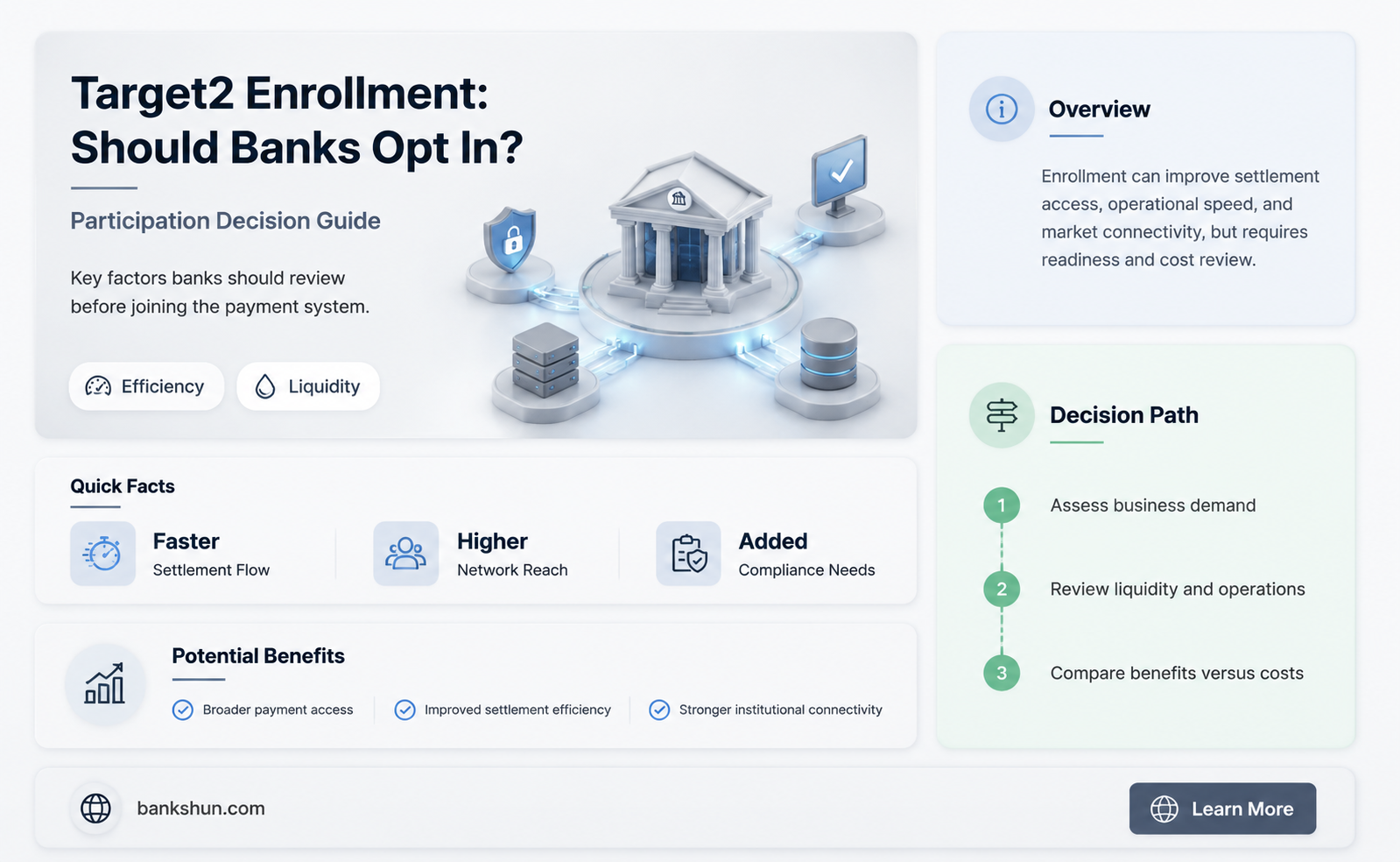

TARGET2 is a payment system that enables banks to transfer money between each other in real time. It is owned and operated by the Eurosystem and used by central and commercial banks to process payments in euros. The system has been in place since 2007 and is used by over 1,000 banks across Europe, making it a widely accepted payment system. TARGET2 is a key component of the infrastructure of the euro, providing a centralised platform for cross-border payments in the European Union. So, do banks need to enroll in TARGET2? The answer is not so straightforward. While TARGET2 is an essential platform for banks conducting transactions in euros, it is not mandatory for banks to use it. However, considering the widespread adoption of TARGET2 and its role in facilitating secure and efficient cross-border payments, it is certainly a system that banks should consider enrolling in to streamline their payment processes.

| Characteristics | Values |

|---|---|

| What is TARGET2? | A payment system owned and operated by the Eurosystem. |

| Who is it for? | Central banks and their national communities of commercial banks. |

| How many banks use it? | More than 1,000 banks across Europe. |

| What is it used for? | Processing large-value payments in euros in real-time. |

| How does it work? | Each bank has its own account within the system. When a bank initiates a transfer, TARGET2 debits the sending bank's account and credits the receiving bank's account. |

| What are the benefits? | TARGET2 provides a centralized platform for businesses to make and receive payments, simplifying the payment process and reducing the need for multiple banking relationships. |

| Who operates it? | France (Banque de France), Germany (Deutsche Bundesbank), and Italy (Banca d'Italia). |

| When did it start? | November 2007. |

| Is it widely accepted? | Yes, TARGET2 is a widely accepted payment system for businesses operating in Europe. |

| How secure is it? | TARGET2 uses advanced security measures to protect against fraud and cyber-attacks. |

Explore related products

![LabelValue.com | Shooting Target Spots - Target Pasters, 2” Circles, Fluorescent Red, [250 Labels/1 Roll] | Great for Target Shooting](https://m.media-amazon.com/images/I/51zFttnwgnL._AC_UL320_.jpg)

What You'll Learn

![]()

Banks must have an account with their national central bank

In the United States, the Federal Reserve System, often shortened to the Federal Reserve or the Fed, acts as the central bank. It was created in 1913 to centralise control of the monetary system and alleviate financial crises. The Federal Reserve is an agency of the federal government that reports to and is directly accountable to Congress. It is considered an independent central bank because its monetary policy decisions do not need approval from the president or anyone in the executive or legislative branches of government.

The Federal Reserve System consists of 12 Federal Reserve Banks, each operating within its own geographic area or district of the United States. These Reserve Banks act as the operating arms of the Federal Reserve System, carrying out core functions such as supervising and examining banks and other financial institutions, enforcing compliance with federal laws, and lending to depository institutions to ensure liquidity.

Nationally chartered commercial banks in the US are required to hold stock in and can elect some board members of the Federal Reserve Bank in their region. As the banker's bank, the Federal Reserve helps assure the safety and efficiency of the payments system. It also acts as the government's bank, processing financial transactions, issuing US government securities, and handling incoming federal tax deposits and outgoing government payments.

In the context of Target2, a payment system owned and operated by the Eurosystem, banks must consult their National Central Bank to determine their needs and select the appropriate participation scenario. Target2 enables banks to transfer funds between each other quickly and securely, with each bank having its own account within the system.

Canadian Banks: Will They Weather the Storm?

You may want to see also

Explore related products

![]()

TARGET2 is a payment system owned and operated by the Eurosystem

TARGET2 is a centralized platform that enables EU banks to transfer money between each other quickly, securely, and in real-time. It is used by over 1,000 banks across Europe, making it a widely accepted payment system for businesses operating in the region. TARGET2 can be easily integrated with other payment and accounting systems, streamlining the payment process for businesses.

The system works as follows: Bank A and Bank B both have accounts with a central bank. A payment in euros is to be made from Bank A to Bank B. Bank A submits the payment instructions to TARGET2, which debits Bank A's account and credits Bank B's account – settling the payment. TARGET2 then transfers the payment information to Bank B. This process ensures that funds are available to the recipient immediately.

TARGET2 also provides settlement services, allowing banks to balance their accounts and ensuring the system remains stable and efficient. It follows five steps to complete a transaction: initiation, processing, reconciliation, confirmation, and finalisation. TARGET2 was introduced in 2007-2008 and was replaced with T2 in March 2023.

Federal Reserve Bank: Government Agency or Independent Entity?

You may want to see also

Explore related products

![]()

It is the leading European platform for processing large-value payments

TARGET2 is a payment system owned and operated by the Eurosystem. It is used by both central banks and commercial banks to process payments in euros in real-time. More than 1,700 banks use TARGET2 to initiate transactions in euros, either on their own behalf or on behalf of their customers. Taking branches and subsidiaries into account, more than 55,000 banks worldwide can be reached via TARGET2.

TARGET2 is a real-time gross settlement (RTGS) system, enabling EU banks to transfer money between each other immediately. This means that when a bank initiates a transfer, TARGET2 debits the sending bank's account and credits the receiving bank's account in real-time, ensuring the funds are available to the recipient right away. TARGET2 also provides settlement services, allowing banks to balance their accounts and ensuring the system remains stable and efficient.

TARGET2 is a mandatory platform for processing large-value payments involving the Eurosystem. It is also used for the settlement of operations of all large-value net settlement systems and securities settlement systems handling the euro. There is no upper or lower limit on the value of payments that can be processed through TARGET2. This makes TARGET2 one of the largest payment systems in the world in terms of the value processed.

TARGET2 provides a centralized platform for businesses to make and receive payments, simplifying the payment process and reducing the need for multiple banking relationships. It is easily integrated with other payment and accounting systems, streamlining the overall payment process for businesses. TARGET2 also provides high-level security, using advanced measures to protect against fraud and cyber-attacks.

Stock Exchange: Are Banks Listed?

You may want to see also

Explore related products

![]()

TARGET2 is used by over 1,000 banks across Europe

TARGET2 is a payment system owned and operated by the Eurosystem, which consists of the European Central Bank (ECB) and the national central banks of the 20 European Union member states that are part of the Eurozone. It is used by over 1,000 banks across Europe, making it a widely accepted payment system for businesses operating in the region. TARGET2 is a platform where banks can settle payments, facilitating cross-border payments between banks. It is one of the largest payment systems in the world in terms of the value processed.

TARGET2 enables the free flow of money across borders and supports the implementation of the ECB's single monetary policy. It is a key building block of financial integration in the EU, allowing EU banks to transfer money between each other in real time, known as real-time gross settlement (RTGS). This makes TARGET2 especially attractive for businesses and large institutions as it can handle large payments. More than 350,000 transactions are processed daily through TARGET2, amounting to over €1.8 trillion.

TARGET2 is also used by central banks from four non-Eurozone states: Bulgaria, Denmark, Poland, and Romania. In 2012, TARGET2 had 999 direct participants, 3,386 indirect participants, and 13,313 correspondents. Taking into account branches and subsidiaries, more than 55,000 banks worldwide (and all their customers) can be reached via TARGET2.

TARGET2 provides a centralized platform for businesses to make and receive payments, simplifying the payment process and reducing the need for multiple banking relationships. It processes payments in real time, ensuring that funds are transferred quickly and securely between accounts. This is achieved through a single technical platform that establishes business relationships between TARGET2 users and their national central bank.

Incompatible Banks: A Complex Relationship

You may want to see also

Explore related products

![]()

It is a key component of the infrastructure of the Euro

TARGET2 is a payment system that enables banks to transfer money between each other in real time. It is owned and operated by the Eurosystem, which is made up of the European Central Bank (ECB) and the national central banks of the European Union countries that have adopted the euro. TARGET2 is a key component of the infrastructure of the Euro.

TARGET2 is a real-time gross settlement (RTGS) system that facilitates the flow of money across borders and supports the implementation of the ECB's single monetary policy. It is available to central banks within the European System of Central Banks (ESCB) and to other central banks that have entered into an agreement with the ECB. More than 1,000 banks across Europe use TARGET2, making it a widely accepted payment system for businesses in the region.

TARGET2 provides a centralized platform for banks to make and receive payments, simplifying the payment process and reducing the need for multiple banking relationships. It processes payments in real time, ensuring that funds are transferred quickly and securely between accounts. This is especially important for time-sensitive transactions. TARGET2 also provides settlement services, allowing banks to balance their accounts and ensuring the system remains stable and efficient.

TARGET2 is the second-generation RTGS system in the European Union, replacing the first-generation TARGET system in 2007. It has become an essential part of the EU's financial infrastructure, processing more than 350,000 transactions every day, worth over €1.8 trillion. TARGET2 was previously used for transactions involving more than €2.2 trillion per day. It is used by EU central banks and their national communities of commercial banks, and taking into account branches and subsidiaries, more than 55,000 banks worldwide can be reached via TARGET2.

Charging for Services: How Banks Profit from Client Transactions

You may want to see also

Frequently asked questions

TARGET2 is a payment system that allows banks to transfer funds between each other quickly and securely. It is owned and operated by the Eurosystem.

TARGET2 uses a centralised platform to process transactions, with each bank having its own account within the system. When a bank initiates a transfer, TARGET2 debits the sending bank’s account and credits the receiving bank’s account. This process happens in real-time.

TARGET2 is available to central banks within the European System of Central Banks (ESCB) and to other central banks that have entered into an agreement with the ECB. More than 1,000 banks across Europe use TARGET2, making it a widely accepted payment system.

Before your bank subscribes to TARGET2 services, talk to your National Central Bank to determine your needs. Depending on your intended participation in TARGET2, select the appropriate forms to complete.