Since the 2008 Global Financial Crisis, central bank balance sheets have grown significantly. This has led to questions about the ideal size of central bank balance sheets and whether large balance sheets are beneficial or detrimental. Central banks use their balance sheets to achieve their monetary policy goals, such as promoting maximum employment, stable prices, and moderate long-term interest rates. A large balance sheet allows central banks to influence securities prices and provide liquidity to firms and households, while also discouraging bank risk-taking. However, large balance sheets can also have negative consequences, such as market distortions and increased risk exposure for central banks. Additionally, a government's reliance on a central bank to hold its debt can threaten the central bank's independence. As such, it is important to understand the implications of large central bank balance sheets and determine the appropriate size to effectively implement monetary policy while maintaining independence and avoiding potential risks.

| Characteristics | Values |

|---|---|

| Size of central bank balance sheets | Have grown significantly since the Global Crisis |

| Traditional goals | Insufficient for assessing the success of modern central banking operations |

| Monetary policy | Stimulating or dampening aggregate demand to achieve price stability |

| Lender of last resort | Lending funds to solvent firms or other vehicles facing liquidity needs |

| Emergency financing | Provided to governments by central banks |

| Interest rates | Interest rate effect is not well-determined |

| Liquidity crisis | Central banks will want to reduce their balance sheets to the lowest level consistent with monetary policy |

| Risk | Market and credit risk to the central bank's assets |

| QE | Distortionary effects on markets |

| Fiscal consequences | Made central bankers nervous |

| Foreign currency reserves | High in financial systems where banks dominate |

| Central bank independence | Threatened by governments that rely on central banks to hold large quantities of debt |

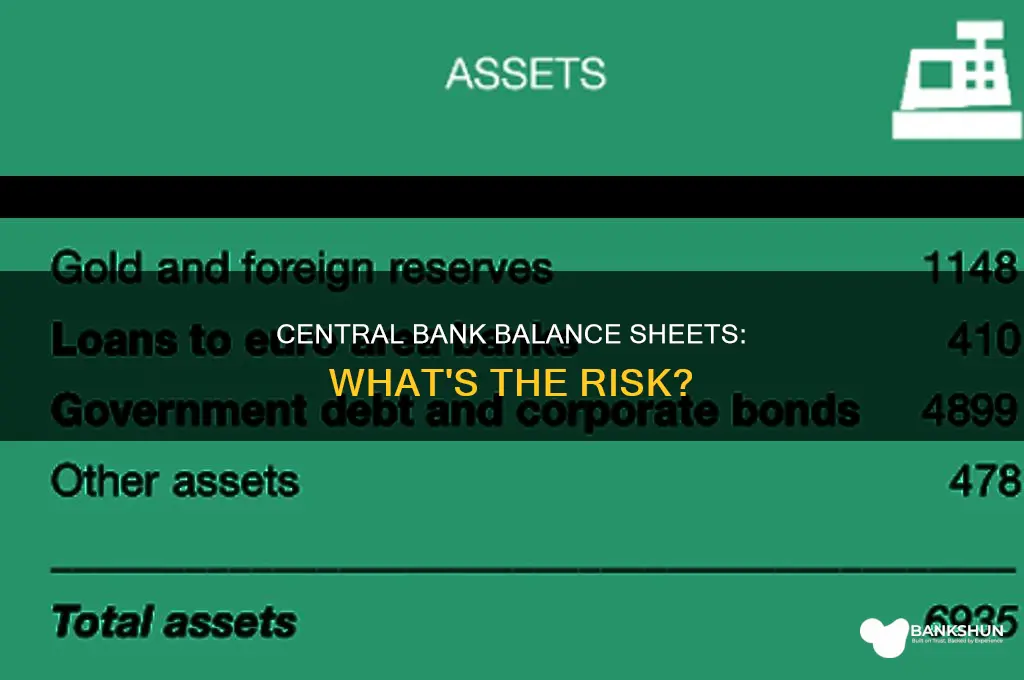

| Fed's balance sheet | Nearly $4.5 trillion as of 2014 |

| Global central bank balance sheets | More than $22 trillion as of mid-2014 |

| Fed assets | Mortgage-backed securities, loans extended to banks, foreign currency |

| Quantitative easing | Used to address the zero lower bound problem |

| Monetary policy | Promote maximum employment, stable prices, and moderate long-term interest rates |

Explore related products

What You'll Learn

![]()

Monetary policy decisions

The size of central bank balance sheets has grown significantly since the Global Financial Crisis. This has important implications for monetary policy decisions, which are a key function of central banks.

Firstly, large central bank balance sheets can impact monetary policy effectiveness. For instance, during the 2008 Global Financial Crisis and the COVID-19 pandemic, central banks engaged in quantitative easing (QE), purchasing large amounts of assets to lower long-term interest rates and stimulate the economy. These actions increased the size of central bank balance sheets and influenced securities prices and market liquidity.

Secondly, central banks need to carefully manage their balance sheets to maintain financial stability and achieve price stability. This includes ensuring sufficient reserves to meet commercial bank needs and managing the mix of assets to avoid excessive risk-taking or market distortions.

Thirdly, central bank independence is crucial. A large central bank balance sheet can make a government reliant on the central bank to hold its debt, potentially influencing monetary policy decisions. To maintain independence, central banks should aim for "asset neutrality," holding only the assets necessary for effective monetary policy implementation.

Finally, central banks must balance the benefits and costs of a large balance sheet. While a large balance sheet can provide tools for influencing the economy, it may also lead to market distortions, increased risk exposure, and fiscal consequences. Central banks must consider these trade-offs and communicate their actions clearly to maintain legitimacy and accountability.

In conclusion, large central bank balance sheets have significant implications for monetary policy decisions. Central banks must carefully manage their balance sheets to achieve their monetary policy goals while maintaining independence and minimizing potential negative consequences.

The Core Function of Banks: Facilitating Money and Credit

You may want to see also

Explore related products

![]()

Lender of last resort

The lender of last resort (LoR) is an institution, usually a country's central bank, that offers loans to banks or other eligible institutions that are experiencing financial difficulty or are considered highly risky or near collapse. In the United States, the Federal Reserve acts as the lender of last resort to institutions that do not have any other means of borrowing, and whose failure to obtain credit would dramatically affect the economy.

The lender of last resort provides emergency credit to financial institutions that are struggling financially and near collapse. The lender of last resort function is to lend funds to fundamentally solvent firms or other collective vehicles facing liquidity needs that cannot be met via private markets. This is a form of liquidity reinsurance to financial intermediaries which provide liquidity services to the economy more broadly. The central bank has an unlimited capacity to issue money (so long as its liabilities continue to be treated as money), making it the only institution that can take on this role at short notice.

The traditional way of preventing contagion from spreading throughout the banking system is to maintain an institution that is prepared to lend to other banks to provide liquidity. As long as banks are able to borrow funds to cover any sudden and unexpected withdrawal of deposits, a cascade effect can be stopped in its tracks. Providing banks with a guarantee of funds to cover any deposit withdrawals is the function of the central bank, acting in the capacity of lender of last resort. The central bank is called the lender of last resort because it is capable of lending in periods when no other lender is either capable or willing to lend in sufficient volume to prevent or end a financial panic.

Some argue that having a lender of last resort encourages moral hazard, meaning that banks can take excessive risks knowing that they will be bailed out. However, proponents of the lender of last resort function state that the potential consequences of not having a lender of last resort are far more dangerous than excessive risk-taking by banks. For example, during the 2008 financial crisis, large financial institutions such as Bear Stearns and American International Group, Inc. were bailed out.

How to Get Coin Wrappers From Banks?

You may want to see also

Explore related products

![]()

Selective credit

Central banks have transformed over the past 15 years, and their balance sheets have grown significantly. However, there is a lack of transparency and accountability in their operations. The public and their representatives lack the means to scrutinise central bank actions due to unclear purposes, objectives, and constraints.

To address this issue, it is recommended that central banks formally distinguish their operations by clearly setting out their purposes, objectives, and constraints. This includes their roles as lenders of last resort, market makers of last resort, providers of selective credit support, and emergency government financing.

By improving transparency and governance, central banks can maintain legitimacy and ensure that their actions align with their traditional goals of price and financial stability, as well as any new objectives that may have emerged in the post-Global Crisis era.

Jackson or Banks County: Where Am I?

You may want to see also

Explore related products

$17.96 $22.95

![]()

Emergency government financing

Central banks have a variety of functions, including providing emergency government financing. This involves providing needed funds directly to governments. Central banks can also steer credit to municipal governments and small businesses through implicit and explicit subsidies. For example, the Eurosystem's targeted longer-term refinancing operations (TLTROs) provide funding at favourable rates as low as -1% to banks, which then lend to businesses or households.

Central banks use their balance sheets to set the quantity or price of their money to achieve price stability objectives. They can influence the quantity of money in the economy by purchasing securities, which drives down long-term interest rates and compresses various risk premia, easing financial conditions and increasing aggregate activity and inflation. This process is known as quantitative easing (QE). QE can improve liquidity conditions in financial markets, particularly during crises, by encouraging greater bank lending. However, the effectiveness of QE is debatable, and it may not stimulate the economy according to some economic models.

The balance sheets of central banks, such as the US Federal Reserve, have grown in size and complexity in recent years due to the development of new lending facilities to address financial crises. The Federal Reserve's balance sheet includes various assets and liabilities, such as holdings of Treasury securities, foreign currency holdings, and lending to other institutions. Market participants closely study the Federal Reserve's balance sheet to understand the implementation of monetary policy.

To maintain legitimacy and accountability, central banks should distinguish their operations by clearly setting out their purposes, objectives, and constraints. This includes separating monetary policy decisions from emergency government financing activities.

Grocery Stores' Surplus Food: Donating to Food Banks?

You may want to see also

Explore related products

![]()

Liquidity crisis

The 2007-09 financial crisis led to a significant increase in the size of central bank balance sheets worldwide. During this period, central banks actively supplied liquidity to unstable financial systems. They extended loans to banks and, in some cases, non-traditional counterparties to support financial stability. This resulted in a substantial increase in reserves, which was often a byproduct of their quantitative easing (QE) policies.

Central banks play a crucial role as lenders of last resort, providing liquidity to sound firms facing illiquidity. This function has become more complex with the emergence of intermediaries, such as broker-dealers and money market funds, that engage in bank-like activities. As the only institution with the unlimited capacity to issue money, central banks are uniquely positioned to act as lenders of last resort.

In response to the financial crisis, several central banks, including the Federal Reserve, the Bank of England (BoE), and the Norges Bank, employed liquidity swaps. They exchanged liquid assets for less liquid ones, such as government securities, covered bonds, mortgage-backed securities, and corporate bonds. These swaps helped reduce liquidity spreads for less liquid assets and provided funding to institutions holding them.

To prepare for potential future liquidity crises, central banks aim to reduce their balance sheets to manageable levels. This strategy enhances their ability to expand quickly during crises and mitigates market and credit risks associated with large balance sheets. Additionally, it helps avoid the distortionary effects of QE on markets and the potential fiscal consequences that may concern central bankers.

While the normalization process remains uncertain, central banks are likely to expand their lending operations while reducing their outright asset holdings to ensure liquidity reaches all parts of the financial system.

Bank of the Sierra: Zelle Availability and Accessibility

You may want to see also

Frequently asked questions

A large central bank balance sheet can influence a variety of securities prices and provide a large volume of high-quality liquid assets to firms and households. It can also offer banks a large level of reserves at low cost, discouraging bank risk-taking in the form of liquidity and maturity transformation.

A large central bank balance sheet can pose a threat to central bank independence. When the central bank loses control of its balance sheet to the fiscal authority, the results can be catastrophic.

The answer depends on the policy goals and the nature of the financial system. In financial systems where banks dominate, central bank balance sheets will be larger. Where reserve requirements are high, central banks need bigger balance sheets to satisfy commercial bank reserve needs.