When sending an international wire transfer, one common question that arises is whether the recipient's bank address is required. The answer typically depends on the specific banking systems and regulations of the countries involved. In most cases, the recipient's bank name, SWIFT code (or BIC), and account number are essential for a successful transfer. However, some banks or financial institutions may also request the bank's physical address to ensure accuracy and compliance with international banking standards. It is always advisable to check with both the sender's and recipient's banks to confirm the exact information needed, as requirements can vary.

| Characteristics | Values |

|---|---|

| Bank Address Requirement | Generally required for international wire transfers to ensure accurate routing of funds. |

| Purpose of Bank Address | Identifies the recipient bank's location and facilitates proper processing of the transfer. |

| Additional Information Needed | SWIFT/BIC code, recipient account number, and recipient bank name are also essential. |

| Exceptions | Some banks or systems may use alternative identifiers (e.g., IBAN) instead of address. |

| Country-Specific Rules | Requirements may vary by country; always verify with the sending and receiving banks. |

| Online Banking Systems | Many platforms auto-populate bank address details when SWIFT/BIC or IBAN is entered. |

| Manual Transfers | Bank address is typically mandatory for manual or paper-based wire transfer forms. |

| Importance of Accuracy | Incorrect bank address can delay or fail the transfer, incurring additional fees. |

| Alternative Methods | Services like Wise or PayPal may bypass traditional bank address requirements. |

| Verification Process | Always double-check bank address, SWIFT/BIC, and other details before initiating transfer. |

Explore related products

What You'll Learn

![]()

Required Bank Details for Wire Transfers

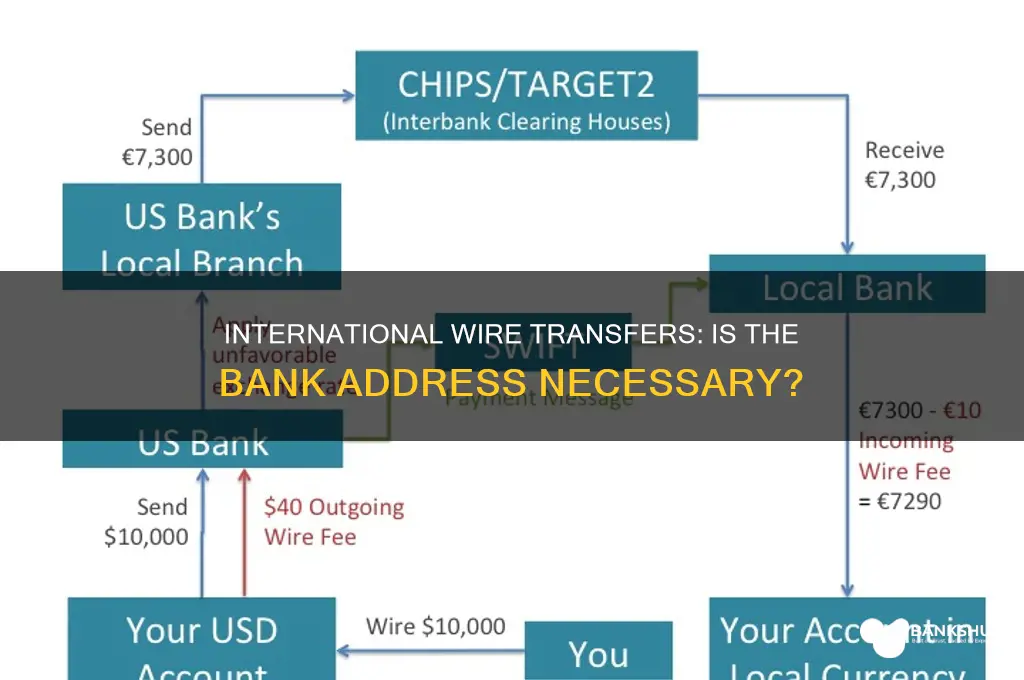

When initiating an international wire transfer, it is essential to provide accurate and complete bank details to ensure the transaction is processed smoothly. One of the most critical pieces of information required is the recipient's bank address. This is because international wire transfers often involve intermediary banks, and the bank address helps route the funds correctly through the global banking network. The bank address typically includes the physical location of the bank, which is used in conjunction with other details like the SWIFT code or routing number to identify the recipient’s bank.

In addition to the bank address, the SWIFT code (Society for Worldwide Interbank Financial Telecommunications) is a mandatory detail for international wire transfers. The SWIFT code is a unique identifier for banks worldwide and is crucial for ensuring the funds reach the correct financial institution. Without the SWIFT code, the transfer may be delayed or fail altogether. This code is usually 8 to 11 characters long and can often be found on the recipient’s bank statement or by contacting their bank directly.

Another essential detail is the recipient’s bank account number. This number is specific to the individual or business receiving the funds and ensures the money is deposited into the correct account. Depending on the country, additional identifiers like an IBAN (International Bank Account Number) may also be required. The IBAN is a standardized international account number used in many countries to facilitate cross-border transactions. It includes country-specific details and helps minimize errors in processing international payments.

The name of the recipient’s bank is also a required detail, as it provides clarity and confirms the destination of the funds. In some cases, the full legal name of the bank, rather than a shortened or colloquial version, may be necessary. Additionally, the recipient’s full name and address are often required to comply with international regulations, such as anti-money laundering (AML) and know your customer (KYC) rules. These details help verify the identity of the recipient and ensure the transfer is legitimate.

Lastly, some banks may require a purpose of payment or transaction reference code. This information helps both the sending and receiving banks understand the nature of the transfer and can be crucial for compliance purposes. Providing a clear and concise description of the payment ensures transparency and can prevent delays in processing. By gathering and verifying all these required bank details—including the bank address, SWIFT code, account number, and recipient information—you can ensure a successful and efficient international wire transfer.

Bank Transfers: Instant or Delayed?

You may want to see also

Explore related products

![]()

Difference Between Domestic and International Wire Transfers

When comparing domestic and international wire transfers, one of the most significant differences lies in the information required to complete the transaction. For domestic wire transfers, which occur within the same country, the sender typically needs the recipient’s bank account number, the bank’s routing number, and sometimes the recipient’s name. The process is relatively straightforward because both the sender’s and recipient’s banks operate under the same regulatory framework and often use the same currency. In contrast, international wire transfers require additional details due to the cross-border nature of the transaction. One critical piece of information often needed for international wires is the recipient bank’s address, along with its SWIFT code (or BIC), the recipient’s account number, and sometimes intermediary bank details. This is because international transfers involve multiple financial institutions and currencies, necessitating precise routing information to ensure the funds reach the correct destination.

Another key difference is the processing time. Domestic wire transfers are usually completed within the same business day or even instantly, depending on the banks involved. This efficiency is due to the streamlined communication between banks within the same country. International wire transfers, however, can take anywhere from 1 to 5 business days or more. The delay is attributed to the involvement of multiple banks, currency exchanges, and compliance checks, such as anti-money laundering (AML) and know-your-customer (KYC) verifications, which are more stringent for cross-border transactions.

Costs also differ significantly between domestic and international wire transfers. Domestic wires are generally less expensive, with fees ranging from minimal to free, depending on the bank and account type. International wires, on the other hand, incur higher fees, which can include charges from the sender’s bank, the recipient’s bank, and any intermediary banks involved. Additionally, currency conversion fees may apply, as international transfers often require converting funds from one currency to another. These costs can add up quickly, making international wires more expensive than their domestic counterparts.

The regulatory environment is another distinguishing factor. Domestic wire transfers are governed by the laws and regulations of a single country, making the process more uniform and predictable. International wire transfers, however, are subject to the regulations of both the sender’s and recipient’s countries, as well as international financial standards. This complexity often requires additional documentation, such as the purpose of the transfer, to comply with global financial regulations. The need for the recipient bank’s address in international wires is partly due to these regulatory requirements, ensuring transparency and traceability in cross-border transactions.

Finally, the level of complexity in the transfer process highlights the difference between domestic and international wires. Domestic transfers are typically handled through automated clearing house (ACH) systems or real-time gross settlement (RTGS) systems, which are well-established within a country. International transfers, however, often involve the SWIFT network, a global messaging system used by banks to securely exchange financial information. The inclusion of the recipient bank’s address in international wires is essential for accurate routing within this network, ensuring the funds navigate the intricate web of global financial institutions. In summary, while domestic wire transfers are simpler, faster, and cheaper, international wire transfers require more detailed information, take longer, cost more, and are subject to greater regulatory scrutiny.

The Banking Industry: Private or Public Sector?

You may want to see also

Explore related products

![]()

Role of SWIFT Code in Wire Transfers

When conducting an international wire transfer, one of the most critical pieces of information required is the SWIFT code. The SWIFT code, which stands for Society for Worldwide Interbank Financial Telecommunication code, is a unique identifier for banks and financial institutions globally. It plays a pivotal role in ensuring that international wire transfers are routed accurately and securely to the recipient’s bank. Unlike a bank address, which is a physical location, the SWIFT code is an alphanumeric code (8 to 11 characters) that acts as a digital address for banks in the global financial network. This code is essential because international wire transfers involve multiple banks and intermediaries, and the SWIFT code ensures that the funds reach the correct institution.

The primary role of the SWIFT code in wire transfers is to eliminate ambiguity in identifying the recipient bank. Without it, there is a high risk of errors, delays, or even loss of funds, as bank names and addresses can be similar or duplicated across different countries. For example, if you are sending money from the United States to a bank in Germany, the SWIFT code precisely identifies the German bank among thousands of others. It works in conjunction with other details like the recipient’s account number and bank address (if required) to create a seamless transfer process. While the bank address may provide additional context, the SWIFT code is the cornerstone of the transaction, ensuring the funds are directed to the correct institution.

Another critical aspect of the SWIFT code is its role in standardizing international communication between banks. SWIFT operates as a secure messaging system, allowing banks to exchange information about transactions, including wire transfers. When you initiate an international wire transfer, your bank sends a SWIFT message to the recipient bank, which includes details like the amount, currency, and purpose of the transfer. The SWIFT code embedded in this message ensures that the recipient bank is correctly identified, even if the bank address is incomplete or unclear. This standardization reduces the likelihood of errors and speeds up the processing time for international transfers.

While the SWIFT code is indispensable, it is important to note that some banks may still require the bank address for additional verification or compliance purposes. For instance, certain countries or banks may have specific regulations that mandate both the SWIFT code and the physical address of the recipient bank. However, the SWIFT code remains the primary identifier in the wire transfer process. It is always advisable to verify the recipient bank’s SWIFT code and address (if needed) before initiating the transfer to avoid complications. In essence, the SWIFT code is the linchpin of international wire transfers, ensuring accuracy, security, and efficiency in the global financial system.

In summary, the SWIFT code is not just a requirement but a fundamental component of international wire transfers. It serves as a unique identifier for banks, standardizes communication between financial institutions, and minimizes the risk of errors in routing funds. While a bank address may be requested in certain cases, the SWIFT code is the critical piece of information that ensures the transfer’s success. Understanding its role helps individuals and businesses navigate international transactions with confidence, knowing their funds will reach the intended destination securely and efficiently.

How Savings Bonds are Taxed by Banks

You may want to see also

Explore related products

![]()

Common Mistakes in International Wire Transfers

When initiating an international wire transfer, one of the most common mistakes is omitting or incorrectly providing the recipient bank’s address. While the primary details required for a wire transfer typically include the recipient’s bank name, SWIFT/BIC code, account number, and beneficiary information, the bank’s physical address is often overlooked. Many banks, especially in certain countries, require the full address of the recipient bank to ensure accurate routing of funds. Failing to include this detail can result in delays, additional fees, or even the rejection of the transfer. Always verify with your bank whether the recipient bank’s address is necessary and double-check its accuracy.

Another frequent error is misunderstanding the role of intermediary banks. International wire transfers often involve intermediary banks, which act as bridges between the sender’s bank and the recipient’s bank. Senders sometimes neglect to provide the intermediary bank’s details, including its address or SWIFT code, leading to complications. Even if the recipient bank’s address is correctly provided, omitting intermediary bank information can cause the transfer to fail. It’s crucial to confirm the entire payment route, including all intermediary banks, to ensure smooth processing.

A third common mistake is ignoring currency conversion and fees. Senders often assume that the amount they initiate will be the exact amount received. However, international wire transfers typically involve currency conversion and fees deducted by both the sender’s and recipient’s banks, as well as intermediary banks. Failing to account for these deductions can result in the recipient receiving less than intended. To avoid this, clarify with your bank how fees and exchange rates will be applied and consider options like “sender pays all fees” or “recipient gets the full amount” to ensure transparency.

Incorrectly formatting beneficiary details is another pitfall. Even if the bank address and other details are correct, mistakes in the beneficiary’s name, account number, or other identifying information can lead to transfer failures. Some countries have specific formatting requirements for account numbers or beneficiary names, and deviations can cause delays. Always verify the beneficiary’s details with them directly and ensure they match the bank’s requirements exactly.

Lastly, not confirming the transfer timeline and cutoff times can lead to unexpected delays. International wire transfers are not instantaneous and can take several business days to complete. Additionally, banks often have cutoff times for processing transfers, and missing these deadlines can push the transfer to the next business day. Failing to plan for these timelines can cause inconvenience, especially if the transfer is time-sensitive. Always check with your bank about processing times and cutoff hours to manage expectations effectively.

By avoiding these common mistakes—such as omitting the bank address, neglecting intermediary bank details, ignoring fees, misformatting beneficiary information, and overlooking transfer timelines—you can ensure a smoother and more efficient international wire transfer process. Always double-check all details and consult your bank for specific requirements to minimize errors.

Citizens One Bank Auto Payment: How It Works and Benefits

You may want to see also

Explore related products

![]()

How to Verify Bank Address for Wire Transfers

When initiating an international wire transfer, ensuring the accuracy of the recipient's bank address is crucial to avoid delays or potential loss of funds. The bank address is a key component of the transfer process, as it helps identify the specific financial institution that will receive the funds. To verify the bank address for wire transfers, start by obtaining the necessary details from the recipient. This typically includes the bank’s full name, physical address, SWIFT/BIC code, and routing or sort code, depending on the country. Double-check these details with the recipient to ensure there are no typos or omissions.

One of the most reliable methods to verify a bank address is by cross-referencing it with official banking directories or databases. Many countries maintain public registries or websites where you can confirm the legitimacy of a bank’s address and its corresponding codes. For instance, the SWIFT code directory is a widely used resource for international wire transfers. Additionally, some banks provide online tools or customer service support to help verify their branch addresses. If you’re unsure, contact your own bank and provide them with the recipient’s bank details—they can often assist in confirming the information before processing the transfer.

Another effective way to verify the bank address is by asking the recipient to provide an official bank statement or a letter from their bank confirming the address. This documentation should include the bank’s logo, contact information, and a stamp or signature for authenticity. While this step may require additional effort, it adds an extra layer of security, especially for large transactions. Be cautious of relying solely on informal communication channels, as errors or fraudulent information can easily occur.

If you’re still uncertain about the bank address, consider using a trusted third-party service that specializes in verifying financial institution details. These services often have access to comprehensive databases and can quickly confirm the accuracy of the information provided. While this may incur a small fee, it can save time and prevent potential issues. Always prioritize accuracy over speed when verifying bank addresses for wire transfers, as mistakes can lead to complications that are difficult to resolve.

Finally, once you’ve verified the bank address, carefully input the details into the wire transfer form. Review the information multiple times before submitting the transaction. Many banks allow you to save recipient details for future transfers, but it’s still essential to reconfirm the address periodically, as bank information can change. By following these steps, you can ensure a smooth and secure international wire transfer process, minimizing the risk of errors or fraud.

Title Insurance: A Must-Have for Banks

You may want to see also

Frequently asked questions

Yes, an international wire transfer typically requires the recipient’s bank address, along with other details like the SWIFT/BIC code, account number, and recipient’s name. The bank address helps ensure the funds are routed correctly.

Failing to provide the bank address can delay or prevent the transfer from being processed. The sender’s bank may not be able to locate the recipient’s bank, leading to potential errors or rejections.

No, the bank address is one of several required details. You’ll also need the recipient’s account number, the bank’s SWIFT/BIC code, and sometimes additional information like the recipient’s full name and address. Always verify all details with the recipient’s bank to ensure accuracy.