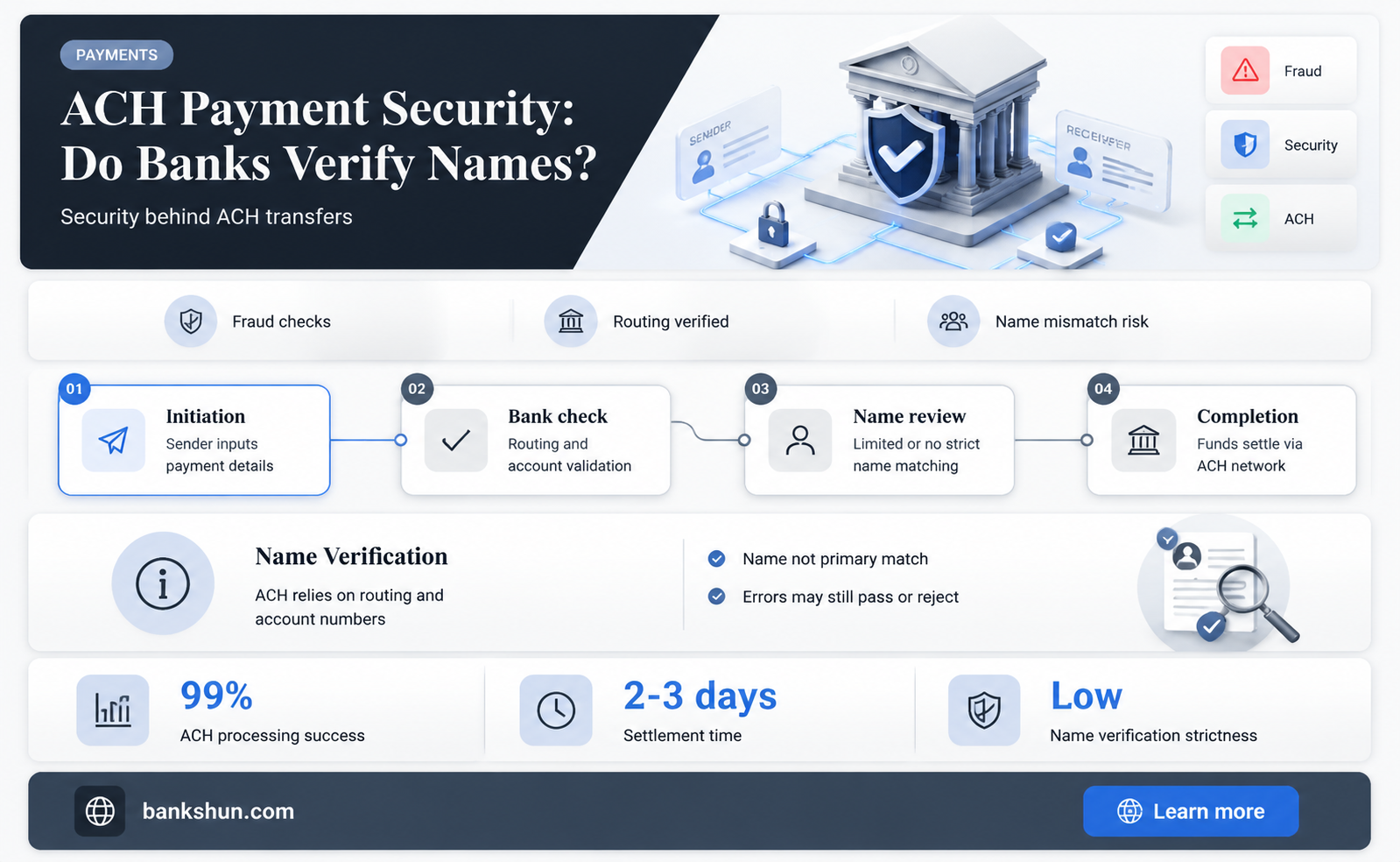

ACH, or Automated Clearing House, is a secure network that facilitates electronic money transfers between banks. It is a convenient and typically free method of transferring money, used by 92% of American workers to receive their payroll. However, it is important to understand the risks associated with ACH transfers. While the sender typically requires the recipient's bank account and routing number, account type, and name, the name is not always verified, leaving room for fraud. Banks can be held liable for fraud if they fail to detect and stop suspicious activity due to a lack of proper monitoring systems. To prevent fraud, banks can implement tools to analyze patterns and enhance verification processes.

| Characteristics | Values |

|---|---|

| Name verification | Not always required; the account and routing number are the most important |

| Name mismatch | ACH payments can go through with a different name as long as the account and routing numbers match |

| Fraud detection | Banks can use tools to analyze patterns that may indicate fraud, such as frequent cross-bank transfers of round sums |

| Fraud prevention | Random audits, customer verification, relationship monitoring, and bank collaboration |

| ACH kiting | A scheme where fraudulent actors transfer funds between accounts they control at different banks to inflate the balance before transactions clear |

Explore related products

What You'll Learn

![]()

The importance of name matching in ACH transfers

In terms of technical requirements, the "Name" field is typically included in ACH transactions. However, it is not always strictly enforced, and some transfers may go through even with a name mismatch. This flexibility is intentional, allowing financial institutions to make decisions based on their own risk assessment and fraud prevention practices.

Additionally, name matching is crucial for ensuring accurate payments and preventing errors. While ACH transfers are generally secure and low-cost, they can be prone to unauthorized or mistaken transactions. By matching names accurately, banks can reduce the risk of sending payments to the wrong accounts, protecting sensitive personal information, and safeguarding customers' funds.

To enhance security, banks can implement enhanced verification procedures, such as spot audits, customer verification, and relationship monitoring. These measures help detect and prevent fraud by scrutinizing transactions, verifying customer information, and identifying potential red flags. Therefore, while name matching may not always be a determining factor in ACH transfers, it remains an essential component of the overall security and accuracy of the payment system.

Alissa and FaZe Banks: Relationship Status Update

You may want to see also

Explore related products

![]()

The role of banks in ACH fraud prevention

The ACH, or Automated Clearing House, is a financial transaction network that facilitates electronic fund transfers (EFTs) in the US. It is a convenient way to transfer money, but it has also become a common target for fraud. ACH fraud occurs when a bad actor gains access to an individual's or company's bank account information and initiates a fraudulent transfer. This can happen through phishing scams, insider threats, or other means. As such, financial institutions play a crucial role in safeguarding account holders from the perils of ACH fraud.

One way banks can prevent ACH fraud is by using advanced technologies such as machine learning and transaction monitoring to detect suspicious activity. For example, tools like Plaid Signal can create transaction risk assessment scores to predict the likelihood of an ACH payment being returned and help companies limit their risk. Other tools like Plaid IDV can quickly verify identity information by comparing it to regulated data sources and global ID documents, ensuring that a real person is submitting the information. Banks can also use secure APIs to protect their customers' financial information.

In addition to advanced technologies, banks can also employ simpler methods to prevent ACH fraud. For instance, they can require customers to manually review and approve transactions before they are completed. Banks can also train their employees to recognize common phishing scams and their warning signs, such as overly urgent-sounding emails. By raising awareness of these scams, banks can encourage employees and customers to be more skeptical of suspicious emails and to verify sending addresses and URLs.

Finally, banks can protect their customers by compensating them for fraudulent ACH transactions. According to Federal Reserve Regulation E and the National ACH Association (NACHA), banks are liable for ACH fraud and must reimburse consumers for unauthorized transfers, as long as the fraud is reported within 60 days of the bank providing a statement showing the transaction. By following these regulations, banks can help to minimize the financial impact of ACH fraud on their customers.

Which Banks Offer 90% LTV Mortgages?

You may want to see also

Explore related products

![]()

Customer verification processes for ACH payments

ACH verification confirms that a bank account is legitimate, active, and authorized for transactions before initiating an ACH transfer. This step ensures that funds are sent to or withdrawn from the correct account. The ability to offer multiple verification options can improve customer satisfaction.

One of the most common methods to verify bank account information is to use micro-deposits. This involves sending a couple of small deposits (usually less than a dollar each) to a customer's bank account. The customer then provides the exact amounts of the micro-deposits, and if they match, the account is verified. This process can take a couple of business days.

Another option is to use third-party software, such as Plaid, which can instantly verify a customer's account by having them enter their login credentials. Third-party verification can also check for insufficient funds and future account balances, which micro-deposits cannot do.

Online internet banking verification is another method where customers can instantly verify their accounts by signing into their bank online and selecting the account. This option provides immediate access to process scheduled payments.

Jos. A. Bank Shirts: Are They Worth the Hype for Men?

You may want to see also

Explore related products

![]()

How ACH transfers work

ACH transfers are a secure, reliable, and affordable way to send and receive money between bank accounts. They are ideal for payroll, bill payments, and even peer-to-peer (P2P) payments.

The two main types of ACH transfers are credits and debits. With an ACH credit, you receive money, and with an ACH debit, you send money. To receive money via ACH credit, you need to provide the sender with your bank details, including your bank name, routing number, and account number. Sometimes, senders may ask for a void check to verify your account information. Once the ACH payment is sent and processed, it will show up in your account, and you can see who sent the money and the amount on your transactions list or statement.

For example, when you start a new job, you provide your employer with your banking information. Before each payday, your employer sends that information, along with the amount you are owed and your pay date, to its bank. Your employer is the "Originator", and its bank is the "ODFI" (Originating Depository Financial Institution). The ODFI receives payment files from many employers and then sends them to an ACH Operator. The ACH Operator sorts all the transactions, ensuring each goes to the correct place. In this case, the ACH Operator sends a file to your bank or credit union, instructing it to credit the funds to your account on payday. Your bank or credit union is the "RDFI" (Receiving Depository Financial Institution). The RDFI places the money in your account, making you the "Receiver".

ACH debits work in a similar way, but the process is initiated by the recipient of the funds. For example, if you pay your electric bill through a monthly standing authorization, the utility company will follow your instructions and become the "Originator" because they are originating an ACH payment instruction. The utility company sends your payment instructions, along with payment instructions from other customers, in the form of an ACH file to its bank, the "ODFI". The ODFI combines the payment instructions and sends the combined ACH file to an ACH Operator, which sorts all the payment instructions so that each one gets sent to the correct destination. The ACH Operator then sends the payment instructions to your bank or credit union account, the "RDFI", which withdraws the funds from your account to pay the bill, making you the "Receiver".

ACH transfers are usually quick, with same-day transfers often taking just a few hours. They are also safe and follow the latest in financial technology requirements. However, there is a risk of fraud, with criminals impersonating legitimate businesses and convincing victims to send ACH payments.

Masks at Citizens Bank Park: What's the Policy?

You may want to see also

Explore related products

![]()

The limitations of ACH transfers

While ACH transfers are a secure, reliable, and affordable way to send and receive money between bank accounts, they do come with certain limitations.

Firstly, there are transfer limits on ACH transactions. The maximum ACH transfer limit varies depending on the financial institution, the ACH platform, and the nature of the transaction. For example, ACH direct deposits often have higher limits than direct payments. Same-day ACH payments have a $1 million limit, although individual banks may have lower limits. Citibank’s limits, for instance, are up to $25,000 to send and $100,000 to receive. Financial institutions set these limits to mitigate risk, ensure regulatory compliance, and manage their own operational capabilities.

Secondly, ACH transfers can be slow to process. While same-day ACH transfers are usually processed in a few hours, standard ACH payments can take one to two business days.

Thirdly, ACH transfers can be reversed. Unlike wire transfers, unauthorized, mistaken, or fraudulent transfers can be reversed. This means that there is a risk of funds not being available to the recipient in cases of disputed transactions.

Finally, there may be a risk of incorrect transfers due to name mismatches. While the "Name" field is required in the actual ACH transactions, some banks may not flag transfers with incorrect names as long as the account and routing numbers match. This could potentially lead to funds being transferred to the wrong account if the account number is correct but the name is not. However, this risk may be mitigated by the fact that senders often ask for additional verification methods, such as a void check, to confirm the recipient's account information.

Banking Secrets: Government Access to Your Money

You may want to see also

Frequently asked questions

Banks generally do not verify names on ACH payments as long as the account number and routing number are correct. However, some banks may review the name if the spelling is significantly different or if the transaction is flagged for review.

To receive an ACH payment, you need to provide the sender with your bank name, routing number, and account number. To send an ACH payment, you need the recipient's bank account and routing number, account type, and whether it is an individual or business account.

Yes, unauthorized, mistaken, or fraudulent ACH transfers can typically be reversed, which is a benefit for consumers but increases risk for businesses that accept ACH payments.

Businesses can implement measures such as spot audits, ACH return analysis, customer verification, relationship monitoring, and bank collaboration to detect and prevent ACH fraud.