An amortization schedule is a table that outlines how a loan is paid down over time, including the proportion of each payment that is made up of interest versus principal. When a loan is extended, banks or other financial institutions provide borrowers with amortization schedules to help them understand the repayment structure. While amortization schedules are commonly used for loans, they are also used by businesses to expense intangible assets over their useful life and to account for the declining value of intangible assets. The specific formulas used to calculate amortization schedules may vary across different banks, but the underlying concept of amortization remains consistent.

Explore related products

What You'll Learn

![]()

Loan amortization schedules vs. loan terms

Loan amortization schedules and loan terms are two related but distinct concepts. Loan amortization refers to the schedule or structure of payments over the life of the loan. On the other hand, the loan term is the duration of the loan, or the period before the loan is due for repayment in full.

A loan amortization schedule outlines how a loan is paid down over time. It details the total number of payments and how much of each payment goes towards the principal loan amount and how much is attributed to interest. The proportion of interest versus principal changes over time, with a higher percentage of each payment going towards interest at the start of the loan term when the loan balance is highest. As the principal amount decreases, the interest portion of each payment also reduces.

Amortization schedules are provided by banks or other financial institutions to borrowers when credit is extended. They are typically used for fixed-rate loans and are less common for adjustable-rate mortgages, variable-rate loans, or lines of credit. The schedules are a powerful tool for budgeting, as they allow borrowers to know exactly how much they will owe each month.

Loan terms refer to the duration of the loan, which can vary depending on the type of loan and the agreement between the borrower and lender. Common loan terms include 15 years, 30 years, or another agreed-upon timeframe. At the end of the loan term, the remaining balance must be paid off or refinanced.

In summary, loan amortization schedules detail the structure of payments over the life of the loan, while loan terms refer to the duration of the loan before it is due for repayment. Both concepts are important for borrowers to understand when taking out a loan or mortgage.

Federal Reserve Banks: Open or Closed?

You may want to see also

Explore related products

![Monthly Interest Amortization Tables: Interest Rates of 2% to 25.75%, Loan Amounts of 50 to 300,000, Terms Up to 40 Years?? [MONTHLY INTEREST AMORTIZATION] [Paperback]](https://m.media-amazon.com/images/I/518sN3Bf1jL._AC_UY218_.jpg)

![]()

Amortization schedules for intangible assets

Amortization is an accounting technique used to periodically lower the book value of a loan or intangible asset over a set period of time. It is a process of allocating the cost of an intangible asset over its useful life. Intangible assets are non-physical assets that generate value for a company for over 12 months, such as patents, trademarks, and copyrights.

Businesses use amortization schedules to account for the declining value of intangible assets. This is done to understand their earnings better, comply with accounting standards, and sometimes reduce taxable income. The straight-line method is often used to allocate the cost of an intangible asset evenly over its expected useful life. For example, a $10,000 patent with a lifespan of 10 years would be amortized at $1,000 per year.

Amortization schedules are also used for loans, outlining how a loan is paid down over time. It details the total number of payments and the proportion of each that goes towards interest and principal. The interest you are charged during a given period is based only on the principal at the start of that period. Amortization schedules are provided by banks or financial institutions to borrowers when credit is extended, so borrowers understand the repayment structure.

It is important to note that amortization schedules for intangible assets and loans are different concepts, with distinct applications in accounting and finance.

Federal Regional Banks: How Many Are There?

You may want to see also

Explore related products

![]()

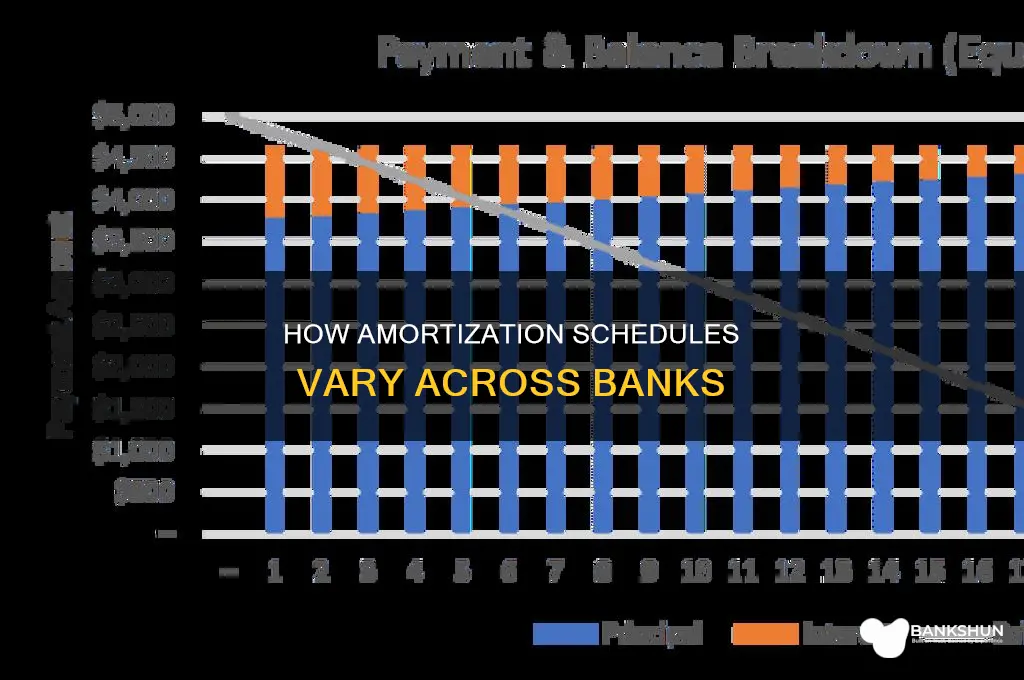

Amortization schedules for different loan types

Amortization is an accounting technique used to periodically lower the book value of a loan or intangible asset over a set period of time. An amortization schedule is a table that details each periodic payment on an amortizing loan. It outlines how a loan is paid down over time, showing the total number of payments and the proportion of each that goes towards the principal versus interest.

Amortization schedules are provided to borrowers by banks or other financial institutions when credit is extended so that borrowers understand the repayment structure. They are most commonly used in the context of loans, but businesses also use them to account for the declining value of intangible assets, such as patents, trademarks, and goodwill.

The details typically included in an amortization schedule are the original loan amount, the loan balance at each payment, the interest rate, the amortization period, the total payment amount, and the proportion of each payment made up of interest versus principal. It's important to note that amortization schedules generally do not consider fees and only work for fixed-rate loans, not adjustable-rate mortgages, variable-rate loans, or lines of credit.

While amortization schedules can be used for various loan types, the specific formula used to calculate the schedule may vary depending on the loan's structure. For example, a loan may be structured as an equal amortizing loan or an equal payment loan (also known as blended payments). In an equal amortizing loan, the principal portion of the loan payment reduces the total loan amount outstanding, while the interest portion does not. As the principal decreases, the interest portion becomes progressively smaller, and a larger portion of each payment goes towards reducing the principal balance. This is commonly seen in mortgage loans, where the borrower makes fixed payments over the loan term, with a larger portion of the early payments going towards interest, and a larger portion of the later payments going towards the principal.

How HECS Debt Affects Your Home Loan Application

You may want to see also

![]()

Calculating amortization schedules

Amortization is the process of paying off a loan or debt over time in equal instalments. Each repayment for an amortized loan will contain both an interest payment and a payment towards the principal balance, which varies for each pay period. An amortization schedule is a table that outlines the total number of payments and the proportion of each that goes towards interest versus principal. It helps borrowers understand the repayment structure of their loan.

To calculate an amortization schedule, you need to know the loan amount, loan term, interest rate, and loan start date. The interest rate should be divided by 12 to get the monthly interest rate, and the number of years in the loan term should be multiplied by 12 to get the total number of payments.

For example, a four-year car loan with a 3% annual interest rate would have 48 payments (4 x 12) and a monthly interest rate of 0.25% (3% / 12). Each repayment will consist of a portion that goes towards the interest and a portion that goes towards the principal. At the start of the loan term, when the loan balance is highest, a higher percentage of each payment goes towards interest. Over time, as the loan balance decreases, the interest portion shrinks, and more of each payment goes towards the principal.

Amortization schedules can be changed by recasting a mortgage, which involves paying a lump sum towards the current loan, or by prepaying with biweekly payments, one additional payment per year, or whenever extra funds are available.

Bank Security: 24/7 Guard Presence for Ultimate Protection

You may want to see also

![]()

Changing amortization schedules

There are several ways to change an amortization schedule:

Refinancing the loan

Refinancing a loan to a longer term will lower the monthly payments, providing more time to pay off the loan. However, this also increases the total cost of the loan as it results in paying more interest over time. Refinancing to a shorter-term loan will result in higher monthly payments but can lead to paying off the loan sooner and saving on interest.

Loan modification

Loan modification involves negotiating with the lender to change the terms of the existing loan. This could include lowering the interest rate or extending the loan term, which can provide some financial relief. However, lenders are not obligated to accept requests for loan modifications.

Biweekly payments

Switching to biweekly payments means paying half the monthly payment amount every two weeks. Over a year, this results in making 26 half-monthly payments, equivalent to 13 monthly payments instead of 12. This method can help pay off the loan sooner and save on interest. However, some lenders may charge a prepayment penalty for early repayment.

Recasting the mortgage

Recasting or prepaying the mortgage involves making a lump-sum payment towards the current loan. This can be done through biweekly payments or whenever extra funds are available. This method can help reduce the loan principal and the overall interest paid over time.

It is important to carefully consider the benefits and drawbacks of changing an amortization schedule, as it can impact the total cost of the loan and the length of the repayment period. Additionally, it is crucial to review the terms and conditions of the loan, including any prepayment penalties or other fees associated with changing the repayment schedule.

Coin Counting at US Bank: What Are Your Options?

You may want to see also

Frequently asked questions

An amortization schedule is a table that outlines how a loan is paid down over time. It includes information such as the total number of payments, the payment amount, and the proportion of each payment that goes towards the principal and interest.

Yes, different banks may have different amortization schedules depending on the specific loan terms and conditions offered. It's always a good idea to review the amortization schedule provided by your bank or financial institution to understand the repayment structure of your loan.

To calculate an amortization schedule, you need to know the loan amount, loan term or length, interest rate, and loan start date. You can use online calculators or create your own amortization table to determine how much you will pay towards the principal and interest over time.

Yes, it is possible to change your amortization schedule by recasting your mortgage or making prepayments. Recasting involves paying a lump sum towards your loan, while prepayments can be made biweekly, annually, or whenever you have extra funds. These options can help you repay your loan faster or reduce the total interest paid over time.