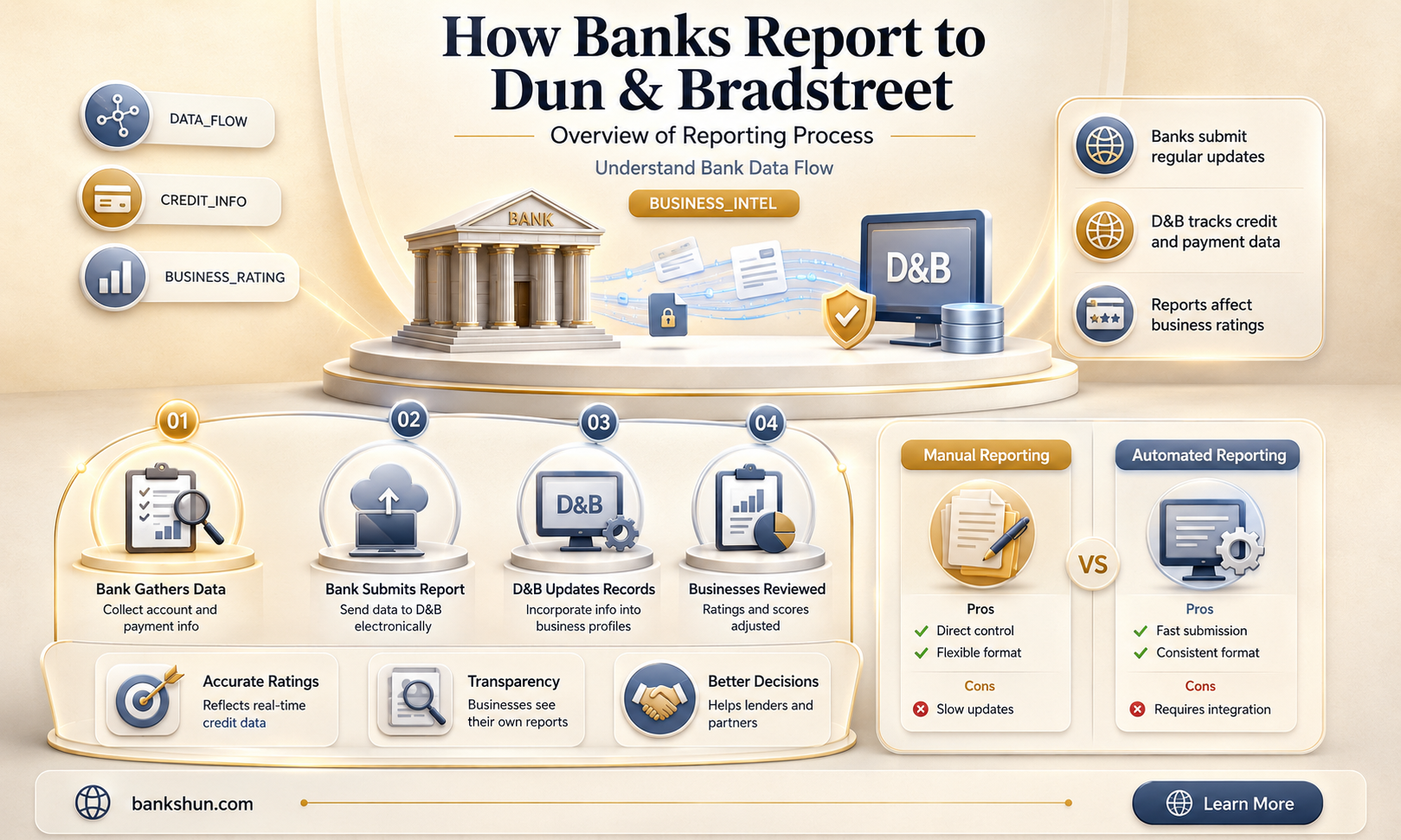

Dun & Bradstreet is one of the largest business credit bureaus, and reporting to it is voluntary. Banks may have different policies and criteria for sharing their customers' credit information. Some banks that report to Dun & Bradstreet include Bank of America, Citibank, and U.S. Bank, among other issuers. When a business credit card issuer reports to Dun & Bradstreet, they share details about the business's trade credit activity, including payment history, outstanding balances, and credit utilization. This information is used to calculate credit ratings and evaluate the risk of conducting business or lending money to a company.

| Characteristics | Values |

|---|---|

| Reporting to Dun & Bradstreet | Voluntary |

| Reporting banks | Bank of America, Citibank, U.S. Bank, Capital One, etc. |

| Information reported | Credit limit, account balance, payment history, account age, public records, etc. |

| Purpose of reporting | Calculating credit ratings, evaluating the risk of conducting business with a company |

Explore related products

What You'll Learn

![]()

Not all banks report to Dun & Bradstreet

If your bank does not report to Dun & Bradstreet, there are still ways to build your business credit profile. You can apply for a business credit card that reports to Dun & Bradstreet, such as cards from Bank of America, Citibank, Capital One, or U.S. Bank. These cards help establish your company's credit and increase your odds of approval for business loans.

Additionally, you can focus on building your Paydex Score with Dun & Bradstreet, which is their popular business credit rating. This can be done by ensuring your vendors report your businesses' accounts as tradelines to business credit bureaus, and by consistently paying on time.

It is important to note that credit reporting policies can change, and information about credit reporting is not always publicly available. Therefore, it is advisable to reach out directly to your lenders and credit card issuers to understand their specific reporting practices.

How Banks Alert You of Suspicious Activity

You may want to see also

Explore related products

![]()

Dun & Bradstreet calculates credit ratings

Dun & Bradstreet (D&B) is a business credit rating agency that calculates credit ratings for businesses. These ratings are used by potential investors, lenders, and suppliers to assess a company's financial health and creditworthiness.

The D&B Rating is a crucial component of a company's business credit profile, which includes various scores and ratings. The rating has two parts: the Rating Classification and the Composite Credit Appraisal. The Rating Classification reflects a company's size based on its worth or equity. Companies with a net worth of $50 million or more receive a 5A rating, while those with a net worth under $5,000 are labelled HH.

The Composite Credit Appraisal is a number from 1 to 4 that indicates a company's overall creditworthiness, with 1 being the most creditworthy. This score is based on information collected by D&B, including payment histories, financial data, public records, years in operation, and other factors.

D&B calculates credit ratings based on information provided by businesses, lenders, and suppliers. This includes payment information, financial statements, and public records related to regulatory requirements and business tax reports. Additionally, D&B considers a company's track record of on-time payments, business structure, and the likelihood of defaulting on loans and credit.

Businesses can impact their D&B ratings by ensuring timely bill payments, maintaining up-to-date company information, and uploading financial reports to their credit files. Suppliers can also submit paid invoices as trade references, which can positively affect a company's creditworthiness assessment.

While not all banks report account activity to D&B, major credit card companies like Capital One, Bank of America, Citibank, and U.S. Bank do. This information helps D&B calculate credit ratings and assess the risk associated with lending to a particular company.

How Banks Verify Employment: Calling Your Employer?

You may want to see also

Explore related products

![]()

Business credit cards that report to Dun & Bradstreet

It is important to note that reporting to Dun & Bradstreet is voluntary, and banks may have different policies and criteria for sharing their customers' credit information. If your bank does not report to Dun & Bradstreet, you can still build your business credit profile by using a credit card that reports to other business credit bureaus, such as Experian Business or Equifax Business.

- Capital One reports activity about its Spark business credit cards to Dun & Bradstreet, Experian, and the SBFE.

- Bank of America reports activity about its business credit cards to the SBFE. This information may then be available to lenders and other businesses that purchase credit reports from Dun & Bradstreet.

- American Express reports activity about its business credit cards, including the Amazon Business Prime American Express Card, to the SBFE. This information may also be available to Dun & Bradstreet through its commercial credit bureau partners.

- Chase reportedly provides information about its business credit cards, such as Ink Business cards and co-branded cards like the United Business Credit Cards, to Dun & Bradstreet and other business credit bureaus.

- Citibank and U.S. Bank also offer business credit cards that report to Dun & Bradstreet.

In addition to the above, the Nav Prime Card is a business credit-building Visa charge card that submits tradelines to all major business credit bureaus, including Dun & Bradstreet.

It is always a good idea to contact the issuing bank or company directly to inquire about their credit reporting practices before applying for a business credit card.

Why Central Banks Are Buying Gold

You may want to see also

Explore related products

![]()

Trade credit accounts and Paydex scores

Trade credit accounts are a type of credit account where a company can buy goods or services and pay for them at a later date, typically within 30 days of the invoice date. These accounts are important for building a Paydex score, a business credit score reported by Dun & Bradstreet (D&B) that tracks how often a business pays its vendors and suppliers on time.

The Paydex score, ranging from 0 to 100, is a rating of how reliably a business pays certain monitored accounts. A score of 80 or above indicates that a business consistently pays its bills on time or ahead of schedule and is considered low-risk and highly creditworthy. Scores below 50 indicate a serious risk of default.

To establish a Paydex score, a business needs a minimum of two tradelines (accounts with suppliers or vendors) and three or more credit experiences. Not all vendors and suppliers automatically report payment history to D&B, so businesses must ensure that minimum reporting requirements are met. Vendors that offer trade credit and report to business credit bureaus include Net 30 vendors, which give businesses 30 days from the invoice date to pay for purchases.

Businesses can ask their suppliers to report to D&B if they don't already, and increasing the number of on-time or early payments reported can help improve the Paydex score. Opening additional tradeline accounts can also help build a stronger score, as long as payments are made on time.

While not all banks report account activity to Dun & Bradstreet, major credit card companies like Capital One, Bank of America, Citibank, and U.S. Bank do. This information is used to calculate credit ratings and evaluate the risk of doing business with or lending money to a company.

Monthly Fees: Are US Banks Charging Customers?

You may want to see also

Explore related products

![]()

Lenders can purchase credit reports

When it comes to business credit, lenders can purchase credit reports from Dun & Bradstreet, which uses information from credit card companies to calculate credit ratings. While reporting to Dun & Bradstreet is voluntary, major credit card companies like Bank of America, Citibank, U.S. Bank, and Capital One regularly report account activity. This information helps lenders evaluate the risk of conducting business or lending money to a company.

Credit reports are essential for lenders to make informed decisions about loan applications. Lenders typically request credit reports from one or more of the three major credit bureaus: Equifax, Experian, and TransUnion. These reports help lenders assess the borrower's credit management skills, identify potential red flags, and determine the likelihood of repayment. Lenders may also use credit reports to establish the borrower's FICO score, which is a widely used credit scoring model.

It is important to note that credit reports may vary among credit bureaus, as not all creditors report information to all three bureaus. Therefore, individuals and businesses should be mindful of which credit report a lender might use and consider requesting reports from multiple bureaus. Additionally, while credit reports provide valuable financial insights, they typically do not include credit scores, which may require separate inquiries to the credit bureaus.

In summary, lenders can purchase credit reports to assess a borrower's creditworthiness and make informed lending decisions. These reports offer a comprehensive view of an individual's or business's financial history and repayment behaviour, enabling lenders to evaluate the risk associated with extending credit. By understanding the information contained in credit reports, lenders can make more informed decisions about loan applications and establish the terms and conditions of the loan, including interest rates and collateral requirements.

Coin Deposits During COVID-19: Are Banks Accepting?

You may want to see also

Frequently asked questions

Not all banks report account activity to Dun & Bradstreet, but most major credit card companies do. Reporting to Dun & Bradstreet is voluntary, and banks may have different policies and criteria for sharing their customers' credit information.

When a business credit card issuer reports to Dun & Bradstreet, they share details about the business's trade credit activity. This includes payment history with vendors, outstanding balances, credit utilization, account age, and any public records such as bankruptcies.

Some banks that report to Dun & Bradstreet include Bank of America, Citibank, Capital One, and U.S. Bank.