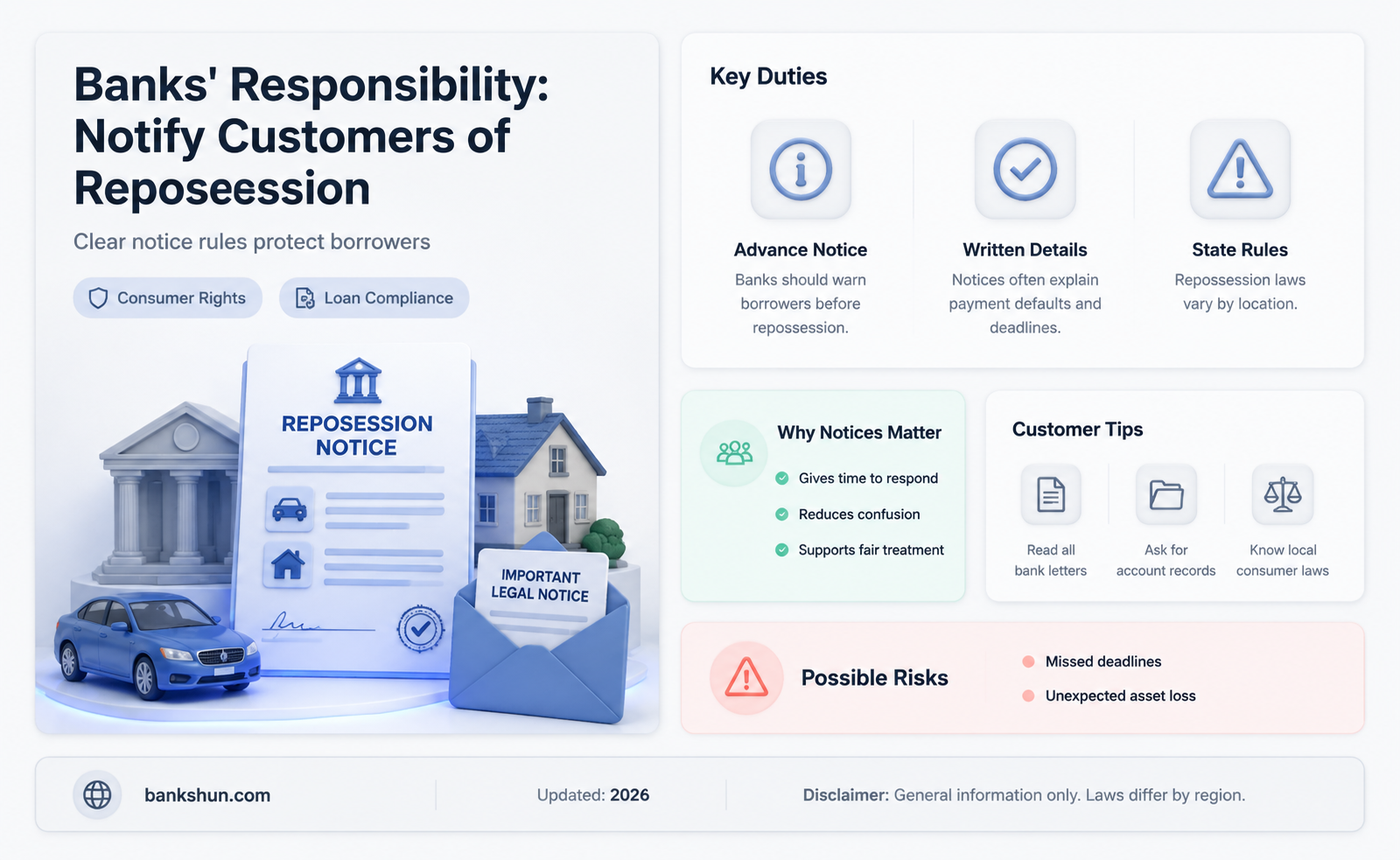

Repossession is a sensitive issue that can be financially and emotionally difficult for the borrower. In the case of car loans, lenders are usually not required to notify borrowers before repossessing their vehicles. However, after repossession, lenders must provide specific notices, such as the right of redemption or reinstatement, the outstanding balance, and the intention to sell the vehicle. In some states, lenders must also notify borrowers of the date, time, and place of a public auction, allowing them to bid on their repossessed vehicles. While repossession laws vary, lenders must ensure the process is lawful, and borrowers have certain rights and protections, including the retrieval of personal belongings from the vehicle.

| Characteristics | Values |

|---|---|

| Do banks have to notify before repos? | In most states, banks are not required to give notice before repossessing vehicles. |

| Do banks have to notify after repos? | Yes, banks must notify after repossessing a car. |

| What are the borrower's rights after repos? | The borrower has the right to be notified before their vehicle is sold or kept as compensation for their debt. They also have the right to buy back the vehicle. |

| What are the lender's obligations after repos? | The lender must provide written notice of the borrower's right of redemption and/or reinstatement, the outstanding balance of the loan, and the intended sale date. |

Explore related products

What You'll Learn

![]()

Lenders don't need to notify before repossessing

Lenders don't need to notify borrowers before repossessing their collateral in many states and situations. This is because loan agreements usually specify that the lender can repossess the collateral when the borrower is late on payments. Most states don't require lenders to give debtors notice before repossession, and courts and law enforcement don't typically monitor the repossession process. This means that borrowers might not know when or where their collateral will be repossessed.

However, there are some exceptions to this. In some states, lenders must notify borrowers before repossession, giving them time to make up missed payments. Additionally, if the borrower is in the military, the Servicemember Civil Relief Act (SCRA) prohibits repossessions without a court order for any auto loan contracts or agreements entered into before their military service.

It's important to note that even if the lender doesn't need to notify the borrower before repossession, they still have certain obligations after the repossession. In most states, the lender must provide specific notices within a short time, usually five days after repossessing the collateral, but before it is sold or auctioned. These notices include the borrower's right of redemption or reinstatement, the outstanding balance of the loan, and the steps to reinstate the loan. If the collateral is sold, the lender must also notify the borrower of how the sale proceeds were applied against the debt and any remaining deficiency balance owed.

Borrowers should also be aware that they have certain rights after their collateral has been repossessed. They have the right to be notified before their collateral is sold or kept as compensation for their debt, and they may have the opportunity to buy it back. Additionally, if the lender has previously accepted late payments, the borrower may be able to raise this as a defense if the lender sues for a deficiency balance.

In summary, while lenders don't always need to notify borrowers before repossessing their collateral, there are exceptions to this, and lenders still have certain obligations after the repossession. Borrowers also have rights and options to resolve the situation, such as negotiating with the lender or consulting with an attorney if they believe the repossession was unlawful.

The Friendship Between Sasha Banks and Ronda Rousey

You may want to see also

Explore related products

![]()

Lenders must notify after repossessing

In most states, lenders are not required to notify debtors before repossessing vehicles. However, they must provide specific notices after repossession. This typically includes the right of redemption or reinstatement, the outstanding balance of the loan, and the lender's intention to sell the vehicle. The lender must also disclose the time, date, and location of a public auction, allowing the debtor to bid on the repossessed property. If the lender sells the car privately, the debtor may have the right to know the sale date.

In some states, lenders are required to notify debtors before repossession, providing information on missed payments and allowing time to rectify the situation. This is particularly relevant for active-duty servicemembers, as the Servicemember Civil Relief Act (SCRA) prohibits repossession without a court order.

It is important to note that lenders must sell repossessed vehicles in a commercially reasonable manner, and debtors can consult an attorney if they believe the sale price is unreasonable. Debtors may also have the opportunity to buy back the vehicle before it is sold or make up overdue payments to retrieve the repossessed car, depending on state law.

Additionally, lenders cannot immediately sell or keep personal property found inside a repossessed vehicle. They must notify the debtor of the personal items and provide instructions on how to retrieve them.

Danske Bank Sterling Notes: Legal Tender?

You may want to see also

Explore related products

![]()

Lenders must notify before selling

In most states, lenders are not required to notify debtors before repossessing vehicles. In fact, the repossession may take place without warning or a court order. However, there are some exceptions to this. If you are in the military, the creditor must usually obtain a court order before repossessing your car. In this case, you will likely receive notice of the legal process. Additionally, some loan agreements specify that the lender can repossess the car if you are late with payments, outlining how far behind you must be before repossession occurs.

After repossessing the car, lenders must provide specific notices. They must inform you of your right of redemption and/or reinstatement, as well as the outstanding balance of the loan, including all fees and charges. If you have the right to reinstate the loan, they must inform you of the amount required to do so and the steps to take. If the lender intends to sell the car, they must notify you of this intention. If the car is sold at a public auction, the lender must inform you of the time, date, and location, allowing you to attend and bid. If the lender sells the car privately, you may have the right to know the date of the sale.

In some states, you may be able to make up overdue payments to get back your repossessed car or buy it back before it is sold. If the lender sells the car, they must explain how the sale proceeds were applied against your debt. If the sale amount does not cover the loan balance and costs, the creditor must notify you of the remaining balance, known as the "deficiency balance," and may take further action, such as suing you for the balance. On the other hand, if the sale results in a surplus, the creditor must inform you of the surplus amount and pay it to you or a co-signer, if applicable.

Banking Services: Are They All the Same?

You may want to see also

Explore related products

![]()

Lenders must notify of any surplus

In most states, lenders are not required to notify debtors before repossessing vehicles. However, they must provide specific notices after repossession, including the right of redemption and/or reinstatement, the outstanding balance, and the intention to sell the vehicle. If the lender sells the car privately, you may have the right to know the sale date.

In the case of a foreclosure, if the property sells for more than what is owed, the homeowner may be entitled to claim any surplus funds after other debts and liens are paid. This process depends on whether the foreclosure was nonjudicial or judicial. If it was nonjudicial, the lender appoints a foreclosure trustee to manage any surplus funds. If it was judicial, the court assigns a foreclosure officer to handle the distribution.

Surplus funds represent the equity built up in the home. To claim these funds, the former homeowner must follow specific procedures, which vary by location, and act quickly as deadlines apply. If the surplus funds go unclaimed, they may be transferred to the state or other designated parties after a certain period.

In the context of car repossession, if the sale amount exceeds the loan balance and costs, the creditor must notify you of the surplus and pay it to you, unless there is a co-signor with rights to the excess.

Egg Inc: Best Time to Prestige Your Farm

You may want to see also

![]()

Lenders must return personal items

In most states, lenders are not required to notify debtors before repossessing their vehicles. However, after the repossession, lenders must provide specific notices, including the right of redemption and reinstatement, the outstanding balance of the loan, and the intention to sell the vehicle.

Now, regarding personal items left inside a repossessed vehicle, it is important to understand your rights. Firstly, you have the legal right to retrieve your personal belongings from a repossessed vehicle. Repo companies cannot keep or sell your personal property, and they are required to provide reasonable access for you to collect your items.

If the repo company refuses to cooperate, here are some steps you can take:

- Contact the lender: Explain the situation and request their assistance in resolving the issue, as they hired the repossession company.

- Notify the state attorney general's office: Report the repo company for violating state laws regulating repossession.

- File a complaint: Contact a consumer protection agency, such as the Federal Trade Commission (FTC) or a state-level agency, to address unfair or illegal practices.

- Take legal action: If your belongings are not returned or are damaged, you can sue the repo company in small claims court.

It is important to act quickly to protect your rights and retrieve your personal belongings. In some cases, the repo company may charge a storage fee if there is a significant delay in collecting your items. Additionally, ensure you have proof that your personal items were in the repossessed vehicle, as you will need to establish this if any items go missing.

PNC Coin Counting Services: Available at Branches?

You may want to see also

Frequently asked questions

No, in most states, car loan lenders are not required to give debtors notice before repossessing vehicles. However, if there is a pattern of accepting late payments, the bank might have waived its right to repossess the car.

Yes, in most states, the bank must notify you, in writing, within a short time, usually five days after repossessing the car, but before it is sold or auctioned.

The lender must provide you with written notice of your right of redemption and/or reinstatement. They must also inform you of the amount of the outstanding balance of the loan, including all fees and charges.

You may be entitled to buy back the vehicle by paying the full loan amount, plus the repossession costs, before the sale. This is sometimes referred to as redemption.

If you believe your repossession is an error, contact your lender or servicer immediately. If you're unable to resolve it, you can submit a complaint and/or pursue legal action in court or with the help of an attorney.