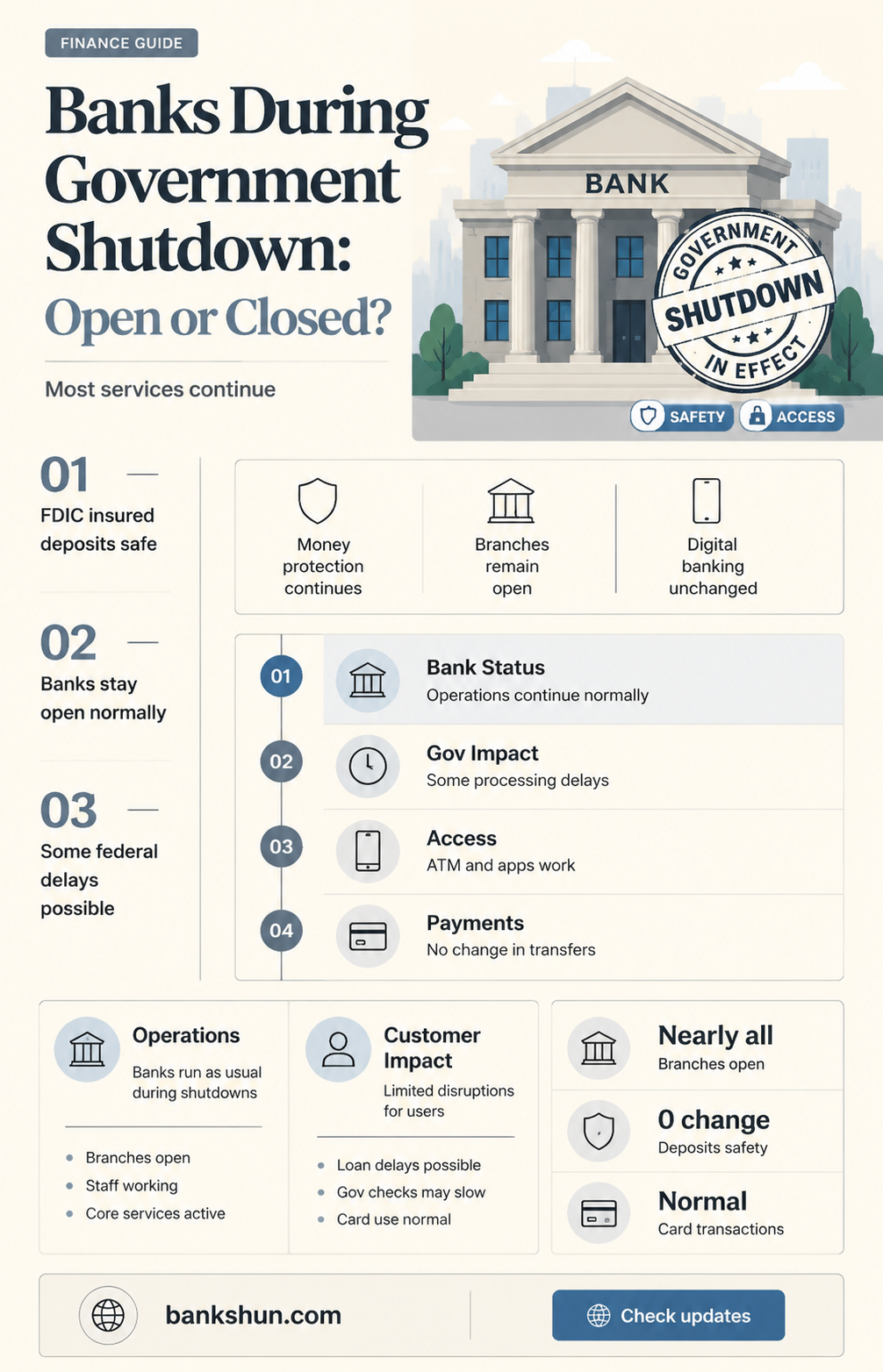

During a government shutdown, banks remain open, but the impact on the economy and banks can vary. While major bank regulatory agencies like the Federal Reserve and the FDIC remain operational and funded, the shutdown of other government agencies can affect the financial stability of consumers and small businesses. This may lead to a decrease in consumer spending and an increase in short-term loans for furloughed federal workers. Additionally, there may be delays in loan processing and challenges in resolving issues related to student loans. The impact of a government shutdown on banks highlights the importance of effective financial regulation and the need for a robust response from financial institutions to support those affected.

| Characteristics | Values |

|---|---|

| Do banks shut down during a government shutdown? | No, banks remain open during a government shutdown. |

| Do bank regulators shut down during a government shutdown? | No, major bank regulatory agencies remain funded and operational during a government shutdown. Examples include the Federal Reserve, FDIC, and Office of the Comptroller of the Currency (OCC). |

| How does a government shutdown impact the economy? | A government shutdown can slow down the economy as federal workers reduce their spending. Consumers may also become anxious and save more rather than spend during periods of uncertainty. |

| How does a government shutdown affect individuals? | Individuals may experience delays or difficulties in processing certain types of loans, such as student loans or mortgages. Social Security payments generally continue during a shutdown, but other programs like SNAP (Supplemental Nutritional Assistance Program) and WIC may be vulnerable to funding shortfalls. |

Explore related products

What You'll Learn

![]()

Banks remain open during government shutdowns

During a government shutdown, consumers tend to become anxious and save rather than spend, which slows the economy. This can particularly impact institutions that rely on retail banking or credit cards. With federal workers furloughed or not being paid, banks may also be affected by customers' inability to make payments on debts like mortgages, student loans, car loans, business loans, or credit cards. Banks are encouraged to consider prudent efforts to modify terms on existing loans or extend new credit to help affected borrowers.

The government shutdown can also affect the availability of certain loans and grants. The Small Business Administration, for example, would shut down, and the Small Dollar Loan Program, which helps people in low-income communities avoid payday lenders, would experience funding delays. Similarly, the review of grant applications and the awarding of grant funds by the Department of Education would come to a halt.

While banks remain open, a government shutdown can cause a slowdown in the economy and impact the availability of certain financial services and assistance.

Banks as Personal Representatives: When and Why?

You may want to see also

Explore related products

![]()

Bank regulatory agencies remain funded

During a government shutdown, major bank regulatory agencies remain funded and operational. This is because they are not dependent on Congressional funding (aka appropriations). Instead, they fund themselves through various means, often correlated to their core activities and sometimes funded directly or indirectly through the financial institutions they regulate. For example, the Federal Reserve, FDIC, and Office of the Comptroller of Currency (OCC) remain on the job, protecting depositors and performing the key role of the central bank.

The Federal Reserve would also provide dollars to banks as quickly as it could print them, helping to prevent a nationwide bank run. This is important because, in a fractional banking system, only a fraction of deposits are kept on hand, with the rest loaned out. If enough people believe that their bank will run out of money, a bank run will result, even with FDIC insurance.

While bank regulatory agencies remain funded, other government services are affected. For example, the Small Business Administration shuts down during a government shutdown, and the IRS and tax collections are likely to reduce staff. Additionally, government employees, including the military, are not paid during a shutdown, which can lead to increased reliance on credit cards and short-term loans.

The impact of a government shutdown on the economy and banks can be significant. Consumers tend to get anxious and save rather than spend during periods of uncertainty, slowing the economy and affecting institutions that rely on retail banking or credit cards. There may also be delays in loan processing and forgiveness, and it may be more difficult to resolve issues related to student loans and other types of loans.

Bank Reserves: Are They Considered Assets?

You may want to see also

Explore related products

![]()

Financial markets stay open

During a government shutdown, financial markets remain open, and banks continue to operate. However, the stability of the financial system relies on regulators, some of which may not be operational during a shutdown.

The Securities and Exchange Commission (SEC) and the Commodities Futures Trading Commission (CFTC) are two critical watchdogs of the financial markets that shut down when the government does. This leaves the financial system vulnerable to potential risks and crises. On the other hand, bank regulators like the Federal Reserve, FDIC, and Office of the Comptroller of the Currency (OCC) remain operational and continue to protect depositors. These regulators are not dependent on Congressional funding and, therefore, can continue their work even during a government shutdown.

The impact of a government shutdown on the economy and financial markets is complex. While markets remain open, consumer sentiment tends to be affected, with individuals becoming anxious and opting to save rather than spend. This shift in behaviour can slow down the economy, particularly impacting institutions that rely on retail banking or credit cards. Additionally, with federal workers furloughed or not spending as much, there is a further reduction in economic activity.

The stability of the financial system during a government shutdown is maintained by the active efforts of bank regulators. These regulators encourage financial institutions to support affected consumers and small businesses. This includes recommending prudent workout arrangements, such as modifying terms on existing loans or extending new credit to help borrowers facing temporary hardships.

While financial markets staying open during a government shutdown ensures continuity, it also highlights the regulatory gaps that can increase systemic risk. The closure of key financial market regulators during a shutdown underscores the need for a robust regulatory structure that can safeguard the financial system even during periods of governmental disruption.

Bank Workers: Can They Show Account Balances?

You may want to see also

Explore related products

![]()

Consumers tend to save rather than spend

During a government shutdown, banks remain open, but consumers tend to save rather than spend. This is because consumers get anxious during periods of uncertainty, such as when the government is shut down. As a result, they tend to reduce their spending and save more. This slowdown in consumer spending can have a ripple effect on the economy, particularly on institutions that rely heavily on retail banking and credit card usage.

When consumers become anxious and save instead of spend, it can lead to a decrease in economic activity. Retailers may experience lower sales, and businesses may see a decline in revenue. This can have a knock-on effect on the businesses' ability to maintain operations and pay their employees, potentially leading to layoffs or reduced working hours. Furthermore, a decrease in consumer spending can also impact tax revenues for the government, which can further exacerbate the economic slowdown.

During a government shutdown, federal workers may be furloughed or temporarily laid off. This loss of income can cause financial strain, especially for those who rely primarily on their government jobs. As a result, affected individuals may have difficulty making payments on debts such as mortgages, student loans, car loans, business loans, or credit card bills. Financial institutions are encouraged to work with these individuals and offer assistance, such as modifying loan terms or providing forbearance on credit card and mortgage debt.

Additionally, a government shutdown can disrupt the flow of credit in the economy. With consumers saving more and spending less, banks may experience a decrease in deposits. This can impact the banks' ability to lend, as they may have less funds available to loan out. A reduction in lending can affect both businesses and individuals, making it more challenging to obtain the credit necessary for investments, expansions, or major purchases.

Moreover, a government shutdown can also impact consumer sentiment and confidence. Consumers may become more cautious and pessimistic about the economy, further reducing their spending. This can create a self-reinforcing cycle, as decreased consumer spending can lead to slower economic growth, reinforcing consumers' negative sentiments. It is essential for policymakers to recognize this dynamic and take appropriate actions to minimize the impact of a government shutdown on consumers and the economy.

Electronic Payments: A Core Feature of Digital Banking

You may want to see also

Explore related products

![]()

Borrowers may face difficulties with payments

Banks remain open during a government shutdown, but borrowers may face difficulties in making payments. The federal government continues to make Social Security payments, and Medicare and Medicaid programs are protected from federal funding shortfalls. However, the government may temporarily lay off employees, and those who are furloughed will have to rely on short-term loans to make ends meet. With fewer federal employees, there could be delays in loan processing and forgiveness, and it may be more difficult to resolve issues related to student loans.

The Small Business Administration, which provides disaster relief, would shut down, and the Small Dollar Loan Program, which helps people in low-income communities avoid payday lenders, would have funding delayed. The shutdown may also affect flood insurance, as the National Flood Insurance Program (NFIP) would be unable to issue new policies or allow property owners to renew their existing policies. This could cause property buyers to lose financing or be forced to pay fees to hold interest rates.

Financial regulators encourage institutions to consider modifying the terms of existing loans or extending new credit to help affected borrowers. Borrowers facing financial strain are encouraged to contact their lenders immediately. Institutions that rely on retail banking or credit cards could struggle during a government shutdown as consumers tend to save rather than spend during periods of uncertainty. Banks will be under pressure to offer forbearance on credit card and mortgage debt.

A government shutdown could also lead to a wider economic slowdown. With federal workers furloughed, there will be less spending in the economy. The government will also stop purchasing goods and services, impacting businesses. The shutdown of regulatory bodies such as the Securities and Exchange Commission (SEC) and the Commodities Futures Trading Commission (CFTC) could further increase the risk of a financial crisis.

Bank Security: 24/7 Guard Presence for Ultimate Protection

You may want to see also

Frequently asked questions

No, banks remain open during a government shutdown. However, there may be knock-on effects on the economy and banks.

Yes, major bank regulatory agencies like the Federal Reserve, FDIC, and OCC remain funded and operational during a government shutdown as they are not dependent on Congressional funding.

Your money in the bank is generally safe during a government shutdown. However, there may be some impact on your investments depending on the length of the shutdown. Additionally, there could be delays in loan processing and forgiveness, and it may be more challenging to resolve related issues.