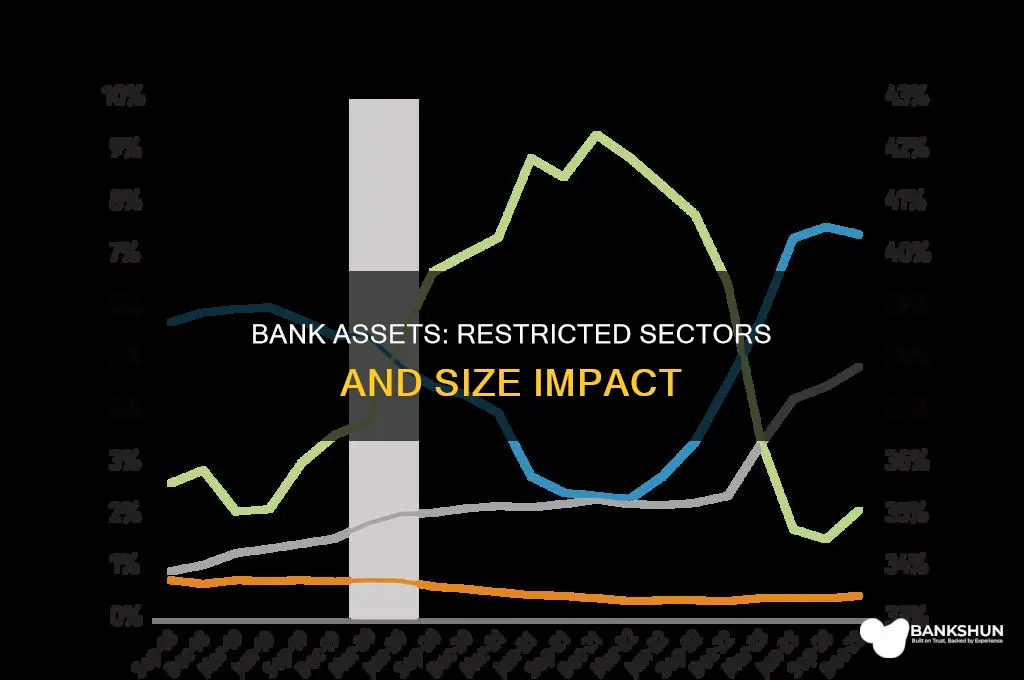

The size of a bank's assets is an important indicator of its performance and regulatory requirements. In the United States, banks are categorized into different tiers based on their asset size, with thresholds adjusted annually to account for inflation. These categories play a crucial role in determining the extent of regulatory evaluations and compliance requirements. For instance, small banks with assets under $346 million are typically evaluated using the Lending Test, which assesses their lending activities, including home mortgage, small business, and community development lending. As banks grow in asset size, they face more detailed Community Reinvestment Act (CRA) evaluations, with intermediate small banks (ISBs) and large banks subject to additional tests like the Community Development Test. The CRA, enacted in 1977, aims to combat redlining and ensure banks meet the credit needs of the communities they serve, including low- and moderate-income (LMI) families, small businesses, and small farms. The pandemic-induced balance sheet expansion has accelerated the transition of some community banks into higher CRA asset-size categories, leading to increased regulatory expectations and potential strategic adjustments.

| Characteristics | Values |

|---|---|

| Average asset size across the top 250 banks | $87.2 billion |

| Median asset size across the top 250 banks | $14.5 billion |

| Average asset size of the top credit unions in the top 250 | $6.25 billion |

| Small bank asset threshold | $600 million |

| ISB asset threshold | $2.5 billion |

| Small bank asset threshold (as of January 1, 2024) | $391 million |

| ISB asset threshold (as of January 1, 2024) | $1.564 billion |

| Small bank asset threshold (as of January 1, 2025) | $402 million |

| ISB asset threshold (as of January 1, 2025) | $1.609 billion |

Explore related products

What You'll Learn

![]()

US commercial banks' total assets grew by $5 trillion during the pandemic

The COVID-19 pandemic has had a significant impact on the global economy, and the banking industry is no exception. In the United States, the total assets of commercial banks grew by a staggering $5 trillion during the pandemic. This unprecedented expansion has had several consequences, including a push for some community banks to be categorised as intermediate small banks (ISBs) or large banks sooner than anticipated.

Prior to the pandemic, the US banking industry was already facing challenges, with the implementation of new regulations and evaluations. The Community Reinvestment Act (CRA), enacted in 1977, requires banks to meet the credit needs of the communities they serve. Regulators evaluate compliance by assessing lending and investment in low- and moderate-income (LMI) areas, as well as the proportion of lending to LMI families, small businesses, and small farms. The CRA also establishes asset-size thresholds for different categories of banks, which are adjusted annually based on inflation.

As of 2024, banks with assets under $346 million are considered small banks, those with assets from $346 million to $1.564 billion are ISBs, and banks with over $1.564 billion in assets are large banks. The asset thresholds are updated regularly, and as of December 31, 2025, ISBs will be defined as having assets between $402 million and $1.609 billion. These categorisations are important because they determine the type of evaluations banks undergo, with larger banks facing more detailed CRA performance evaluations.

The $5 trillion growth in total assets during the pandemic has had a significant impact on the CRA categorisations of US commercial banks. Some community banks, which previously fell into the small bank category, now meet the criteria for ISBs or even large banks. This change brings increased regulatory expectations and more stringent lending and investment requirements. Banks that have moved up a category must now demonstrate compliance with more rigorous standards, which may include additional data collection burdens.

While the pandemic has caused disruptions and challenges for the banking industry, the growth in total assets also reflects the resilience and adaptability of US commercial banks. The increase in assets has contributed to the overall stability of the banking sector, with total deposits remaining well above pre-pandemic levels. Additionally, loan balances have continued to grow, with community banks reporting strong loan growth, outpacing the industry average. Despite the uncertainties of the pandemic, US commercial banks have demonstrated their ability to navigate economic challenges and support the financial needs of their communities.

The Government's Role in Bank Closures: An Analysis

You may want to see also

Explore related products

![]()

CRA performance evaluations are more detailed for larger asset sizes

The Community Reinvestment Act (CRA) was enacted in 1977 to combat redlining and requires banks to meet the credit needs of the communities they serve. Regulators determine compliance by evaluating banks' lending and investment in low- and moderate-income (LMI) census tracts, as well as the proportion of their lending to LMI families, small businesses, and small farms. CRA performance evaluations are indeed more detailed for larger asset sizes.

The CRA asset-size thresholds are adjusted annually based on the average change in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a measure of inflation. As of December 31, 2025, an intermediate small bank is defined as a small institution with assets of at least $402 million for the prior two calendar years and less than $1.609 billion as of December 31 of either of the prior two calendar years. These thresholds are subject to change annually.

The three prudential regulators responsible for conducting CRA exams (the Office of the Comptroller of the Currency, Federal Deposit Insurance Corp., and Federal Reserve Board) use the same three asset-size categories. Banks with assets under $346 million are evaluated as small banks, while those with assets from $346 million to $1.384 billion are evaluated as Intermediate Small Banks (ISBs). Banks with assets above $1.384 billion are considered large banks.

Small banks are evaluated using the Lending Test, which assesses their lending activities, including home mortgage, small business, small farm, and community development lending. If consumer lending constitutes a substantial portion of a small bank's portfolio, it is also evaluated. ISBs are subject to both the Lending Test and the Community Development Test, which evaluates the number and amount of community development loans, investments, and services. Large banks are evaluated under a three-part lending, service, and investment test.

As banks increase in asset size, they are subject to more detailed CRA performance evaluations. The Lending Test is weighted more heavily when determining a bank's overall CRA rating. However, the Investment Test also considers the impact of qualified investments, which can benefit larger community banks with deeper local knowledge. Additionally, all banks are evaluated on their fair lending exam performance and responsiveness to customer complaints.

Banks and Old Currency: Are Old £20 Notes Valid?

You may want to see also

Explore related products

$31.26 $42.99

![]()

CRA asset-size thresholds are adjusted annually

The CRA (Community Reinvestment Act) regulations establish a framework for assessing financial institutions' records of meeting the credit needs of their entire communities, including low- and moderate-income neighbourhoods. The CRA asset-size thresholds are adjusted annually based on the average change in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a measure of inflation. This annual adjustment ensures that the evaluation of financial institutions remains dynamic and adapts to economic fluctuations.

Financial institutions are evaluated under different CRA examination procedures based on their asset-size classification. As banks increase in asset size, they become subject to more detailed CRA performance evaluations. The three prudential regulators responsible for conducting CRA exams—the Office of the Comptroller of the Currency, Federal Deposit Insurance Corporation, and Federal Reserve Board—use the same three asset-size categories: small banks, intermediate small banks (ISBs), and large banks.

The specific asset thresholds for these categories are adjusted annually, as mentioned earlier. For example, as of December 31, 2024, a small bank was defined as an institution with assets of less than $1.609 billion. An intermediate small bank was defined as a small institution with assets of at least $402 million as of December 31 of the previous two calendar years and less than $1.609 billion as of December 31 of either of the prior two years. These definitions are subject to change annually, with the thresholds effective from January 1 to December 31 of the following year.

The CRA asset-size thresholds are crucial as they determine the evaluation procedures and expectations for financial institutions. For instance, small banks are evaluated using the Lending Test, which assesses their lending activities, including home mortgage, small business, small farm, and community development lending. ISBs are subject to both the Lending Test and the Community Development Test, which evaluates their impact on the community.

It is worth noting that the regulatory agencies are continuously working to modernise CRA's implementing regulations. For instance, in 2020, the OCC proposed a new CRA framework that aimed to make performance evaluations strictly quantitative and significantly change the definitions of qualifying activities. However, due to the additional data collection burdens it imposed and the lack of inclusion of other regulatory bodies, the rule was rescinded in 2021, and the OCC returned to its 1995 rule.

Waiving Small Debt Amounts: Banks' Strategies and Consumer Impact

You may want to see also

Explore related products

![]()

CRA small bank and ISB definitions changed in 2020

The Community Reinvestment Act (CRA) was enacted in 1977 to combat redlining and requires banks to meet the credit needs of the communities they serve. In June 2020, the Office of the Comptroller of the Currency (OCC) changed the CRA framework, which included raising the small bank asset threshold to $600 million and the intermediate small bank (ISB) threshold to $2.5 billion. This change was reversed in December 2021, reverting to the 1995 rule, which sets the small bank asset threshold at $346 million and the ISB threshold at $1.384 billion.

The CRA regulations establish the framework and criteria for assessing a financial institution's record of meeting the credit needs of its entire community, including low- and moderate-income neighbourhoods. As banks increase in asset size, they are subject to more detailed CRA performance evaluations. The asset-size thresholds are adjusted annually based on the average change in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), a measure of inflation. For example, the CRA asset-size thresholds for small banks and ISBs in 2024 were $391 million and $1.564 billion, respectively, and these thresholds increased to $402 million and $1.609 billion in 2025.

The increased regulatory expectations associated with moving from a small bank to an ISB or from an ISB to a large bank can be challenging for community banks. Small banks are evaluated using the Lending Test, which considers their lending activities in home mortgages, small businesses, small farms, and community development. ISBs are also subject to the Community Development Test, which evaluates their responsiveness to the community development needs of their assessment areas through loans, investments, and services. Planning ahead and establishing processes to collect and maintain information for the Community Development Test can help small banks prepare for the transition to ISB evaluation procedures.

Who Lives in the West Bank?

You may want to see also

Explore related products

![]()

Average asset size across top 250 banks is $87.2 billion

The average asset size across the top 250 banks is $87.2 billion. This figure is significantly larger than the average asset size of credit unions, which is $6.25 billion. The median asset size among these top banks is $14.5 billion.

These figures highlight the vast financial resources held by the largest banks in the United States. The average asset size of $87.2 billion indicates that these banks possess substantial capital, enabling them to offer a wide range of financial services to their clients. It also underscores the economic power and influence that these institutions wield in the global financial system.

The asset size of a bank is a critical indicator of its overall financial health and stability. Banks with larger asset sizes tend to have a more diverse range of investments and holdings, which can contribute to their profitability and resilience in the face of economic downturns. Additionally, larger asset sizes can grant these banks access to exclusive regulatory frameworks, such as the Community Reinvestment Act (CRA) asset-size categorization.

The CRA, enacted in 1977, is a regulatory framework that evaluates banks' records of meeting the credit needs of their communities, including low- and moderate-income (LMI) neighbourhoods. Banks are categorised into different asset-size thresholds, which determine the specific CRA evaluation procedures they must follow. As of 2025, the CRA categorises banks with assets under $346 million as small banks, those with assets from $346 million to $1.384 billion as intermediate small banks (ISBs), and banks with over $1.384 billion in assets as large banks.

It is worth noting that accounting treatments can affect the reported assets of banks. For example, the use of US GAAP instead of IFRS in the United States leads to differences in the reporting of derivative assets. Adjustments to netting can significantly impact the total assets reported, as illustrated by the example of JPMorgan Chase, where adjustments resulted in a total asset value of $4,359.78 billion instead of $4,002.81 billion.

Barclaycard and Barclays: One and the Same?

You may want to see also