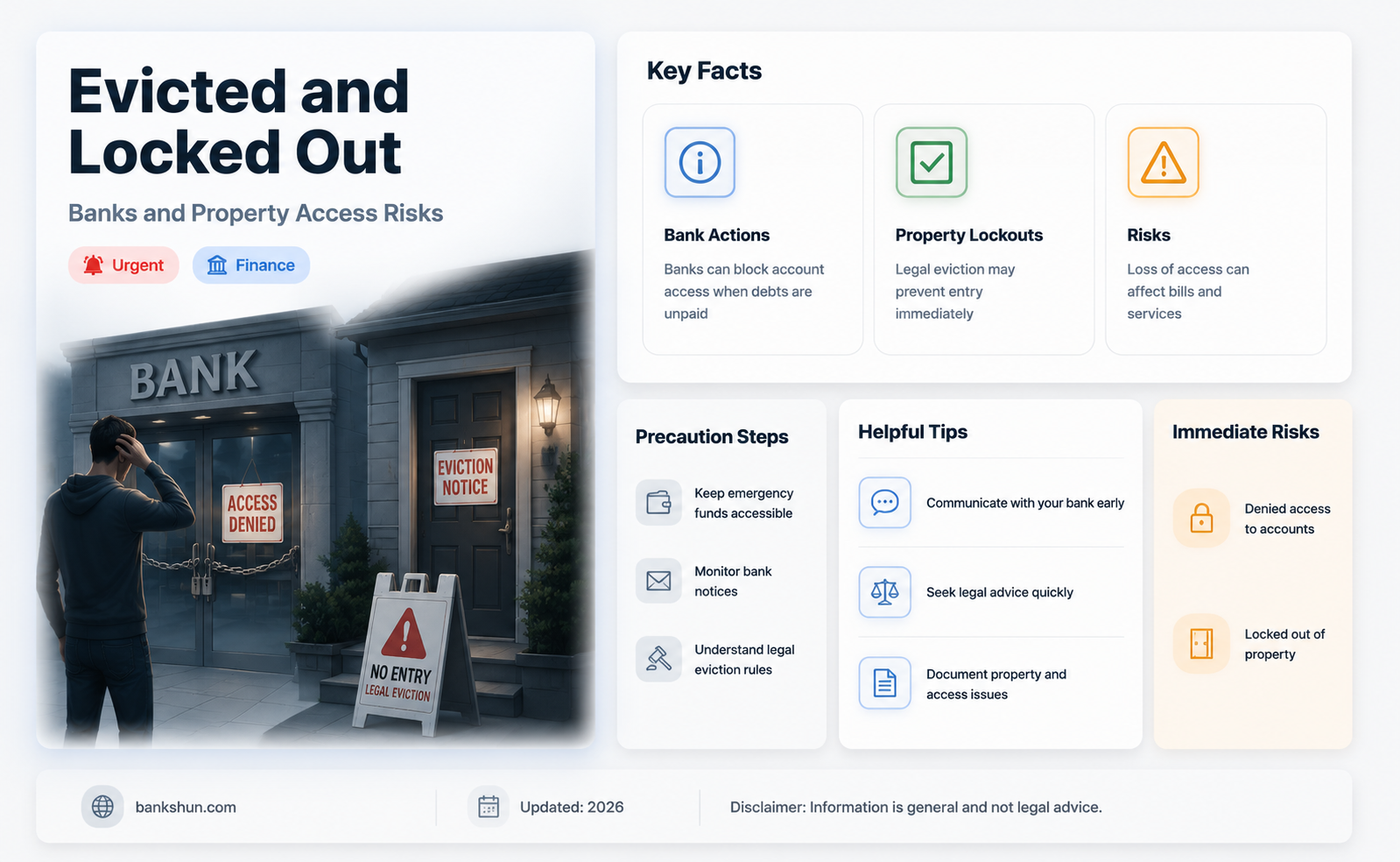

When a bank forecloses on a property, it becomes the new owner and will typically move to sell the property as soon as possible. This often results in the eviction of anyone living on the property, including tenants. The bank must obtain a court order and file for eviction, and cannot change the locks or padlock the door if the property is occupied. However, if the property is vacant, the bank can take steps to secure it, such as changing locks or boarding up doors. The laws regarding foreclosure and eviction vary from state to state, and it is important to research local regulations.

| Characteristics | Values |

|---|---|

| Can banks lock the doors of an eviction property? | Banks cannot lock the doors of an eviction property if it is still occupied. |

| Can banks evict people from the property? | Banks can evict people from the property by getting a court order. |

| Can banks evict tenants from a rented property? | Banks can evict tenants from a rented property if the landlord defaults on their loan. |

| Can banks evict tenants without notice? | Banks cannot evict tenants without notice. A written notice is usually given with a deadline to vacate, which can range from 3 to 30 days. |

| Can banks evict tenants with notice? | If a tenant refuses to leave after the notice period, banks can file an eviction lawsuit. |

| Can banks evict tenants with an eviction lawsuit? | Yes, banks can evict tenants with an eviction lawsuit. |

Explore related products

What You'll Learn

![]()

Banks can't change locks until they own the property

Banks cannot change the locks on an eviction property until they own it. If a homeowner is still living in the house after it is sold in a foreclosure sale, the bank must evict them before changing the locks and taking over the property.

The foreclosure process can be tricky to navigate, and many homeowners are unaware of their rights. Banks may make illegal moves, and oftentimes, homeowners are none the wiser. If a homeowner's locks have been changed and they still live in the home, they have the right to take action. They can replace the lock, notify their lender, or seek legal help. They can also call their loan servicer and tell them that they have been illegally locked out of their home. It is important to note that even during a foreclosure, a homeowner is still responsible for the upkeep of the home.

The ability of banks to change locks on an eviction property depends on whether the property is vacant or occupied. If the house is vacant, the servicer can take steps to secure the property, such as changing locks, on behalf of the lender or subsequent loan owner. This is known as "property preservation". The loan contract usually allows the lender to conduct property inspections and take appropriate action to protect its interest in the property if the homeowner abandons it.

In some states, lenders can request court approval to take possession early if the home appears vacant. Banks may pursue a non-judicial foreclosure or judicial foreclosure, depending on the property's location. It is important to research local laws and regulations to understand the foreclosure process in a specific state.

Small vs Big Banks: Who Wins?

You may want to see also

Explore related products

![]()

They can't evict without a court order

If you're facing eviction, it's important to know your rights. While the specifics of eviction laws vary from state to state, there are some general principles that hold true across the United States. Firstly, understand that a bank cannot evict you from your property without first obtaining a court order and filing for eviction. Even if you've defaulted on your mortgage payments and the bank has initiated foreclosure proceedings, they cannot legally change the locks or kick you out without a court order.

In most states, landlords and banks are required to provide notice before they start an eviction case. This notice will inform you of the reason for the intended eviction and give you a timeframe to resolve the issue, pay rent, or take other corrective actions. If you can work out an agreement with your landlord or bank before they file an eviction claim, that's always a positive outcome. For example, you could apply for rental assistance or seek a loan modification to help with mortgage payments.

If you receive an eviction notice, don't ignore it. Responding to the lawsuit is crucial, as you have the right to present your case to the court and explain why you should not be evicted. You can object to false information and share your side of the story. It's highly recommended to consult a lawyer who can advise you on your specific circumstances and ensure your rights are protected. They can also help you understand local ordinances and state laws that may provide additional protections, such as delaying the eviction process.

Keep in mind that even during a foreclosure, you are still responsible for maintaining the property. If a home appears unoccupied or is falling into disrepair, it may be mistakenly categorized as vacant, which could give the bank or lender the impression that they can change the locks or take possession. Therefore, it's in your best interest to maintain the property as best as you can during this challenging time.

Free ATM Access: Banks That Don't Charge Withdrawal Fees

You may want to see also

Explore related products

$29.99

![]()

Vacant homes can be secured by banks

When a homeowner defaults on their loan, the bank can initiate foreclosure proceedings to recoup past-due loan payments. This typically involves selling the property as soon as possible, which may result in the eviction of tenants or the former owner.

During the foreclosure process, the bank may take steps to secure the property, particularly if it is vacant, as vacant properties are more likely to be vandalized or damaged. These steps can include changing locks, boarding up doorways, replacing or boarding up doors and windows, and turning utilities on or off.

However, it is important to note that the bank cannot change the locks or take other security measures if the homeowner or tenant still occupies the property. Doing so would be illegal, and the occupant should contact their loan servicer and inform them that they have been illegally locked out of their home. To avoid this situation, homeowners or tenants should maintain the property and keep it in good repair, even during the foreclosure process, to avoid it being mistakenly categorized as vacant.

Additionally, banks must follow proper legal procedures to evict occupants, including obtaining a court order and providing written notice with a deadline to vacate the premises. The time frame for this process depends on state law, and in some cases, banks may be required to delay the eviction process or offer assistance programs to help occupants transition to new housing.

Overall, while banks have the right to secure vacant properties during the foreclosure process, they must also respect the rights of occupants and follow the appropriate legal procedures for eviction.

Civil Service Status: Bank of England Employees

You may want to see also

Explore related products

![]()

Banks can pursue judicial or non-judicial foreclosure

Banks can pursue a judicial or non-judicial foreclosure, depending on the location of the property. The bank may also consider other factors, such as whether there are complex issues related to the property, like a dispute over the title.

A judicial foreclosure involves the bank going to court to get a judgment to foreclose on the property. This process may take close to a year, and the borrower can raise defences in court. The lender will bring a lawsuit, and a judge will review the evidence submitted by both sides. A hearing may be held to decide whether the homeowner is in default on the loan. If the court finds in favour of the lender, a judgment of foreclosure will be entered, triggering a foreclosure sale. This may expose the homeowner to a deficiency judgment for any balance remaining on the loan after the sale.

A non-judicial foreclosure does not require the bank to go to court. This process may take only a month or two and is more efficient than a judicial foreclosure. However, if the homeowner raises a defence, the process will move to court. Before initiating a non-judicial foreclosure, the lender must take several steps required by law, including sending letters demanding payment and contacting the borrower to discuss ways to avoid foreclosure. The lender must also inform the borrower of their right to request a meeting to discuss how to avoid foreclosure. After recording a Notice of Default, the lender must send a copy to the borrower within a specified timeframe. The borrower then has a period to "cure" the default, usually by paying what is owed, during which they can negotiate a loan modification or repayment plan. After this period, a Notice of Sale is recorded, stating that the trustee will sell the home at auction.

It is important to note that foreclosure laws vary from state to state, and it is advisable to seek legal advice or consult state-specific resources for more information.

Grand Banks: Glacial Moraine Mystery

You may want to see also

Explore related products

![]()

Evicted tenants may be offered cash for keys

Banks are not in the business of renting to consumers. When a bank forecloses on a landlord, it typically moves to sell the property as soon as possible, which involves evicting tenants—usually with little warning.

Some banks may offer "cash for keys" programs to encourage tenants to vacate the property quickly. This is a legal and ethical alternative to eviction if conducted transparently and consensually. It is also known as the 'Keys for Cash' strategy, and it offers a mutually beneficial solution to avoid the eviction process. The tenant voluntarily hands over the keys to the property in exchange for a financial incentive.

The amount of money offered varies depending on where you live, the cost of living in your location, and local/state laws. Generally, the amount is usually half a month's rent plus the security deposit or a full month's rent. It is important to note that the tenant is not required to accept or sign the Buyout Agreement and may consult an attorney for advice.

Cash-for-keys agreements can be a perfect solution for landlords and tenants who need cash and want to avoid the complicated and expensive eviction process. However, it is a controversial method, and some consider it a predatory tactic used to displace tenants.

Inheritance in Ireland: Do Banks Know?

You may want to see also

Frequently asked questions

Banks can pursue a non-judicial or judicial foreclosure depending on the property's location. They can padlock a vacant home to protect their interest in the property. However, they cannot kick you off the property without a court order and filing for eviction. If you still live in the home, they must take the proper steps to evict you.

If you come home and find the locks changed or the door padlocked, you should call your loan servicer and inform them that you have been illegally locked out of your home. You should also call the field service company, although they will likely refer you back to the servicer.

If your landlord defaults on their loan, the bank can take title to the home and become your new landlord. They will likely move to sell the property and evict anyone living there. You will receive a notice of a new owner and a notice to vacate. You can refuse to leave, but the bank can then file an eviction lawsuit.