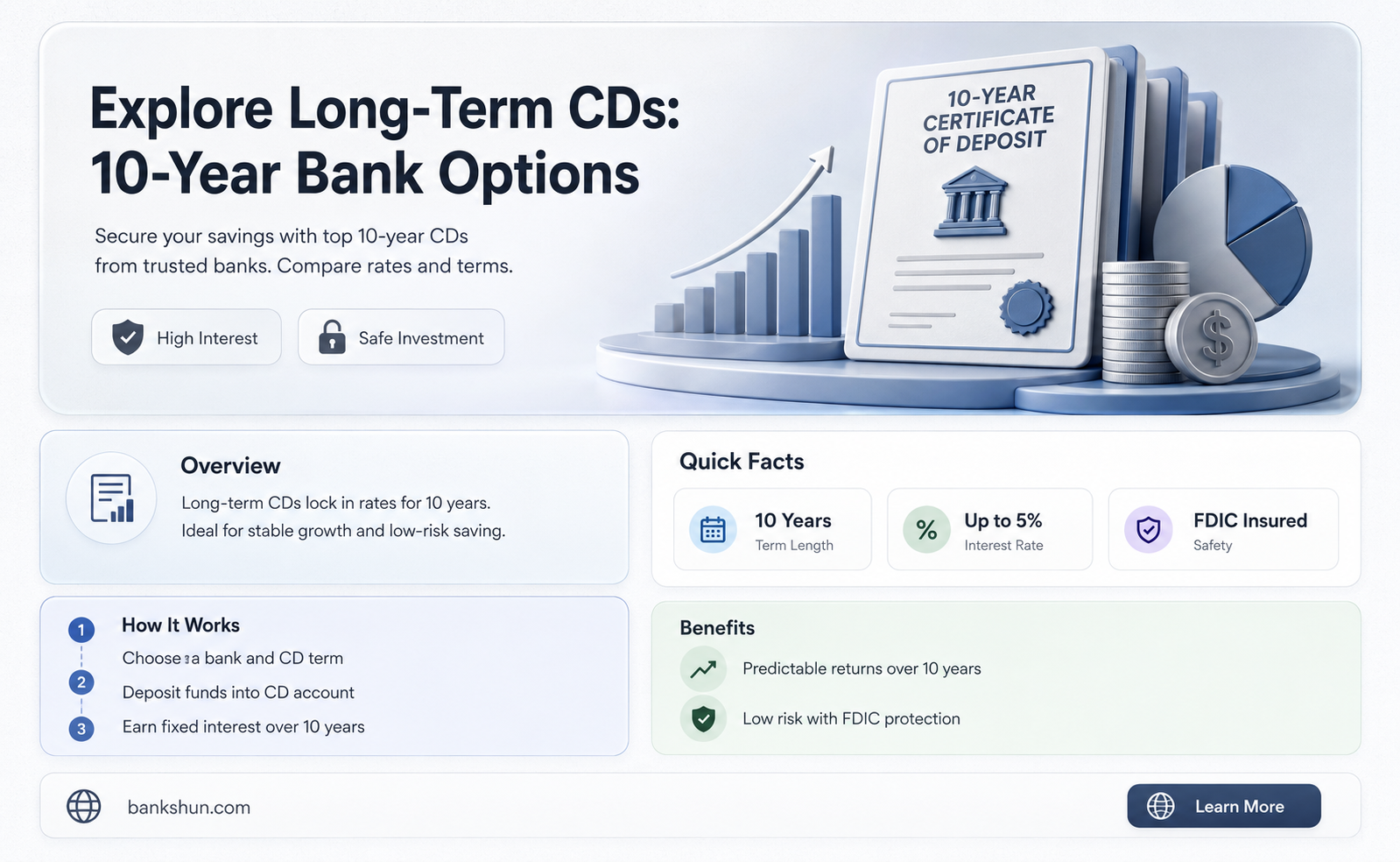

A certificate of deposit (CD) is a type of low-risk savings account that offers a higher interest rate than traditional savings accounts. CDs are generally considered low-risk because they are insured up to $250,000 by the Federal Deposit Insurance Corporation (FDIC). The most common CD terms are three months to five years, but they can be as short as 28 days or as long as 10 years. While few institutions offer 10-year CDs, they are available from banks such as First National Bank of America, EmigrantDirect, MySavingsDirect, and PNC Fixed Rate Certificates of Deposit.

| Characteristics | Values |

|---|---|

| Term | 10 years |

| Interest Rate | Fixed |

| Interest Crediting | Monthly, quarterly, daily |

| Minimum Opening Deposit | $1,000 |

| Maximum Opening Deposit | Up to $250,000 |

| Early Withdrawal | Penalty of 90-180 days' interest |

| Renewal | Automatic |

| FDIC Insurance | Up to $250,000 |

Explore related products

What You'll Learn

![]()

CDs are a low-risk savings account

Banks do offer 10-year certificates of deposit (CDs). CDs are a low-risk savings account option. They are considered safe because they are insured by the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA). This insurance covers up to $250,000 of your savings in the event that the bank fails.

CDs are a good option for those who don't need immediate access to their money. They have a specific maturity period, during which you earn interest at a fixed rate. This rate is typically higher than that of a traditional savings account, although it may not keep up with inflation. If you withdraw your money before the maturity date, you will likely have to pay an early withdrawal penalty.

CDs are a good option for longer-term savings goals, such as saving for a wedding, tuition, or a down payment on a home. They can also be a useful addition to a diversified retirement portfolio. One strategy is to create a CD ladder, where you buy multiple CDs with different maturity dates and interest rates that increase as the maturation dates get longer. This can help protect your money from changing interest rates and allow you to take advantage of the higher rates offered by longer-term CDs.

While CDs are a safe and effective way to save money, there are some drawbacks. One is that your money is locked in for the term of the CD, and withdrawing it early can result in penalties. Additionally, CDs may not offer the same growth potential as stocks and bonds, and you may miss out on higher returns from other investment opportunities. It's important to be aware of what's happening with interest rates in the economy before investing in CDs, as you could miss out on a higher return if your money is locked in at a lower rate.

Birth Certificates: Valid IDs for Banks?

You may want to see also

Explore related products

![]()

CDs offer a higher interest rate than savings accounts

Banks do offer 10-year certificates of deposit (CDs). CDs are a type of savings account that holds your money for a fixed term, ranging from a few months to several years.

CDs typically offer higher interest rates than regular savings accounts, helping your money grow more over time. For example, on May 19, 2025, the average rate for a 12-month CD was 1.75%, more than four times higher than the average savings account rate of 0.42%. The best interest rate a bank could have offered on a CD was 5.37%—the national cap rate at the time.

CDs are considered safe, with FDIC or NCUA insurance protecting funds up to $250,000. They also offer guaranteed returns, as you know exactly how much you'll earn by the end of the term. However, it's important to note that your money is locked in for the term of the CD, and withdrawing it early can result in penalties.

High-yield savings accounts also offer higher interest rates than traditional savings accounts. These accounts are often available at online-only banks, which can offer higher rates due to lower overhead costs compared to brick-and-mortar banks. While the average savings account interest rate in the US was 0.42% APY on June 10, 2025, some banks advertised high-yield savings accounts with APYs upwards of 4.5%.

When deciding between CDs and savings accounts, it's essential to consider your financial goals and needs. CDs offer higher interest rates and guaranteed returns but lack the flexibility of easy access to your funds. On the other hand, high-yield savings accounts provide higher interest rates than traditional savings accounts while maintaining the liquidity and ease of access to your money.

The World Bank's Mission: Eradicate Poverty, Build Prosperity

You may want to see also

Explore related products

![]()

CDs are federally insured

Certificates of deposit (CDs) are considered a safe way to save money because they are federally insured. The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that provides deposit insurance and maintains the safety of the US banking system. FDIC insurance covers deposits up to \$250,000 per person per account ownership type. This means that if a bank fails, customers are guaranteed to receive their money back up to \$250,000.

Most CDs are FDIC-insured, but there are some exceptions. For example, if you invest in foreign banks through your CD account, it may not be covered by FDIC insurance. Similarly, if you purchase a CD account through a non-bank institution such as a brokerage firm, it may not carry FDIC insurance. It is important to evaluate your risk tolerance and the issuing bank's stability when considering an uninsured CD account.

You can check if a bank offers FDIC-insured CDs by looking for the acronym FDIC or NCUA at the bottom of its website. You can also use the FDIC's BankFind tool to look up the status of your financial institution. By confirming that your CD account is FDIC-insured, you can have peace of mind that your savings are protected.

While CDs are federally insured, it is important to note that there may be penalties for early withdrawal. CDs typically have time-based restrictions on accessing your money, and you may face charges and fees if you need to withdraw your funds before the term is up. Therefore, CDs are best suited for longer-term savings goals, while traditional savings accounts or money market accounts are more suitable for short-term goals.

Large Transactions: Banks' Reporting Requirements and Implications

You may want to see also

Explore related products

![]()

CDs have varying terms

Certificates of deposit (CDs) are fixed-income investments that generally pay a set rate of interest over a fixed time period. CDs have varying terms, with the most common being three months to five years, though they can be as short as 28 days or one month, and as long as 10 years.

When choosing a CD, it's important to consider your savings goals and shop around for a product that balances term and rate in a way that fits those goals. For instance, if you need the money soon, a CD with a shorter term or one that offers penalty-free withdrawals may be more suitable. On the other hand, if you're saving for something further down the line, a CD with a longer term may be more beneficial.

Additionally, it's worth considering where interest rates might be headed before investing in CDs. While CDs with longer terms and higher balance requirements tend to pay higher interest rates, this isn't always the case. For example, long-term CDs may offer lower rates than short-term CDs if interest rates are expected to fall. Variable-rate CDs and bump-up CDs are also options if you expect rates to rise, though they typically have lower rates than the best available CDs.

To make your money more accessible, you can also consider a CD ladder strategy, which involves investing in multiple CDs with staggered maturity dates. This allows you to reinvest or use the cash as needed when each CD matures.

Armed Guards: Are They Still Necessary for Banks?

You may want to see also

Explore related products

![]()

CDs have different minimum balance requirements

Banks do offer 10-year certificates of deposit (CDs). CDs are a type of deposit account that is payable at the end of a specified amount of time, known as the term. They generally pay a fixed rate of interest and can offer a higher interest rate than other types of deposit accounts, depending on the market.

The right amount to deposit into a CD depends on your financial situation and goals. CDs generally work best for long-term savings goals, as there are often penalties for early withdrawal. It's important to only lock in funds that you won't need before the term expires to avoid early withdrawal penalties.

When choosing a CD, it's essential to consider the interest rates and terms offered by different financial institutions. Additionally, FDIC insurance protects your money up to $250,000 per depositor, per insured bank, so it's crucial to stay within this limit or diversify your savings across multiple banks or investment types.

Clear Access Banking: Wells Fargo's Simplified Solution

You may want to see also

Frequently asked questions

Yes, some banks offer 10-year CDs.

CD stands for Certificate of Deposit. It is a type of low-risk savings account that can boost the amount you earn in interest in exchange for keeping your money deposited for a set amount of time.

CDs generally offer more competitive interest rates than traditional savings accounts. They are also insured by the federal government for up to $250,000.

If you withdraw your money before the CD matures, you will likely pay an early withdrawal penalty, which can significantly reduce the interest you have earned.

It's important to consider where interest rates might be headed before investing in CDs. If rates are falling or expected to fall, locking in a rate for the long term can be beneficial. If rates are rising or expected to rise, the flexibility of shorter-term CDs may be more beneficial.