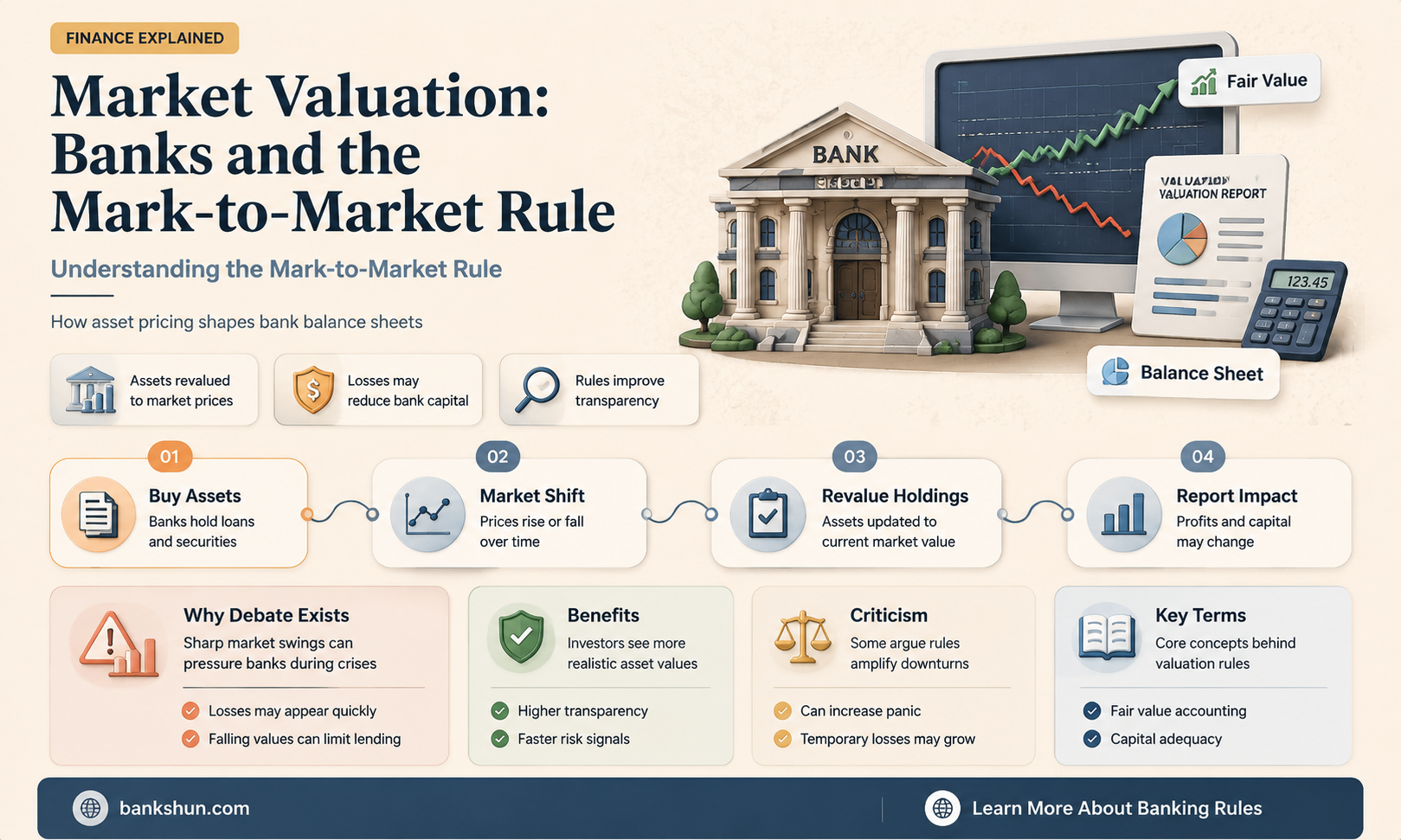

Mark-to-market (MTM) accounting is a method of measuring the fair value of accounts that can fluctuate over time, such as assets and liabilities. It is a way of valuing these accounts based on current market conditions and their current buy or sell price, rather than their original price. MTM is crucial for providing transparency and accuracy in financial statements and can be used to adjust loan portfolios based on credit risk. However, it can also introduce significant volatility during market disruptions. While MTM accounting has become fundamental to modern accounting and investment practices, it is not mandatory for all financial institutions.

| Characteristics | Values |

|---|---|

| Definition | Mark-to-market (MTM or M2M) is a method of measuring the fair value of accounts that can fluctuate over time, such as assets and liabilities. |

| Synonyms | Fair value accounting, marking to market, market value accounting (MVA) |

| Origin | Futures trading |

| Purpose | To provide a real-time snapshot of financial worth and transparency and accuracy in financial statements |

| Advantages | Provides greater transparency about an organization's true financial position |

| Disadvantages | Introduces significant volatility during market disruptions; most bank assets are difficult to measure at market value; can trigger a margin call |

| Regulatory Bodies | Financial Accounting Standards Board (FASB) |

| Regulatory Changes | In 2015, FASB gave final approval to an accounting standard that is limited in its requirement for MTM. In 2018, this standard, "classification and measurement", became effective and requires all equity investments to be treated as trading securities. |

Explore related products

What You'll Learn

![]()

Mark-to-market accounting (MTM)

MTM originated in futures trading but has become fundamental to modern accounting and investment practices. When banks, investment firms, or corporations use MTM accounting, they're essentially asking: "What is this asset worth if we had to sell it right now?" MTM accounting can provide greater transparency about an organization's true financial position, but it can also introduce significant volatility during market disruptions. It is crucial for providing transparency and accuracy in financial statements.

The Financial Accounting Standards Board (FASB) provides guidelines for MTM under generally accepted accounting principles (GAAP). MTM can lead to volatility in financial statements during unstable market conditions. MTM accounting is based on the principle of fair value accounting, which prioritizes current market prices over historical costs. This method regularly updates asset and liability valuations to ensure financial statements reflect an organization's true financial position.

Financial institutions use MTM accounting to adjust their loan portfolios based on credit risk. When a bank issues loans, it creates an "allowance for credit losses" account that cushions against expected defaults. As loan quality deteriorates, the bank increases this allowance, effectively marking down the value of its receivables even before actual defaults occur.

Masks at Simmons Bank Arena: What You Need to Know

You may want to see also

Explore related products

![]()

Fair value accounting

Mark-to-market (MTM) or fair value accounting is a method of measuring the "fair value" of accounts that can fluctuate over time, such as assets and liabilities. It is a valuation method that values assets and liabilities based on what they could be bought or sold for in today's marketplace rather than their original price. This approach provides a real-time snapshot of financial worth, like checking an investment portfolio's value on a given day.

The Financial Accounting Standards Board (FASB), the chief rule-making body for accountants, has played a significant role in promoting fair value accounting. FASB's guidelines allow for the valuation of assets and liabilities based on orderly market prices rather than forced liquidation prices. Additionally, FASB's inclusion of more members from the financial services industry has contributed to the increased popularity of fair value accounting.

While fair value accounting offers advantages, it also has some limitations. One of the main issues is the potential for large swings in value, especially when dealing with volatile assets. Another concern is that the observed market value of an asset may not always reflect its fundamental value. Additionally, fair value accounting can lead to increased costs for banks as estimating market values for non-traded assets and liabilities can be complex and vary across institutions.

PNC Banks in Jacksonville, FL: Locations and Services

You may want to see also

Explore related products

![]()

Market value accounting (MVA)

MVA is calculated by finding the difference between the market value of a company and the capital contributed by all investors, including bondholders and shareholders. It is a metric used to measure wealth and determine how much value a firm has accumulated over time. A positive MVA indicates that the company's management has increased the value of capital contributed by shareholders, while a negative MVA indicates that management actions have diminished this value.

MVA is important because it provides a real-time snapshot of a company's financial worth and can indicate its ability to create wealth for its stakeholders. It is particularly relevant for investors and lenders who use it to assess the value of a company and determine its credit risk.

However, there are challenges associated with MVA. Most bank assets, such as small commercial loans, are not actively traded, making it difficult to determine their market value. Additionally, there is no standardised method for valuing non-traded liabilities, leading to potential inconsistencies across banks. Implementing MVA can also be costly for banks as each market value estimate must be done on a case-by-case basis.

The Oldest Bank in the USA: A Historical Perspective

You may want to see also

Explore related products

![]()

Mark-to-market and banker's bonuses

Mark-to-market (MTM) or fair value accounting is a method of valuing assets and liabilities based on current market conditions. It is a way of measuring the "fair value" of accounts that can fluctuate over time. MTM accounting is based on the principle of fair value accounting, which prioritises current market prices over historical costs. This method regularly updates asset and liability valuations to ensure financial statements reflect an organisation's true financial position.

MTM accounting is crucial for providing transparency and accuracy in financial statements. It originated in futures trading but has become fundamental to modern accounting and investment practices. When banks, investment firms, or corporations use MTM accounting, they ask: "What is this asset worth if we had to sell it right now?".

However, MTM accounting can also introduce significant volatility during market disruptions. It can lead to volatile financial statements during unstable market conditions. During the 2008 financial crisis, many securities held on banks' balance sheets could not be valued efficiently as the markets had disappeared from them.

MTM accounting can also impact bankers' bonuses. During January 2010, Adair Turner, Chairman of the UK's Financial Services Authority, said that marking to market had been a cause of exaggerated bankers' bonuses. This is because it produces a self-reinforcing cycle during an increasing market that feeds into banks' profit estimates.

Furthermore, MTM accounting can eliminate the incentive for an accounting abuse known as "gains trading." Banks that gains trade tend to sell securities with unrealized gains, bolstering income and book capital, while keeping securities with unrealized losses on the books at historical cost, thereby keeping book capital artificially high. MTM accounting can also serve as a financial reality check during normal times, but it can become a self-fulfilling prophecy during market panics when liquidity disappears.

PNC Bank's Headquarters: Address and Location

You may want to see also

Explore related products

$44.95 $42.95

![]()

Mark-to-market and loan portfolios

Mark-to-market (MTM) is a method of measuring the fair value of accounts that can fluctuate over time, such as assets and liabilities. MTM accounting is a valuation method that values assets and liabilities based on what they could be bought or sold for in today's marketplace rather than their original price. This approach gives a real-time snapshot of financial worth, like checking your investment portfolio's value on a given day. MTM originated in futures trading but has become fundamental to modern accounting and investment practices.

When banks, investment firms, or corporations use MTM accounting, they ask: "What is this asset worth if we had to sell it right now?" MTM accounting can provide greater transparency about an organization's true financial position. However, it can also introduce significant volatility during market disruptions. MTM is crucial for providing transparency and accuracy in financial statements.

Financial institutions use MTM accounting to adjust their loan portfolios based on credit risk. When a bank issues loans, it creates an "allowance for credit losses" account that cushions against expected defaults. As loan quality deteriorates, the bank increases this allowance, effectively marking down the value of its receivables even before actual defaults occur.

The level of interest rates and the shape of the yield curve impact the value of loans that can be revealed when marking loans to market. Each basis point increase in rates decreases the lifetime value of a fixed-rate loan to a bank. Marking loans to market would be the same process as the AOCI for fixed-rate securities. The longer the fixed rate, the more sensitive the loan is to negative economic adjustment.

Community banks are experiencing approximately six to eight times higher negative AOCI from their loan portfolios than their securities portfolio. Marking investments to current value provides a consistent and actionable feedback loop. As rates rise, bankers act to mitigate the risk embodied in the portfolio's performance.

Banks' Confidentiality: Commercial Lending and Customer Privacy

You may want to see also

Frequently asked questions

Mark-to-market (MTM) accounting is a method of measuring the "fair value" of accounts that can fluctuate over time, such as assets and liabilities.

MTM accounting values assets and liabilities based on what they could be bought or sold for in today's marketplace rather than their original price. This approach provides a real-time snapshot of an organization's financial worth.

MTM accounting provides transparency and accuracy in financial statements. It helps eliminate the incentive for an accounting abuse known as "gains trading," where banks sell securities with unrealized gains while keeping those with unrealized losses to artificially inflate book capital.

The Financial Accounting Standards Board (FASB), the chief rule-making body for accountants, has approved standards that require mark-to-market accounting for certain financial assets and liabilities. However, these standards may not apply to all banks, especially those that are not considered "public business entities."

Most bank assets, such as small commercial loans, are not actively traded, making it difficult to determine their market value. Additionally, there may be significant costs involved in estimating market values for non-traded assets and liabilities, and the comparability of these values across banks could be a challenge.