Cash flow is a critical metric for evaluating a company's financial health and liquidity. It refers to the money that flows in and out of a business, encompassing revenue from sales, expenses, interest, investments, and credit sales. While most companies aim for a positive cash flow, indicating strong financial flexibility and the ability to meet obligations, banks often present a different picture. Operating cash flow in banks is notoriously complex due to their unique business model and accounting practices. Banks' cash flow positions can be influenced by various factors, including loan classifications, investment portfolios, and customer deposits, leading to challenges in comparing banks' financial health based solely on their recorded cash flow.

| Characteristics | Values |

|---|---|

| Nature of cash flow | Money that goes in and out of a business |

| Positive cash flow | More money coming in than going out |

| Negative cash flow | Less money coming in than going out |

| Banks' cash flow | Varies based on how they classify loans and investments |

| Operating cash flow | Refers to money from a business's operations |

| Investing cash flow | Refers to money from investment activities |

| Financing activities | Another category of cash flow |

| Banks' classification methods | Can impact the appearance of their cash flow position |

| Customer-driven deposits | Should be included in operating cash flow, according to researchers |

Explore related products

What You'll Learn

![]()

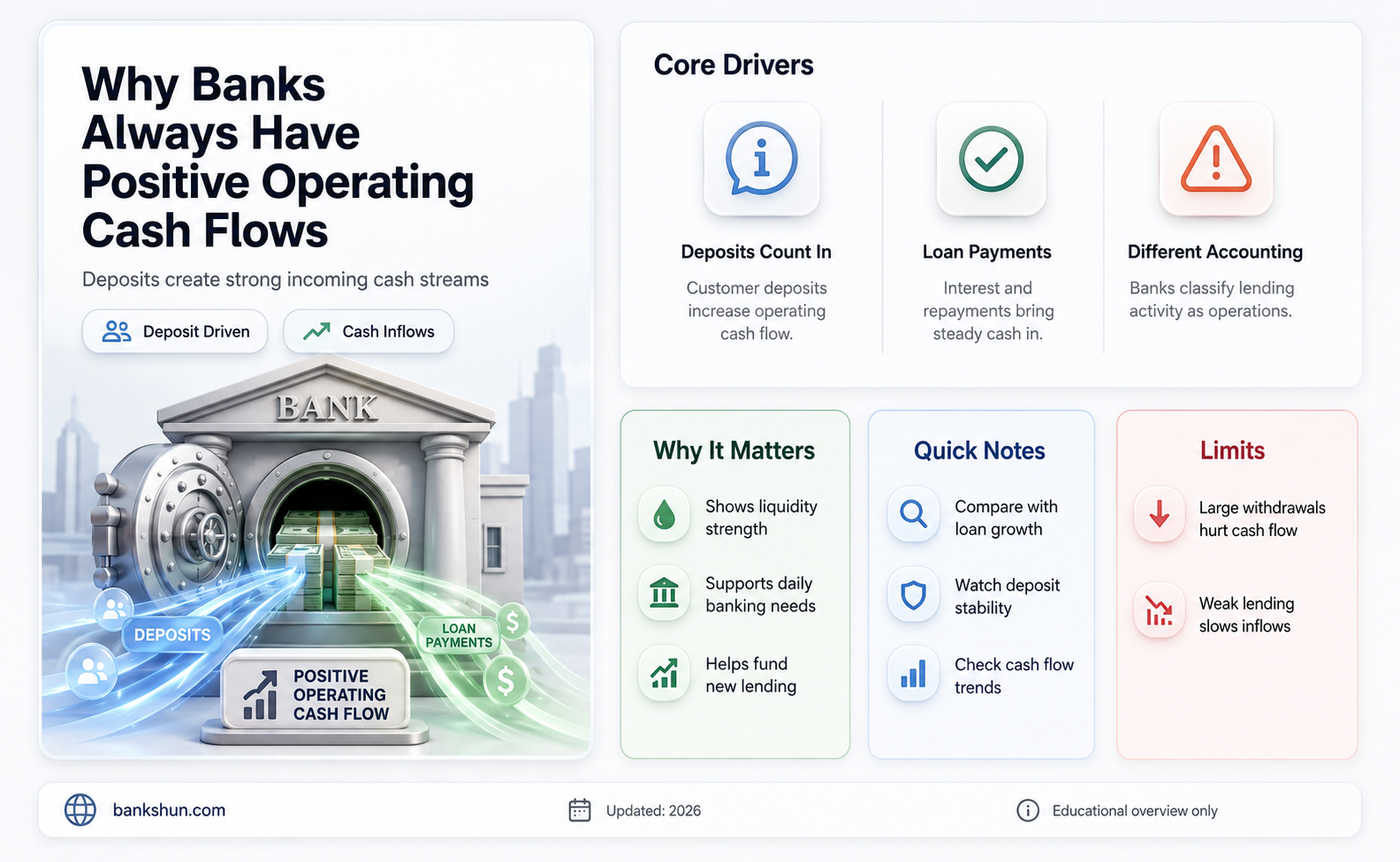

Banks' cash flow reports vary

In general, cash flow refers to the money that goes in and out of a business. It is calculated by taking cash received from sales and subtracting operating expenses paid in cash for the period. Positive cash flow indicates that a company's liquid assets are increasing, enabling it to cover obligations, reinvest in its business, and provide a buffer against future financial challenges.

However, in the case of banks, operating cash flow is largely ignored by analysts. Banks' cash flow reports are not always comparable to each other, and their recorded cash flow from operations can vary significantly. This is because banks have the flexibility to classify certain loans differently, which can impact how loans and securities are accounted for in their cash flow statements.

Additionally, banks' cash flow reports may not accurately reflect customer-driven deposits, which are crucial to a bank's operations and financial health. As a result, banks' cash flow reports can vary significantly, and it is challenging to make direct comparisons between different banks based solely on their recorded cash flow from operations.

Citing World Bank Data: A Quick Guide

You may want to see also

Explore related products

![]()

Operating cash flow is a bad metric for banks

Firstly, a bank's operating income is often relatively small compared to their high operating expenses, resulting in a negative operating cash flow. This negative cash flow, however, does not accurately reflect the bank's financial health or ability to meet obligations. Banks maximize future cash flows by lending as much as possible, leveraging time value and interest.

Secondly, banks have significant control over how they classify loans, which can drastically impact their cash flow. For example, a loan can be classified as "for investment" or "for sale," each with distinct effects on cash flow calculations. This flexibility in classification can skew the interpretation of operating cash flow and make it challenging to compare banks' financial positions accurately.

Additionally, bank statements provide a historical record of transactions but fail to offer a real-time or predictive view of a company's financial position. They do not account for timing differences, in-transit transactions, or future payments, leading to gaps in understanding week-to-week cash flow and hindering effective cash flow management.

For these reasons, operating cash flow, while important, should be considered alongside other financial metrics and forecasts for a comprehensive understanding of a bank's financial health and prospects.

The Bank of the US: A Historical Perspective

You may want to see also

Explore related products

![]()

Customer-driven deposits impact operating cash flow

Customer deposits represent a critical aspect of financial reporting for many businesses. They are a common practice across various industries and can significantly impact a company's cash flow and revenue recognition processes. These deposits are essentially prepayments for goods or services, providing an influx of cash before the actual sale occurs. This immediate liquidity can be advantageous for managing day-to-day operations, purchasing inventory, or investing in capital improvements.

From a cash flow perspective, customer deposits can provide a company with a source of liquidity, which can be particularly beneficial for cash-strapped businesses. However, it is important to distinguish that this influx of cash is not equivalent to revenue earned and should not be confused with income. Revenue is only recognized when the transaction is completed, and the goods or services are provided. This distinction is crucial for accurate financial reporting and compliance with accounting principles.

The timing of cash flows from customer deposits can also affect financial planning. For instance, businesses with seasonal fluctuations can utilize deposits received during peak periods to sustain operations during slower months. Conversely, a sudden influx of deposits may require the business to quickly scale up operations, necessitating careful cash flow management to meet the increased demand without compromising financial stability. To maintain a healthy cash flow balance, companies may employ strategies such as staggered billing or milestone payments, ensuring a steady stream of cash inflows.

The recognition and classification of customer deposits in financial reporting are crucial. Customer deposits are recorded as current liabilities on the balance sheet, reflecting the company's obligation to either return the funds or fulfill the contract. If the company expects to provide the goods or services within a year, the deposits are classified as current liabilities. However, if the timeline extends beyond a year, they are considered long-term liabilities, impacting the company's liquidity ratios and influencing investor perception and creditworthiness assessments.

Effective management of customer deposits is essential for maintaining a healthy balance sheet and ensuring compliance with accounting standards and tax regulations. Technological advancements, particularly in fintech, are reshaping how businesses track and manage these deposits, offering more sophisticated tools for accurate reporting and compliance. By adopting comprehensive risk management strategies, businesses can safeguard customer deposits and fulfill their obligations.

The Written Word or Numbers: How Do Banks Operate?

You may want to see also

Explore related products

![]()

Banks' investment portfolios affect cash flow

Banks' investment portfolios can have a significant impact on their cash flow. A bank's investment portfolio comprises various investments, including securities, assets, and financial market activities. These investments are essential for banks to generate income and maximize future cash flows.

Firstly, banks need to classify their securities into two main categories: "held for maturity" (HTM) and "available for sale" (AFS). Changes in the fair market value of these securities directly affect the income statement, impacting the bank's current income or expenses. For instance, a decrease in the value of investment securities held as assets can result in unrealized losses, negatively affecting the bank's liquidity and capital position.

Secondly, banks must effectively manage their investment portfolios to maintain sufficient liquidity. This involves ensuring enough liquid assets to meet their obligations and withstand fluctuations in interest rates. Rising interest rates can complicate banks' investment portfolios by increasing the cost of liabilities and reducing the value of fixed-rate bonds held as investments. In such cases, banks might be forced to sell "underwater" bonds, realizing losses and further impacting their cash flow.

Additionally, diversification is a crucial aspect of bank investment portfolios. By allocating their assets across a variety of investment types, banks can mitigate interest rate risk. For example, some banks invest only about 25% of their assets in diverse investments to reduce their overall risk. This strategic diversification helps protect the bank's capital and maintain a stable cash flow, even during economic fluctuations.

Furthermore, a well-managed investment portfolio enables banks to achieve their financial goals and objectives. It involves implementing a sound risk management framework to identify, monitor, and mitigate the risks associated with their investments. This includes understanding the risks, developing policies to address them, and maintaining transparency about the composition and performance of their investment portfolios.

How Banks Handle Coin Rolls and Customer Requests

You may want to see also

Explore related products

![]()

Positive cash flow benefits beyond the financial

Positive cash flow has several benefits for businesses beyond their financial health. Firstly, it enables a company to cover its obligations, such as paying debts, bills, and operating expenses. This ensures the business can maintain its operations and avoid financial distress. Positive cash flow also allows a company to reinvest in its business, fund research and development, and purchase new inventory. This helps the business stay competitive and responsive to market changes.

Another benefit of positive cash flow is the ability to return money to shareholders. This can increase shareholder confidence and support the company's long-term financial goals. Positive cash flow also provides a buffer against future financial challenges. During economic downturns, companies with strong cash flow are better equipped to weather the crisis and avoid the costs of financial distress.

Additionally, positive cash flow can enhance a company's reputation and creditworthiness. Suppliers, lenders, and partners may view a company with positive cash flow more favourably, leading to improved relationships and potentially better terms in contracts and negotiations. This can further strengthen the company's financial position and growth prospects.

Furthermore, positive cash flow can contribute to a company's operational efficiency. With healthy cash flow, businesses can invest in systems and technologies that improve productivity, streamline processes, and reduce administrative burdens. This can free up resources for more strategic initiatives and revenue-generating opportunities.

While the financial implications of positive cash flow are significant, the benefits extend beyond a company's financial health. Positive cash flow supports a business's overall stability, adaptability, and long-term sustainability, contributing to its success and resilience in the marketplace.

How Banks Create Risk: Internal vs External Factors

You may want to see also

Frequently asked questions

Cash flow refers to the money that goes in and out of a business. It can be categorized as cash flows from operations, investing, and financing.

Banks can change the loan status to "for investment" or "for sale", which has drastic effects on how those items are reflected in their cash flow statements. Banks maximize future cash flows by lending as much money as possible and taking advantage of interest.

Banks can monitor their operating, investing, and financing activities through online banking and mobile apps. They can also refer to monthly statements to gain additional insights into their cash flow.

Banks' cash flow reports differ in how they designate their various cash flows as operating, investing, or financing activities. Additionally, current accounting rules allow banks to make non-cash transfers between investment classifications, impacting how loans and securities are accounted for in their cash flow statements.