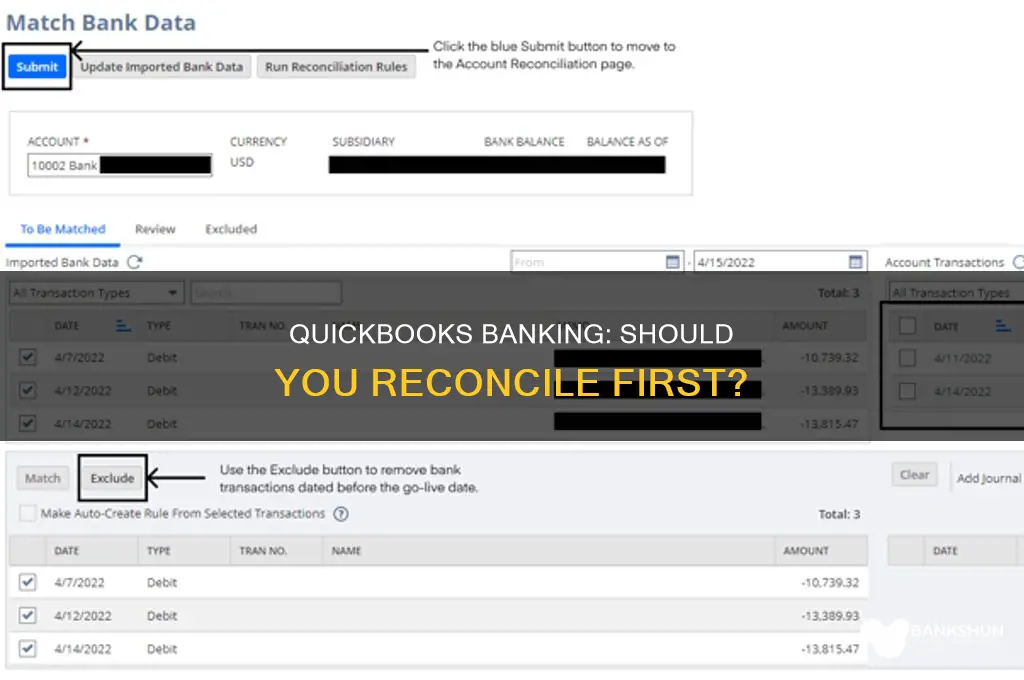

Reconcile is the process of matching your financial transactions in QuickBooks with your bank or credit card statements. This ensures that your records are accurate, up-to-date, and that no transactions have been duplicated. It is recommended to reconcile your accounts on a monthly basis. QuickBooks now offers AI-powered reconciliation, which can automatically import your bank statement and compare it to what's in QuickBooks. However, even if you have connected your bank and credit card accounts to QuickBooks, you still need to reconcile your accounts to the bank or credit card statements every month.

| Characteristics | Values |

|---|---|

| Definition | Reconciling means reviewing your bank and credit card statements and comparing them to what's in QuickBooks. |

| Purpose | To ensure accurate bookkeeping and financial records, prevent errors, and facilitate smoother audits. |

| Frequency | Recommended to be done on a monthly basis or periodically. |

| Process | Compare transactions on your statement with QuickBooks, check off matches, add missing transactions, and resolve discrepancies. |

| Tools | QuickBooks Online, AI-powered reconciliation, Hubdoc, ReceiptBank |

| Benefits | Accuracy, error prevention, audit assistance, better financial management, and identification of double entries or missing transactions. |

Explore related products

What You'll Learn

![]()

How to reconcile accounts in QuickBooks

Reconciling your accounts in QuickBooks is a significant part of bookkeeping, and it is recommended to do this monthly. It involves reviewing your bank and credit card statements and comparing them to what is in QuickBooks. This process ensures that no transactions are missed or entered twice, which could cause serious discrepancies in your file.

- Select the account you would like to reconcile.

- Verify that the beginning balance in QuickBooks matches the statement you are about to upload.

- Upload your bank statement.

- If you have QuickBooks Online Plus, Advanced, or Intuit Enterprise Suite, AI-powered reconciliation will automatically import your bank statement and compare it to what is in QuickBooks.

- If you do not have AI-powered reconciliation, you can manually reconcile by selecting 'Start reconciling' and filling in the ending date and ending balance information.

- Compare each transaction on your statement with what is in QuickBooks.

- If the transaction in QuickBooks matches your statement, check it off as reconciled.

- If there is a small discrepancy, such as the recipient being incorrect, select the transaction in QuickBooks and edit it so that the details match your statement.

- If a transaction in QuickBooks is not on your statement, leave it unchecked.

- When you have checked all transactions, the difference between your statement and QuickBooks should be $0.00.

- Click 'Finish Now' to complete the reconciliation.

It is important to note that you do not need to connect a bank or credit card to QuickBooks Online to reconcile. However, it is best to ensure that your beginning balance matches the balance of your real bank or credit card account when you start tracking transactions in QuickBooks.

Capital One Banks: Are They in Georgia?

You may want to see also

Explore related products

![]()

Common errors and how to avoid them

Bank reconciliation is the process of comparing your business's accounting records to your bank statement to ensure they match. It is a way to confirm that the cash you think you have is the actual amount in your account. While tools like QuickBooks can automate most of the reconciliation process, it is important to understand how to do it manually to spot and fix any problems.

- Duplicated transactions: Duplicated transactions are a common error that can occur when you match transactions without checking if they are accurate. To avoid this, always do a quick check of the date and description before matching transactions.

- Incomplete records: Incomplete records are another common error. To avoid this, ensure that you have entered all the items in the bank feed into QuickBooks. Work through everything in the bank feed until you have cleared it up to the date of the reconciliation.

- Data entry errors: Data entry errors, such as typos, wrong amounts, or incorrect dates, can occur during manual data entry. To prevent these errors, slow down, double-check entries, and use accounting software to minimize manual input. Utilize tools like QuickBooks to automate data capture from bank feeds and reduce the risk of manual mistakes.

- Reconciliation discrepancies: Discrepancies can arise from missing checks, transactions marked as reconciled that are inaccurate, or incorrect beginning or ending balances. To address these issues, review your unreconciled transactions, edit any mistakes, and ensure that your starting and ending balances match your bank statement for the reconciliation period.

- Timing issues: Timing issues can occur when a payment has not yet cleared or there are transactions recorded in QuickBooks but not on your bank statement, or vice versa. If you come across a discrepancy, flag it and make a note to dig into it later.

By being mindful of these common errors and following the suggested steps, you can improve the accuracy of your financial records and make more informed decisions based on real numbers.

How Mortgage Rates Vary Across Banks

You may want to see also

Explore related products

![]()

When to reconcile accounts

Reconciling your accounts in QuickBooks is a significant part of the bookkeeping process. It involves reviewing your bank and credit card statements and comparing them to your QuickBooks transactions to ensure that nothing was missed or double-counted. It is recommended to reconcile your accounts monthly to maintain accurate records.

When you're ready to start reconciling, select the account you want to reconcile and verify that the beginning balance in QuickBooks matches the statement you will upload. If you have QuickBooks Online Plus or Advanced, you can use the AI-powered reconciliation feature to automatically import and compare your bank statement with your QuickBooks data. This feature can detect reconciliation issues and save time. Alternatively, you can manually reconcile by choosing not to upload a bank statement and entering the ending date and balance information.

One by one, compare the transactions on your statement with those in QuickBooks. If a transaction in QuickBooks matches your statement, check it off as reconciled. If there are discrepancies, such as a minor error in the recipient, select the transaction in QuickBooks and edit the details to match your statement. If a transaction in QuickBooks is not on your statement, leave it unchecked. When you're finished, the difference between your statement and QuickBooks should be zero, indicating that your accounts are balanced and accurate.

You can also reconcile other control accounts in QuickBooks, such as your Petty Cash account, Payroll Clearing account, Superannuation liability account, or Loan accounts. This ensures that all your accounts are accurate and up to date. Additionally, if you have just one or two bank accounts and a relatively simple bookkeeping system, you may be able to handle the reconciliation yourself, but if you have a more complex system, you may consider hiring a professional for assistance.

Sperm Bank Workers: China's Unique Job

You may want to see also

Explore related products

![]()

How to handle discrepancies

To handle discrepancies in QuickBooks, you must first identify the cause of the discrepancy. Several factors could be responsible for discrepancies in your account balance:

- An incorrect ending balance was entered at the start of the reconciliation.

- Transactions that were already reconciled were edited or deleted.

- There are missing or duplicate transactions in QuickBooks.

- Transactions were entered into QuickBooks but have not cleared your bank yet.

- The last reconciliation was adjusted with a journal entry.

To identify the specific transaction(s) causing the imbalance, you can run a reconciliation discrepancy report. Here's how:

- Go to the Reports menu.

- Hover over Banking and select Reconciliation Discrepancy.

- Select the account you're reconciling and then select OK.

- Review the report and look for any discrepancies.

- Talk to the person who made the changes to understand the reason for the edits.

- Edit the transaction as needed to resolve the discrepancy.

If you are using QuickBooks Desktop, you can also try the following steps:

- In the Date From field, select the earliest date in QuickBooks for the account or leave it blank.

- In the Date To field, select the date of your last reconciliation.

- Go to the Filters tab and select the account you're reconciling in the Account field.

- In the Entered/Last Modified field, set the Date from to the date of your last reconciliation, and the Date to field to today's date.

- Select OK to run the report.

- Look for any discrepancies or transactions that don't match your bank statement.

- Discuss with the person who made the changes and edit the transaction as required.

- If needed, reach out to your accountant for guidance.

If you are unable to find any issues in your accounts, you may need to undo the previous reconciliation and redo it to ensure the accuracy of your financial data.

PNC Coin Counting Services: Available at Branches?

You may want to see also

![]()

Benefits of reconciliation

Reconciliation is an important process for maintaining accurate financial records and ensuring data integrity. It involves matching transactions in QuickBooks with bank or credit card statements to verify that the funds have moved and the total sum is correct. Here are some key benefits of reconciliation:

Accuracy and Data Integrity

Reconciliation helps to ensure that your financial records in QuickBooks match your bank and credit card statements. By comparing the two sets of records, you can identify and correct any discrepancies, errors, or irregularities that may have occurred during the recording process. This maintains the accuracy and integrity of your financial statements and books.

Cash Flow Management

Reconciliation allows you to confirm your true cash position and understand your cash flow better. By reconciling, you can verify that the cash you think you have is actually in your account. This helps you budget wisely, avoid overdrafts, and plan for upcoming expenses.

Fraud Detection and Protection

Regular reconciliation can help detect fraudulent transactions or unauthorized activities. By spotting these issues early, you can take prompt action to protect your business and prevent financial losses.

Timely Error Correction

Reconciliation helps catch incorrect charges, accounting mistakes, or missed transactions. By identifying these issues in a timely manner, you can maintain the accuracy of your financial data and avoid potential problems that could impact business decisions.

Streamlined Process

Tools like SaasAnt Transactions for QuickBooks simplify the reconciliation process by providing bulk import, export, and transaction management features. This saves time, reduces manual errors, and improves the overall accuracy of your financial records.

Banks and Old Currency: Are 10 Notes Still Valid?

You may want to see also

Frequently asked questions

Reconciling in QuickBooks refers to reviewing your bank and credit card statements and comparing them to what's in QuickBooks.

It is recommended to reconcile your accounts in QuickBooks on a monthly basis to ensure accurate bookkeeping and financial management.

Reconciliation in QuickBooks is crucial to maintaining accurate financial records. It helps identify discrepancies between your accounting records and bank statements, ensuring that transactions are not missed or double-counted.

Firstly, gather your latest bank or credit card statement, including the ending balance and statement date. Log into your QuickBooks Online account, select the account you want to reconcile, and upload your bank statement. Compare each transaction on your statement with those in QuickBooks, checking off the ones that match.

Yes, QuickBooks offers AI-powered reconciliation, which can automatically import and compare your bank statement to QuickBooks. This feature is built into QuickBooks Online Plus and Advanced plans.