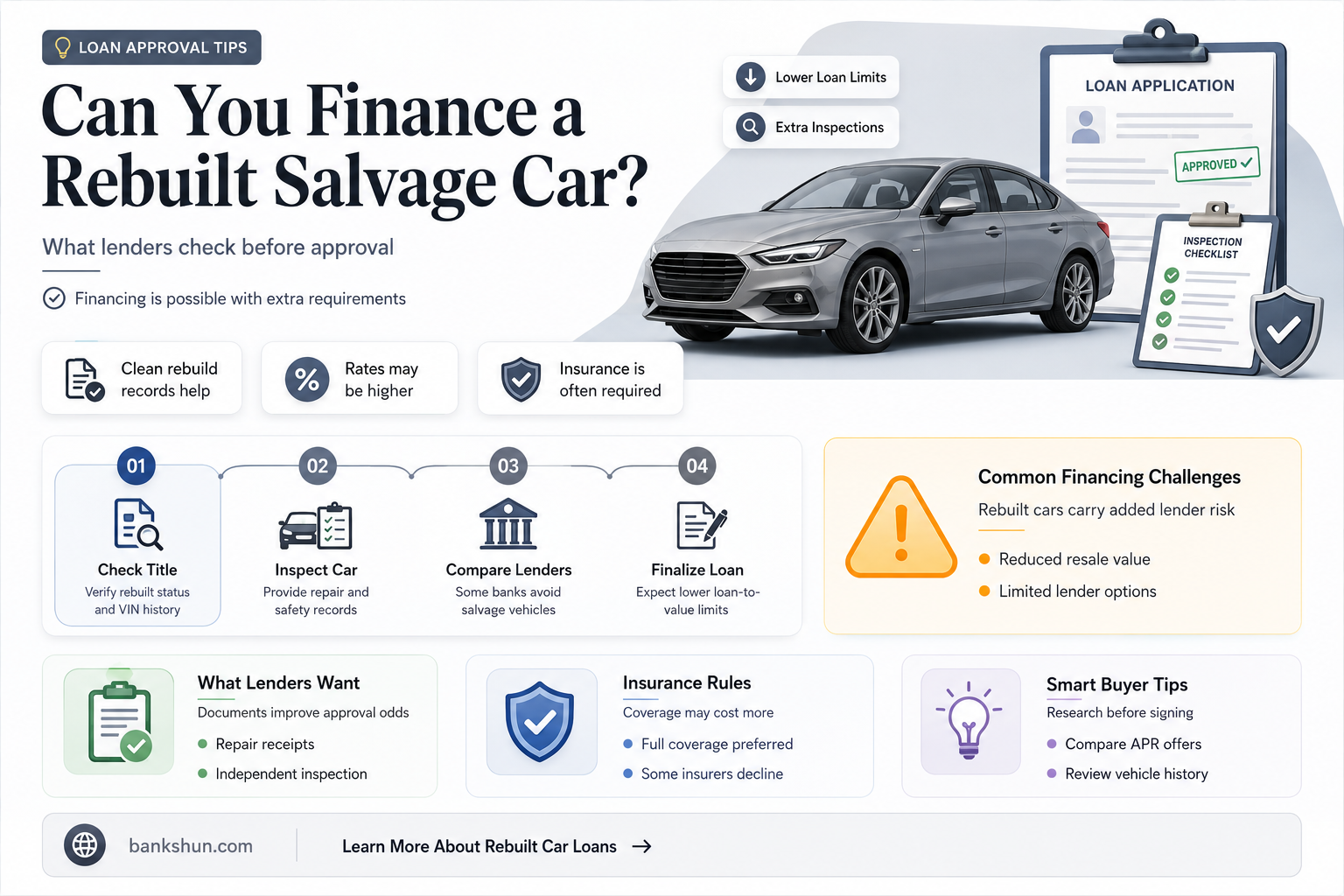

It is challenging to find lenders to finance rebuilt salvage-titled vehicles. Major banks like Wells Fargo, Chase, Capital One, and Bank of America generally do not finance rebuilt salvage-titled vehicles. Smaller banks, credit unions, and online lenders are more likely to finance these vehicles, but it may require good credit and thorough due diligence. Borrowers with good to great credit can obtain personal loans, which do not put a lien on the vehicle. LightStream, USAA, and America First Credit Union are examples of lenders that finance salvage-titled vehicles.

| Characteristics | Values |

|---|---|

| Difficulty in financing | Banks generally don't finance rebuilt salvage-titled vehicles due to the risks involved. |

| Large banks | Major banks like Wells Fargo, Chase, Capital One, and Bank of America do not finance rebuilt salvage titles. |

| Smaller banks | Smaller banks are more likely to finance rebuilt salvage titles, but it depends on the customer's credit score and history. |

| Credit unions | Some credit unions finance rebuilt salvage titles, but it depends on their policies and the state/community. |

| Online lenders | Online lenders are an option for financing rebuilt salvage titles. |

| Interest rates | Interest rates for financing rebuilt salvage titles tend to be higher due to the risks involved. |

| Insurance | Many insurance companies are hesitant to provide full coverage for rebuilt salvage titles due to potential hidden damage or improper repairs. |

| Inspection and repairs | A rebuilt salvage title vehicle must be inspected, repaired, and deemed safe to drive by an independent mechanic before financing. |

Explore related products

What You'll Learn

- Smaller banks, credit unions, and online lenders are more likely to finance rebuilt title vehicles

- Large banks like Wells Fargo, Chase, Capital One, and Bank of America generally do not finance rebuilt salvage-titled vehicles

- Borrowers with good to great credit can get personal loans for rebuilt salvage-titled vehicles

- Financing a rebuilt salvage-titled vehicle can be difficult due to the potential for hidden damage or improper repairs

- Undamaged salvage title theft recoveries can be a great buy, and financing can be a good idea

![]()

Smaller banks, credit unions, and online lenders are more likely to finance rebuilt title vehicles

It can be difficult to find a lender who will finance a vehicle with a salvage title. Large banks, in general, are reluctant to finance or refinance a rebuilt salvage title vehicle. However, smaller banks, credit unions, and online lenders are more likely to finance such vehicles.

AutoSavvy, for example, helps customers finance rebuilt title vehicles. They offer financing for branded title vehicles, which are vehicles that have been salvaged and restored to excellent condition, passing DMV inspections.

Credit unions may also be an option for financing rebuilt salvage title vehicles. While some credit unions may not offer refinancing, others may be willing to finance these vehicles, especially if they are in good condition.

Online lenders are another option for financing rebuilt salvage title vehicles. These lenders can provide financing for vehicles that have been repaired, inspected, and given a rebuilt title.

To improve the chances of securing financing, it is recommended to have good credit and obtain statements from mechanics and insurance carriers attesting to the vehicle's safety and good working condition.

The Wachovia-Wells Fargo Merger: A Retrospective Review

You may want to see also

Explore related products

![]()

Large banks like Wells Fargo, Chase, Capital One, and Bank of America generally do not finance rebuilt salvage-titled vehicles

Smaller banks, credit unions, and online lenders are more likely to finance rebuilt salvage title vehicles. Some credit unions that have been known to finance rebuilt salvage title vehicles include America First Credit Union, Navy Federal Credit Union, and State Farm. LightStream is also a popular option for those seeking to finance a rebuilt salvage-titled vehicle.

To improve the odds of getting approved for a loan on a rebuilt salvage-titled vehicle, it is a good idea to obtain a mechanic's statement that the car has been thoroughly rehabilitated and is in excellent and safe running condition. A statement from an insurance carrier indicating that they are willing to insure the vehicle can also help. Good credit can also increase the likelihood of getting approved for a loan on a rebuilt salvage-titled vehicle.

Even with these steps, financing a rebuilt salvage-titled vehicle can be difficult. Many insurance companies are hesitant to provide full coverage for these vehicles due to the potential for hidden damage or improper repairs. Additionally, interest rates for financing a rebuilt salvage-titled vehicle may be high.

Cheque Expiry: Do Bank Cheques Have a Shelf Life?

You may want to see also

Explore related products

![]()

Borrowers with good to great credit can get personal loans for rebuilt salvage-titled vehicles

It is challenging to obtain financing for a rebuilt salvage-titled vehicle, and major banks like Wells Fargo, Chase, Capital One, and Bank of America generally do not offer such loans. This is because rebuilt salvage-titled vehicles are perceived as riskier investments due to their history of being written off as a total loss, accident damage, or other issues like floods or fires. As a result, they are considered more likely to break down, lose value, or experience mechanical issues in the future.

However, borrowers with good to great credit do have some options for obtaining personal loans for rebuilt salvage-titled vehicles. LightStream, for example, is recommended by some sources as a competitive option for such loans. USAA also lends for salvage-titled vehicles but requires military affiliation. Many credit unions also offer these loans, such as America First Credit Union in the western US. Dealerships often work with third-party indirect lenders like Westlake Financial and Western Lending, and some dealers can facilitate loans with lenders like Navy Federal Credit Union or Capital One, although their policies may vary.

To increase the chances of approval for a rebuilt title car loan, it is advisable to obtain and present a mechanic's statement certifying that the car is in excellent and safe running condition, along with a statement from an auto insurance carrier indicating their willingness to insure the vehicle. While financing options for these vehicles may be limited, they can be a good deal for buyers willing to take on the risk, as they are considerably cheaper than cars with clean titles.

US Bank Fund Holds: How Long Do They Last?

You may want to see also

Explore related products

![]()

Financing a rebuilt salvage-titled vehicle can be difficult due to the potential for hidden damage or improper repairs

Smaller banks, credit unions, and online lenders are typically more willing to finance rebuilt salvage-titled vehicles. Borrowers with good to great credit can obtain personal loans, which are guaranteed by their signature and do not put a lien on the vehicle. LightStream, for example, has been praised for its straightforward loan process for salvage-titled vehicles. USAA also lends for salvage-titled vehicles but requires military affiliation. Dealerships often work with third-party lenders such as Westlake Financial and Western Lending, which may be more open to financing salvage-titled vehicles.

It is important to note that even if financing is obtained for a rebuilt salvage-titled vehicle, interest rates may be higher than for a car with a clean title due to the inherent risks involved. Additionally, insurance for such vehicles can be challenging to obtain, as many insurance companies are hesitant to provide full coverage due to the potential for hidden damage or improper repairs.

To improve the odds of securing financing for a rebuilt salvage-titled vehicle, it is recommended to obtain a mechanic's statement certifying that the car has been thoroughly rehabilitated and is in excellent and safe working condition. A statement from an insurance carrier indicating their willingness to insure the vehicle can also help. Furthermore, having a strong relationship with a bank branch manager can increase the chances of obtaining financing from a major bank.

While financing a rebuilt salvage-titled vehicle comes with challenges, it can be a great option for budget-conscious buyers, as these vehicles typically sell for 20-40% less than their counterparts with clean titles. However, buyers should carefully consider the potential risks and ensure they are comfortable with the possibility of hidden damage or repair issues.

Weekend Bank Transfers: What You Need to Know

You may want to see also

Explore related products

![]()

Undamaged salvage title theft recoveries can be a great buy, and financing can be a good idea

Credit unions, such as America First Credit Union in the western US, are another option for financing salvage titles. Dealerships often work with third-party lenders like Westlake Financial and Western Lending, and some dealers can connect with other lenders that may not directly loan on a salvage title, such as Navy Federal Credit Union or Capital One.

When considering an undamaged salvage title theft recovery, it's important to be cautious and conduct a thorough inspection. While these vehicles can be great deals, selling them clean may not be worth the potential headaches for insurance companies, and they may salvage perfect theft recoveries for liability reasons. Additionally, insurance can be more challenging to obtain for these vehicles, and full coverage may not be an option.

Before purchasing an undamaged salvage title theft recovery, ensure that you can obtain insurance for the vehicle. Be prepared for potential issues with hidden damage or improper repairs, as insurance companies are hesitant to provide full coverage due to these risks. It is also recommended to have a good relationship with your bank and strong credit to increase your chances of obtaining financing for this type of vehicle. Overall, undamaged salvage title theft recoveries can be a great buy if you are willing to navigate the financing and insurance challenges.

Crafting a Compelling Resume: Adding a Minor for Banking Roles

You may want to see also

Frequently asked questions

Yes, it is possible to finance a rebuilt salvage-titled vehicle, but it can be challenging. Smaller banks, credit unions, and online lenders are more likely to provide financing for these vehicles.

Some options for financing a rebuilt salvage-titled vehicle include LightStream, America First Credit Union, Westlake Financial, and Western Lending. Navy Federal Credit Union previously financed these vehicles but stopped in 2022.

Lenders typically consider factors such as credit score, credit history, and loan-to-value ratio when deciding whether to finance a rebuilt salvage-titled vehicle. A strong relationship with the bank and approval from multiple managers may also be required.

Yes, financing a rebuilt salvage-titled vehicle may come with higher interest rates due to the perceived risk. Obtaining insurance for these vehicles can also be difficult as many insurance companies are hesitant to provide full coverage due to the potential for hidden damage or improper repairs.

![[2-Pack] Mini Portable Charger 5000mAh Power Bank,3A PD USB C Cell Phone Portable Power, LCD Display Battery Pack Compatible with iPhone 16/15/15 plus/15 pro/15 pro Max/Android/Samsung/Moto/LG etc](https://m.media-amazon.com/images/I/61JTODtGlRL._AC_UL320_.jpg)