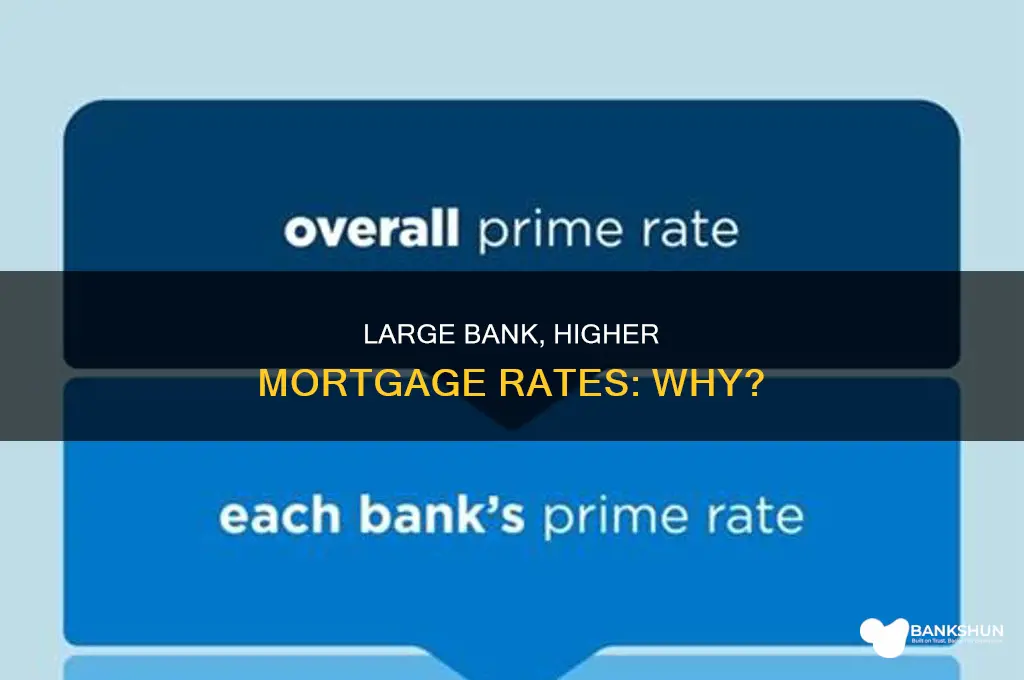

The size of a bank is a factor that influences the mortgage rates it offers. Larger banks, due to their extensive access to capital markets, can often provide competitive interest rates and fees, which may be lower than those offered by local lenders. However, smaller, local lenders may offer slightly higher interest rates and fees because of their limited scale of operations. It is important to note that mortgage rates are also influenced by various other factors, such as economic conditions, inflation, an individual's financial profile, and the housing market. Therefore, when considering a mortgage, it is advisable to compare rates from multiple lenders, including both large banks and local options, to secure the most favourable terms.

| Characteristics | Values |

|---|---|

| Variety of mortgage products and services | Larger banks tend to offer a wider range of mortgage products and services. |

| Interest rates | Larger banks may offer competitive interest rates due to their greater access to capital markets. However, local lenders' interest rates may be slightly higher or lower than larger banks. |

| Fees | Larger banks may have lower fees. |

| Personalised service | Smaller lenders may offer a more personalised service due to having fewer customers. |

| Stringent requirements | Larger banks may have more stringent requirements due to their larger customer base. |

| Local market knowledge | Local lenders may have deeper knowledge of the local real estate market, which can help secure better mortgage terms and rates. |

| Brand recognition and trust | Local lenders may provide a sense of stability and trust that larger banks can't match. |

| Flexibility | Local lenders may be more flexible in their underwriting criteria, considering unique circumstances. |

| Negotiation | Both larger and smaller lenders may offer negotiation on rates and fees. |

| Convenience | Larger banks often have more advanced online platforms and mobile apps, providing greater convenience in managing mortgages. |

| Loyalty | Loyalty to a bank may not always result in better rates; shopping around is recommended. |

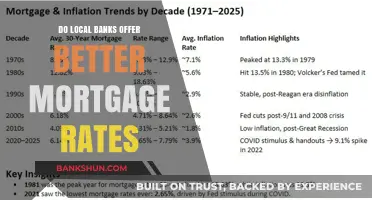

| Inflation | Inflation can cause mortgage rates to rise, as lenders may request higher interest rates to compensate for the loss in the buying power of the dollar. |

| Economic conditions | Economic factors such as employment, wages, and demand for home loans can impact mortgage rates. A strong economy and high demand tend to increase rates, while a slowing economy and decreased demand may lead to lower rates. |

| Federal Reserve activity | The Federal Reserve's monetary policy and interest rate decisions can influence mortgage rates. |

| Credit score | A higher credit score can lead to lower mortgage rates. |

| Down payment | A larger down payment can reduce the overall mortgage rate by lowering the loan-to-value ratio. |

| Closing costs | A lower interest rate may be disguised by higher closing costs, making the overall deal less advantageous. |

Explore related products

What You'll Learn

![]()

Local lenders vs. big banks

When it comes to choosing between local lenders and big banks for a mortgage, there are several factors to consider. Both options have their strengths and weaknesses, and the best choice depends on your specific needs and preferences.

One advantage of local lenders is their personalised service. Local lenders, such as credit unions or community banks, often provide more individualised attention and support throughout the mortgage process. They focus on building long-term relationships with their customers and can offer guidance beyond just the mortgage loan, such as helping you find a suitable realtor or neighbourhood. Local lenders also have a deep understanding of the local housing market, which can be beneficial in securing the right mortgage terms and rates for the specific community. This local knowledge can result in smoother and faster paperwork processes, as local real estate agents may have connections with local lenders.

Additionally, local lenders may offer more flexibility in their underwriting criteria. Due to their smaller size and independence, they can consider unique circumstances and non-traditional loan scenarios, making them more accessible to borrowers with varying financial backgrounds. Local lenders can also approve and close loans faster than big banks due to their streamlined underwriting processes.

On the other hand, big banks, or national lenders, have their advantages too. They offer a wider range of financial products and services, including various mortgage options. Due to their larger size and access to capital markets, they can often provide competitive interest rates and fees. Big banks also tend to have more advanced online platforms, allowing customers to manage their mortgages conveniently through mobile apps and automated payment features.

However, one of the drawbacks of big banks is the potential for higher fees and interest rates. Their emphasis on handling a large volume of loans may result in less flexibility and a more standardised approach to client solutions. The mortgage process with big banks may also lack the personal touch that local lenders offer, as customers are likely to be part of an assembly line of transactions.

It is worth noting that mortgage rates and fees can vary, and it is always advisable to shop around and compare offers from both local lenders and big banks. By evaluating multiple options, you can make an informed decision based on your specific financial situation and preferences for personalisation, convenience, and flexibility.

Local vs. Big Banks: Which is the Better Choice?

You may want to see also

Explore related products

![]()

Mortgage brokers vs. banks

When it comes to taking out a mortgage, you have two main options: using a mortgage broker or going directly to a bank. The best option for you will depend on your financial situation, preferences, and how much effort you want to put into the process.

Mortgage Brokers

Mortgage brokers act as intermediaries between you and direct lenders, including banks. They will discuss your needs and then reach out to their contacts to find loan options that fit your criteria. They can save you time by streamlining the mortgage process and offering a wider array of options. They can also help you navigate challenges in your mortgage application, such as a low down payment or poor credit score. Additionally, they can provide customized assistance and help with gathering the necessary documents. However, using a broker may be more expensive in the long term due to origination points and other costs. It's important to note that not all lenders work with mortgage brokers, and vice versa.

Banks

Going directly to a bank gives you more control over the homebuying process and may cost less. Banks, especially larger ones, often have access to capital markets, allowing them to offer competitive interest rates and fees. They also tend to have advanced online platforms and mobile apps for convenient mortgage management. However, banks may not offer the same level of personalized service due to their larger customer base. Additionally, banks are limited to their own lending products and don't have to disclose what they make on your loan, so you may pay more if you don't shop around aggressively.

In conclusion, both mortgage brokers and banks have their advantages and disadvantages. To get the best deal, it's recommended to obtain loan quotes from at least one broker and one bank, comparing their offers and turn times for underwriting, appraisal, and loan processing. Don't forget to consider credit unions and other direct lenders as well, as they can sometimes offer better rates and more personalized service. Ultimately, the decision between a mortgage broker and a bank depends on your unique circumstances and preferences.

Jim Banks' Re-election: What's the Timeline?

You may want to see also

Explore related products

![]()

The impact of inflation

Inflation has a significant impact on mortgage rates and the housing market. Inflation refers to the increase in the price of goods and services over time, which reduces the purchasing power of money. As inflation rises, central banks typically respond by increasing interest rates to combat inflationary pressures. This increase in interest rates makes borrowing more expensive, leading to higher costs for new mortgages.

Variable-rate mortgages are closely linked to the prime lending rate, which moves in tandem with the central bank's policy rate. Therefore, when inflation rises and the central bank increases rates, borrowers with variable-rate mortgages typically experience an increase in their mortgage payments. On the other hand, fixed-rate mortgages offer a consistent interest rate for the entire loan term, providing stability in monthly principal and interest payments, regardless of changes in interest rates.

However, even with a fixed-rate mortgage, inflation can impact future renewal terms. When inflation is high, investors demand higher returns, pushing bond yields and subsequently fixed mortgage rates higher. This can make refinancing more challenging in a high-inflation environment. Additionally, market reactions to inflation data can influence mortgage rates. If investors anticipate higher rates due to inflation concerns, yields on government securities may increase, prompting lenders to adjust their mortgage rates upward to maintain profit margins.

To navigate the challenges posed by inflation, homeowners and prospective buyers should understand the relationship between inflation and interest rates and consider strategies such as refinancing into fixed-rate mortgages. Consulting with a mortgage broker or financial advisor can help individuals make informed financial decisions and secure their financial futures.

PNC Banks in Clermont, Florida: Locations and Services

You may want to see also

Explore related products

![]()

The role of the Federal Reserve

The Federal Reserve is the United States' central bank. It guides the economy with the twin goals of encouraging job growth while keeping inflation under control. The Federal Open Market Committee (FOMC) pursues these goals through monetary policy: managing the supply of money and the cost of credit.

The Federal Reserve influences mortgage rates but does not set them outright. The Federal Reserve sets a range of different interest rates at various facilities. The range and the rates included are designed to influence banks to borrow from and lend to each other. The rate at which banks borrow and lend is then used by banks to set interest rates on all of their financial products, including mortgages. This rate is called the effective federal funds rate.

The Federal Reserve uses monetary policy to meet its mandate to promote price stability and maximum employment. If the Fed wants to boost the economy, it implements policies that help keep interest rates low. If the Fed wants to tighten the money supply, its policies typically result in higher interest rates.

The Federal Reserve's monetary policy decisions indirectly affect mortgage interest rates. If interest rates decrease and you have a variable-interest mortgage, your payments may go down. However, fixed-rate mortgage payments won't go down with interest rate changes. The Fed can also purchase mortgage-backed securities to lower mortgage rates and housing costs, if necessary, to support economic growth.

Canadian Banks: Free Notarization Services?

You may want to see also

Explore related products

![]()

Credit scores and history

Credit scores are a significant factor in determining mortgage rates. A higher credit score generally leads to a lower mortgage rate, as lenders perceive borrowers as lower-risk. Lenders use credit scores as a measure of creditworthiness, assessing factors like payment history, total debt, types of credit used, and length of credit history. Credit scores can change monthly, and even small increases can improve an applicant's chances of securing a favourable mortgage rate.

While most mortgage lenders use FICO scores, credit scores can differ depending on the credit reporting company used. For instance, lenders may refer to scores from Equifax, Experian, and TransUnion, taking the middle score to decide on the rate offered. FICO scores are based on factors such as credit history, income, and assets. A strong credit history, stable income, and substantial assets can lead to favourable mortgage rates with banks.

Credit scores influence the interest rates offered by lenders, and even small differences in credit scores can significantly impact the mortgage rate. A higher credit score can result in a lower interest rate, reducing the overall cost of the mortgage. Conversely, a lower credit score may lead to a higher interest rate, increasing the total amount paid over the loan's term.

Additionally, credit scores can determine eligibility for specific loan programs. For instance, FHA loans, backed by the Federal Housing Administration, are available to borrowers with lower credit scores but typically come with higher interest rates and fees compared to conventional loans for borrowers with good credit. Jumbo loans, which exceed conforming loan limits, often have higher rates due to the larger loan amounts.

When considering a mortgage, it is advisable to obtain loan quotes from both brokers and banks to find the best deal. Brokers can assist borrowers with challenges such as low down payments or poor credit scores by helping them access loan products with better rates. Banks may offer competitive rates due to their larger size and greater access to capital markets, but they may not provide the same level of personal attention as local lenders. Ultimately, shopping around and comparing rates from multiple lenders is the best way to secure a favourable mortgage rate.

How Banks Handle 1099-Ks for Bill Payments

You may want to see also

Frequently asked questions

Larger banks do not always have higher mortgage rates. Due to their size, larger banks often have more access to capital markets, allowing them to offer competitive interest rates and fees, which may be lower than those of local lenders.

Mortgage rates are influenced by various factors, including inflation, economic growth, Federal Reserve activity, housing market trends, and the overall condition of the bond market. Additionally, a borrower's credit score, debt-to-income ratio, and down payment amount can impact the mortgage rate offered by lenders.

To obtain a better mortgage rate, it is advisable to shop around and compare rates from multiple lenders, including both banks and brokers. Improving your financial profile, such as increasing your credit score and reducing debt, can also lead to more favourable rates.

While not always the case, online lenders have been known to surprise borrowers with substantially higher fees, especially at the time of closing a deal, leaving little choice but to proceed.

Mortgage brokers can help negotiate and find loan products with better rates, especially if your mortgage application has challenges like a low down payment or poor credit score. They can offer "rebate pricing," where you accept a higher interest rate in exchange for lower upfront costs.

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UY218_.jpg)