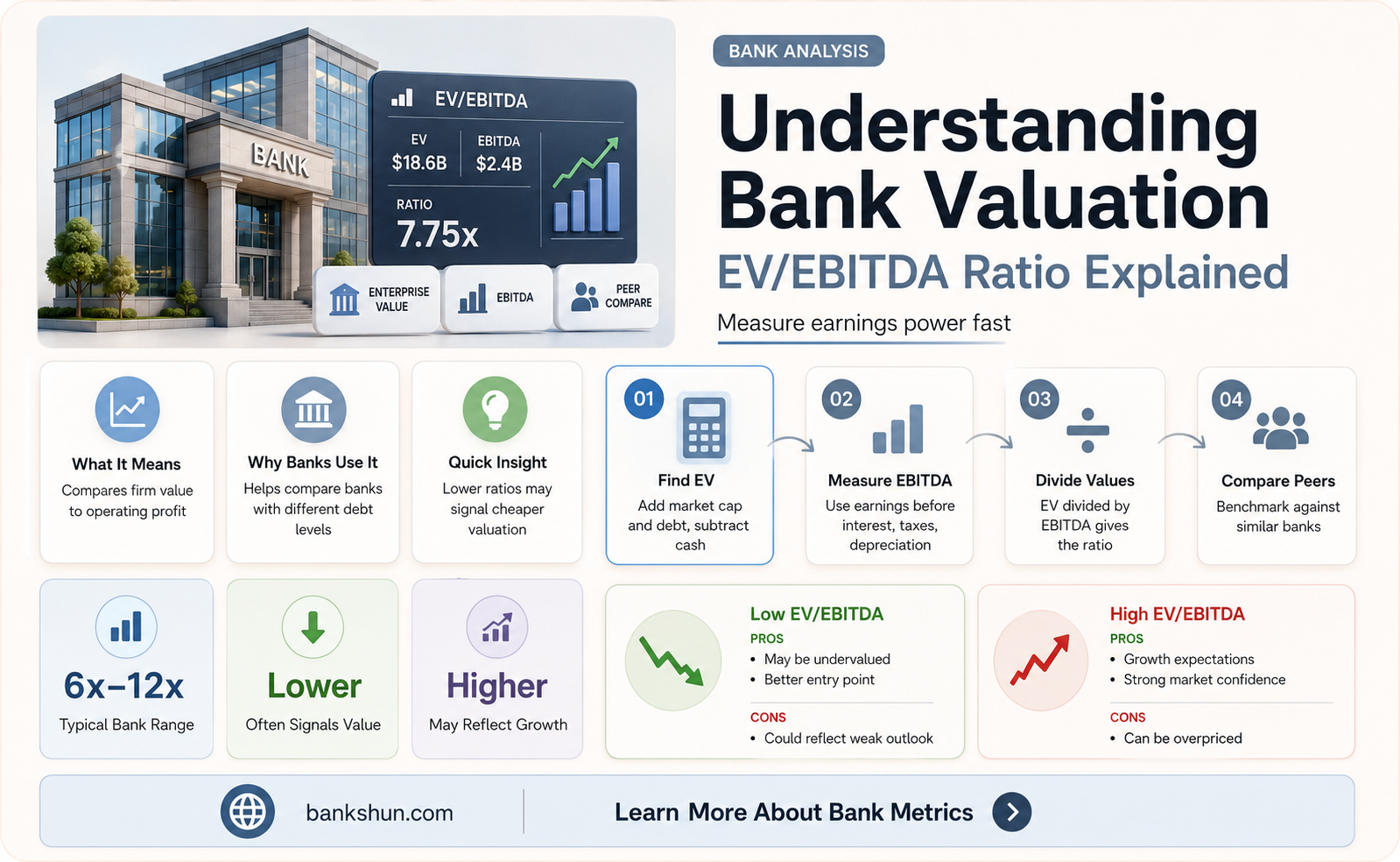

The EV/EBITDA ratio is a crucial tool in company valuation, especially in investment banking. It is calculated by dividing a company's total worth or Enterprise Value (EV) by its operational profitability or EBITDA (earnings before interest, taxes, depreciation, and amortization). While the ratio is widely used, its effectiveness as a tool to assess a company's financial position depends on the industry and other factors. In the case of banks, EBITDA is not considered a vital metric because it does not reflect a bank's true performance, as a bank's main source of revenue is financial revenue.

| Characteristics | Values |

|---|---|

| Use | Evaluating the cash and debts of a company |

| Comparison with P/E ratio | P/E ratio only considers equity value, whereas EV/EBITDA considers capital structure and debt |

| EBITDA's strength | Ability to neutralise differences in tax rates, depreciation schedules, and financing structures |

| EBITDA's weakness | It does not account for capital expenditures or changes in working capital |

| Usefulness of EV/EBITDA ratio | Provides a clearer picture of a company's value to a potential acquirer, including assumed debt |

| Usefulness of EV/EBITDA ratio | Provides a measure of comparability in a way that is not necessarily available from other metrics |

| Usefulness of EV/EBITDA ratio | Particularly useful when evaluating companies within the same industry |

| EBITDA's relevance in the banking industry | Not a vital metric because earnings before interest do not reflect a bank's true performance |

Explore related products

$71.18 $90

$21.49 $27.95

$89.99 $131

What You'll Learn

![]()

EBITDA is a poor metric for banks

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a financial ratio that shows a company's operational profitability before taking into account its financial management, taxes, and depreciation or amortization. It is a widely used metric for evaluating a company's performance and profitability. However, when it comes to the banking industry, EBITDA is not considered a very important metric. Here are several reasons why EBITDA is a poor metric for banks:

- Interest Exclusion: Banks have specific revenue streams, including interest and fees. The interest earned by banks is a crucial component of their earnings, and excluding it from calculations can distort the true financial picture. EBITDA's exclusion of interest income can make it a less relevant metric for banks compared to other industries.

- Regulatory Considerations: The banking industry operates under stringent regulations that may not be adequately captured by EBITDA. Other metrics, such as pre-provision net revenue (PPNR) and return on tangible common equity (ROTCE), are more closely aligned with the unique regulatory environment in which banks function.

- Capital Intensive Nature: Banks are capital-intensive businesses, and the impact of income taxes, depreciation, and amortization can significantly affect their performance. EBITDA's exclusion of these factors may not provide an accurate representation of a bank's financial health and sustainability.

- Alternative Metrics: In the banking industry, there are alternative metrics that are more closely tied to the specific dynamics of the industry. For example, CAMELS (an assessment framework for financial institutions) focuses on asset-liability matching and ensuring that cash outflows are covered by inflows. These industry-specific metrics may provide a more accurate evaluation of a bank's performance.

- Manipulation Concerns: EBITDA has been criticised for its potential to be manipulated and for oversimplifying a company's financial health. The exclusion of interest, taxes, depreciation, and amortization can make unprofitable firms appear fiscally healthy. This manipulation concern is particularly relevant in the banking industry, where transparency and accurate financial reporting are critical.

- Long-Term Sustainability: EBITDA does not account for capital expenditures or changes in working capital, which are critical factors in assessing a bank's long-term sustainability. Banks have unique capital requirements and liquidity needs that EBITDA may not adequately capture.

While EBITDA has its limitations as a metric for banks, it is important to note that it still has its uses. EBITDA can be useful for comparing companies across different industries, normalising for differences in tax rates, depreciation schedules, and financing structures. However, when specifically evaluating banks, it is essential to consider a range of industry-specific metrics that capture the unique aspects of the banking industry.

US Bank's Acquisition of State Farm Bank: What's Next?

You may want to see also

Explore related products

$45.78 $100

![]()

EV/EBITDA is a capital structure-neutral ratio

The EV/EBITDA ratio is a crucial tool in company valuation, especially in investment banking. It is calculated by dividing a company's total worth or enterprise value (EV) by its operational profitability or EBITDA. This ratio reveals a company's value based on its capacity to generate earnings.

EV/EBITDA is considered capital structure-neutral because EBITDA is capital structure-neutral. EBITDA is an earnings figure that ignores capital structure. It is calculated before accounting for interest expense, meaning it does not discriminate between equity holders and debt holders. EBITDA also neutralizes differences in tax rates, depreciation schedules, and financing structures, making it useful for comparing profitability across companies and industries.

EV, on the other hand, adds debt to market capitalisation, which may seem like it would result in a higher EV/EBITDA ratio for companies with more debt. However, this is not necessarily the case. A company with a lot of debt would have a higher EV/EBITDA ratio only if the cash flows available to equity holders were the same regardless of debt, which is not how debt works. Therefore, the EV/EBITDA ratio can be considered capital structure-neutral.

The EV/EBITDA ratio is particularly useful for comparing companies within the same industry, as it accounts for differences in capital structures that might skew other metrics like the P/E ratio. It is also useful for cross-border comparisons since it excludes taxes. However, it should not be used in isolation, as capital expenditure requirements, working capital needs, and growth prospects are also important when evaluating a company's fundamentals.

Who Holds the Reins at the World Bank?

You may want to see also

Explore related products

$85.31 $105

![]()

EV/EBITDA is useful for cash flow-based valuations

The EV/EBITDA ratio is a crucial tool in company valuation, offering a clear and standardised method of determining a company's worth and potential for future development and growth. It is particularly useful for cash flow-based valuations as it provides a rough approximation of cash flow. EBITDA, or Earnings Before Interest, Taxes, Depreciation, and Amortization, is a financial ratio that reflects a company's operational profitability before considering its financial management.

The EV/EBITDA ratio is calculated by dividing Enterprise Value (EV) by EBITDA. EV refers to the total worth of a company, including market capitalization, debt, and cash. This ratio is especially useful when evaluating companies within the same industry, as it accounts for differences in capital structures that might skew other metrics like the P/E ratio. It is also beneficial when comparing companies across different industries, as it is expressed in a uniform manner. By excluding taxes, the EV/EBITDA ratio also facilitates more accurate international comparisons.

The ratio is a significant indicator of investment banking, providing insight into a company's financial standing and worth. A high EV/EBITDA ratio suggests that a company is costly in terms of earnings per share, indicating high market expectations for future growth. On the other hand, a low ratio may imply that a company is undervalued or that the market has lower expectations for its growth.

While the EV/EBITDA ratio is a valuable tool, it should not be used in isolation. It is important to consider other factors such as capital expenditure requirements, working capital needs, and growth prospects when evaluating a company's fundamentals. Additionally, the ratio should be applied comparatively within a specific sector, as different industries have varying ratio ranges.

Banks' Legal Duty: Accommodating Customers with Disabilities

You may want to see also

Explore related products

![]()

EV/EBITDA is a fundamental valuation method in investment banking

The EV/EBITDA ratio is a fundamental valuation method in investment banking. It is a widely used ratio for assessing a company's financial performance and market capitalization. The ratio compares the entire value of a business with the amount of EBITDA it earns annually. EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a financial ratio that reflects a company's operational profitability before accounting for financial management, taxes, depreciation, and amortization. It is a crucial measure of a company's ability to generate profits.

The EV/EBITDA ratio is calculated by dividing a company's enterprise value (EV) by its EBITDA. The EV represents the total worth of a company and is determined by considering its market capitalization, debt, and cash reserves. By dividing EV by EBITDA, the ratio reveals a company's value based on its capacity to generate earnings. This ratio is particularly useful for investors as it provides insights into a company's capital structure and operating profitability. It also offers a standardized method for determining a company's worth and potential for future growth.

One of the key advantages of the EV/EBITDA ratio is its ability to facilitate comparisons between companies in different industries. By normalizing valuation metrics, it becomes easier to conduct cross-industry comparisons. However, it is important to interpret the ratio within specific parameters, such as market conditions and the individual company's context. Additionally, the EV/EBITDA ratio should be used in conjunction with other financial metrics and qualitative factors for a comprehensive evaluation.

The EV/EBITDA ratio also serves as an indicator of market expectations. A high EV/EBITDA ratio suggests that a company is costly in terms of earnings per share, indicating high market expectations for future growth. Conversely, a lower ratio may imply that a company is undervalued or that the market has lower growth expectations. It is worth noting that the healthy" range for EV/EBITDA varies across industries, and savvy investors consider industry-specific comparisons.

In summary, the EV/EBITDA ratio is a fundamental valuation tool in investment banking that provides insights into a company's value, profitability, and market expectations. It is widely used for assessing financial performance and facilitates comparisons across industries. However, it should be interpreted within specific contexts and in combination with other financial metrics for a comprehensive understanding of a company's financial position.

Removing Banks from Apple Pay: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

EV/EBITDA is useful for comparing profitability across companies and industries

The EV/EBITDA ratio is a crucial tool in company valuation and is widely used in the business and investment community. It is a well-established metric that is frequently referenced and discussed in economic research, investment reports, and industry analyses. This ratio is particularly useful for comparing the profitability of companies within the same industry, as it accounts for differences in capital structures that might skew other metrics like the P/E ratio.

The EV/EBITDA ratio is calculated by dividing Enterprise Value (EV) by EBITDA. EV refers to the total worth of a company, including market capitalization, debt, and cash. EBITDA is a financial ratio that shows a company's operational profitability before considering its financial management, taxes, and depreciation or amortization. It is a measure of a company's ability to generate profit and is useful for comparing profitability across companies and industries.

The EV/EBITDA ratio provides a standardized measure of valuation relative to profitability, aiding in normalizing the assessment process. It offers a more accurate representation of a company's operational effectiveness by excluding certain financial factors that can vary significantly between companies or distort true profitability. By removing these items, EBITDA allows for better comparability across companies and industries. A low EV/EBITDA ratio may indicate that a company is undervalued, while a high ratio may suggest overvaluation.

When using the EV/EBITDA ratio, it is important to compare companies within the same sector, as industry norms can vary widely. Additionally, it is recommended to analyze the ratios over a period of 5-10 years to eliminate any unusual data points or outliers. While the EV/EBITDA ratio is a useful tool, it should not be used in isolation. Investors should consider other financial ratios and qualitative factors, such as capital expenditure requirements, working capital needs, and growth prospects, to gain a holistic view of a company's fundamentals.

Robbing Banks: Federal Crime or State Jurisdiction?

You may want to see also

Frequently asked questions

No, EBITDA is not a common metric in the banking industry. This is because earnings before interest do not reflect a bank's true performance, and there are other metrics more vital to the industry, such as PPNR, CET1, and ROTCE.

P/E and EV/EBITDA are completely different ratios. P/E only considers equity value, whereas EV/EBITDA considers the capital structure and debt. This makes P/E less complete when a company has a lot of debt.

While the "healthy" range varies by industry, in 2024 it ranged from about eight to 30, depending on the sector. A ratio below 10 is often considered attractive, but this is not a hard-and-fast rule.