Islamic banking, grounded in Sharia principles that prohibit interest (riba) and promote risk-sharing and ethical investments, has emerged as a significant segment of the global financial system. Its contribution to economic growth is a topic of growing interest, as it operates on a unique model that emphasizes asset-backed financing, profit-sharing, and socially responsible investments. Proponents argue that Islamic banking fosters financial inclusion, mobilizes savings, and channels funds into productive sectors, thereby stimulating economic development. Critics, however, question its efficiency and scalability, particularly in modern, interest-based economies. Examining its impact on economic growth requires analyzing its role in enhancing financial stability, promoting entrepreneurship, and addressing income inequality, while also considering its integration with conventional financial systems and its adaptability to global economic challenges.

Explore related products

$52.92 $71

What You'll Learn

- Islamic Banking and Financial Inclusion: Enhancing access to financial services for underserved populations in Muslim communities

- Stability of Islamic Banking: Reducing systemic risks through asset-backed financing and ethical investment practices

- SME Financing in Islamic Banking: Supporting small and medium enterprises to foster economic development and job creation

- Islamic Banking and Infrastructure: Funding large-scale projects through sukuk (Islamic bonds) for economic growth

- Impact on GDP Growth: Measuring the contribution of Islamic banking to national economic output and productivity

![]()

Islamic Banking and Financial Inclusion: Enhancing access to financial services for underserved populations in Muslim communities

Islamic banking, rooted in Shariah principles, has emerged as a significant tool for promoting financial inclusion, particularly in Muslim communities where traditional banking systems often fall short. Financial inclusion refers to the accessibility and usability of financial services by all individuals and businesses, regardless of their economic status. In many Muslim-majority countries and communities, a substantial portion of the population remains unbanked or underbanked due to religious, cultural, or economic barriers. Islamic banking, with its emphasis on ethical and interest-free transactions, addresses these barriers by offering products that align with Islamic values, thereby encouraging greater participation in the formal financial system. This increased participation not only empowers individuals but also contributes to broader economic growth by mobilizing previously untapped resources.

One of the key ways Islamic banking enhances financial inclusion is through the provision of Shariah-compliant microfinance and small business loans. Traditional banking systems often exclude low-income individuals and small enterprises due to high collateral requirements or interest-based lending models, which are prohibited in Islam. Islamic microfinance institutions, such as those offering *Qard Hassan* (interest-free loans) or *Mudarabah* (profit-sharing) contracts, provide accessible financing options for underserved populations. These products enable entrepreneurs and small business owners to access capital without violating their religious beliefs, fostering economic activity and reducing poverty. By supporting micro and small enterprises, Islamic banking contributes to job creation and income generation, which are essential drivers of economic growth.

Another critical aspect of Islamic banking's role in financial inclusion is its focus on asset-backed and risk-sharing models. Products like *Murabaha* (cost-plus financing) and *Ijara* (leasing) ensure that financial transactions are tied to real economic activities, reducing speculative behavior and promoting stability. This approach not only aligns with Islamic principles but also builds trust among Muslim communities, many of whom are skeptical of conventional banking systems. As trust in financial institutions grows, more individuals are likely to save, invest, and participate in the formal economy. Increased financial participation, in turn, enhances the overall liquidity and investment in the economy, fostering sustainable growth.

Furthermore, Islamic banking plays a pivotal role in extending financial services to rural and remote Muslim communities, where access to traditional banking is limited. Through mobile banking, branchless banking, and digital financial services, Islamic banks are bridging the gap between urban and rural areas. For instance, mobile-based *Zakat* (obligatory almsgiving) collection and distribution systems ensure that charitable funds reach those in need efficiently, while digital platforms enable access to savings accounts, insurance, and investment products. This expansion of financial services not only empowers underserved populations but also integrates them into the broader economic ecosystem, amplifying the impact on economic growth.

In conclusion, Islamic banking is a powerful catalyst for financial inclusion in Muslim communities, addressing the unique religious, cultural, and economic challenges that hinder access to traditional financial services. By offering Shariah-compliant products, supporting micro and small enterprises, and leveraging technology to reach remote areas, Islamic banking empowers underserved populations and mobilizes their economic potential. As more individuals and businesses participate in the formal financial system, the resulting increase in savings, investment, and economic activity contributes significantly to overall economic growth. Thus, Islamic banking not only aligns with the principles of fairness and equity but also serves as a practical solution for inclusive and sustainable development.

Red Bank, New Jersey: Monmouth County's Gem

You may want to see also

Explore related products

$49.49 $59.99

![]()

Stability of Islamic Banking: Reducing systemic risks through asset-backed financing and ethical investment practices

Islamic banking, with its unique principles rooted in Shariah law, offers a distinct approach to financial services that inherently promotes stability and reduces systemic risks. One of the key mechanisms through which it achieves this is asset-backed financing. Unlike conventional banking, which often relies heavily on debt-based instruments and speculative activities, Islamic banking mandates that financial transactions be tied to tangible assets. This means that loans and investments are directly linked to real economic activities, such as trade, property, or infrastructure projects. By ensuring that financial transactions are backed by physical assets, Islamic banking minimizes the risk of asset bubbles and speculative excesses, which are often the root causes of financial crises in conventional systems. This asset-backed approach fosters a more stable financial environment by aligning financial activities with the real economy, thereby reducing the likelihood of systemic shocks.

Another critical aspect of Islamic banking that contributes to its stability is its ethical investment practices. Shariah law prohibits investments in sectors deemed harmful or unethical, such as gambling, alcohol, tobacco, and weapons. Additionally, it discourages excessive risk-taking and speculative behavior, such as short-selling and derivative trading, which are common in conventional finance. By adhering to these ethical guidelines, Islamic banking channels funds into productive and socially beneficial sectors, such as healthcare, education, and renewable energy. This not only promotes sustainable economic growth but also reduces the exposure of the financial system to volatile and high-risk sectors. As a result, Islamic banking is less prone to the boom-and-bust cycles that often plague conventional financial systems, thereby enhancing overall economic stability.

The risk-sharing principle in Islamic banking further reinforces its stability. Unlike conventional banking, where lenders bear minimal risk and borrowers carry the burden of repayment regardless of outcomes, Islamic finance structures transactions to share risks and rewards between parties. For example, in profit-sharing contracts like Mudarabah and Musharakah, both the financier and the entrepreneur share profits and losses based on pre-agreed terms. This alignment of interests encourages prudent decision-making and reduces moral hazard, as all parties are incentivized to ensure the success of the venture. By distributing risk more equitably, Islamic banking prevents the concentration of risk in any single entity, thereby reducing the potential for systemic failures.

Furthermore, Islamic banking’s focus on liquidity management through asset-backed instruments like Sukuk (Islamic bonds) provides an additional layer of stability. Sukuk represents ownership in tangible assets or projects, ensuring that investments are tied to real economic activities rather than speculative paper assets. This reduces the vulnerability of the financial system to liquidity crises, as the underlying assets can be liquidated if needed. In contrast, conventional bonds, which are often backed by debt, can exacerbate liquidity issues during times of financial stress. By prioritizing asset-backed securities, Islamic banking enhances the resilience of the financial system and mitigates the risk of contagion.

In conclusion, the stability of Islamic banking is underpinned by its asset-backed financing, ethical investment practices, risk-sharing principles, and focus on liquidity management. These features collectively reduce systemic risks by aligning financial activities with the real economy, promoting ethical behavior, and distributing risk more equitably. As a result, Islamic banking not only contributes to economic growth but also fosters a more resilient and stable financial system. Its principles offer valuable lessons for conventional finance, particularly in addressing the vulnerabilities that have led to recurring financial crises globally. By embracing the core tenets of Islamic banking, economies can build a more sustainable and inclusive financial framework that supports long-term growth while minimizing systemic risks.

M&T Banks in Boston: Locations and Services

You may want to see also

Explore related products

![Principles of Economics [California Social Studies 2019]](https://m.media-amazon.com/images/I/91t11MvJOvL._AC_UY218_.jpg)

![]()

SME Financing in Islamic Banking: Supporting small and medium enterprises to foster economic development and job creation

Islamic banking has emerged as a significant contributor to economic growth, particularly through its role in financing small and medium enterprises (SMEs). SMEs are widely recognized as the backbone of economies, driving innovation, employment, and GDP growth. Islamic banking, with its unique principles of risk-sharing, ethical investment, and asset-backed financing, offers a tailored approach to support SMEs, thereby fostering economic development and job creation. By aligning financial services with Sharia principles, Islamic banks provide SMEs with access to capital that is both sustainable and equitable, addressing the critical funding gap that often hinders their growth.

One of the key mechanisms through which Islamic banking supports SMEs is via profit-sharing models such as Mudarabah and Musharakah. In Mudarabah, the bank provides capital while the SME contributes expertise and management, with profits shared according to a pre-agreed ratio. This model encourages collaboration and aligns the interests of both parties, reducing the risk of default. Musharakah, on the other hand, involves joint ownership of a project, where the bank and SME share both profits and losses. These structures not only provide SMEs with much-needed financing but also promote a sense of partnership, fostering long-term growth and stability. Such risk-sharing arrangements are particularly beneficial for SMEs, which often face challenges in securing traditional loans due to collateral requirements and high-interest rates.

Another critical aspect of SME financing in Islamic banking is the emphasis on asset-backed financing, such as Ijara (leasing) and Murabaha (cost-plus financing). Ijara allows SMEs to acquire assets like machinery or property through a lease agreement, with the option to purchase the asset at the end of the term. This reduces the upfront financial burden on SMEs, enabling them to invest in productive assets without straining their cash flow. Murabaha, meanwhile, provides short-term financing for purchasing goods, with the bank buying the asset and selling it to the SME at a markup, ensuring transparency and compliance with Sharia principles. These instruments are particularly suited to SMEs, as they provide flexible and ethical financing solutions that support their operational and expansion needs.

Islamic banking also plays a pivotal role in job creation through its focus on real economic activities. By financing SMEs, Islamic banks enable these enterprises to scale their operations, hire more employees, and contribute to local economies. For instance, in countries like Malaysia and the UAE, Islamic banks have launched dedicated SME financing programs that prioritize sectors with high employment potential, such as manufacturing, agriculture, and services. These initiatives not only stimulate economic growth but also address unemployment, particularly among youth and marginalized communities. The ethical framework of Islamic banking ensures that financing is directed toward productive sectors, maximizing its impact on job creation and sustainable development.

Furthermore, Islamic banking contributes to economic resilience by promoting financial inclusion and stability. SMEs often struggle to access formal banking services due to stringent requirements and lack of credit history. Islamic banks, with their focus on relationship-based banking and alternative credit assessment methods, bridge this gap by offering tailored financial solutions to underserved SMEs. This inclusivity strengthens the overall economic ecosystem, as SMEs become more integrated into the formal economy, contributing to tax revenues and economic diversification. Additionally, the risk-sharing nature of Islamic financing reduces the likelihood of financial crises, as banks and borrowers share the burden of losses, fostering a more stable economic environment.

In conclusion, SME financing in Islamic banking is a powerful tool for fostering economic development and job creation. Through innovative Sharia-compliant instruments like Mudarabah, Musharakah, Ijara, and Murabaha, Islamic banks provide SMEs with accessible, ethical, and sustainable financing solutions. By supporting SMEs, Islamic banking not only drives economic growth but also promotes financial inclusion, stability, and equitable wealth distribution. As the global economy continues to evolve, the role of Islamic banking in nurturing SMEs will remain critical, ensuring that the benefits of economic development are shared widely and sustainably.

Muslim Women's Banking Experience: A Unique Perspective

You may want to see also

Explore related products

![]()

Islamic Banking and Infrastructure: Funding large-scale projects through sukuk (Islamic bonds) for economic growth

Islamic banking, with its unique principles rooted in Shariah law, has emerged as a significant contributor to economic growth, particularly through its role in funding large-scale infrastructure projects via sukuk (Islamic bonds). Unlike conventional bonds, sukuk represent ownership in an asset or project, aligning with Islamic finance’s prohibition of interest (riba) and emphasis on asset-backed transactions. This structure not only ensures compliance with religious principles but also fosters economic development by channeling investment into productive sectors. Infrastructure projects, such as roads, bridges, airports, and energy facilities, are capital-intensive and require long-term financing, making sukuk an ideal instrument. By attracting both domestic and international investors, sukuk mobilize substantial capital, thereby accelerating the completion of projects that enhance connectivity, productivity, and overall economic output.

The issuance of sukuk for infrastructure projects has proven to be a catalyst for economic growth in many Muslim-majority countries and beyond. For instance, Malaysia, a global leader in Islamic finance, has successfully utilized sukuk to fund major initiatives like the Kuala Lumpur International Airport and the Mass Rapid Transit (MRT) system. These projects have not only improved public services but also created jobs, stimulated local industries, and attracted foreign investment. Similarly, countries like Indonesia, Saudi Arabia, and the United Arab Emirates have leveraged sukuk to finance large-scale infrastructure, demonstrating its effectiveness in bridging the funding gap for developmental projects. The asset-backed nature of sukuk also reduces risk for investors, making it an attractive alternative to conventional debt instruments, particularly in emerging markets.

One of the key advantages of sukuk in infrastructure financing is its ability to align the interests of investors, governments, and the public. Since sukuk holders are partial owners of the underlying asset, they have a vested interest in the project’s success, encouraging transparency and accountability in project management. This ownership-based model also promotes ethical investment, as funds are directed toward tangible, socially beneficial projects rather than speculative ventures. Furthermore, sukuk can be structured to provide regular returns based on the project’s revenue, such as through Ijarah (lease) or Musharakah (partnership) contracts, ensuring a steady income stream for investors while supporting long-term economic growth.

The role of Islamic banking in infrastructure development extends beyond financing to fostering financial inclusion and stability. By providing Shariah-compliant investment opportunities, sukuk enable a broader segment of the population, including religiously observant Muslims, to participate in economic activities. This inclusivity can unlock significant domestic savings and investment, particularly in countries with large Muslim populations. Additionally, the asset-backed nature of sukuk reduces systemic risk compared to interest-based debt, contributing to a more resilient financial system. As governments and private entities seek sustainable funding for infrastructure, sukuk offer a viable and ethical solution that aligns financial objectives with societal and economic development goals.

In conclusion, Islamic banking’s utilization of sukuk for infrastructure financing plays a pivotal role in driving economic growth. By providing a Shariah-compliant, asset-backed alternative to conventional bonds, sukuk mobilize capital for large-scale projects that enhance productivity, create jobs, and improve public services. The success of sukuk in countries like Malaysia, Indonesia, and the Gulf states underscores its potential as a powerful tool for economic development. As the global demand for infrastructure continues to rise, Islamic banking, through innovative instruments like sukuk, is poised to make a lasting impact on economic growth while adhering to ethical and religious principles.

Central Pacific Bank Postage Stamps: Availability and Services Explained

You may want to see also

Explore related products

![]()

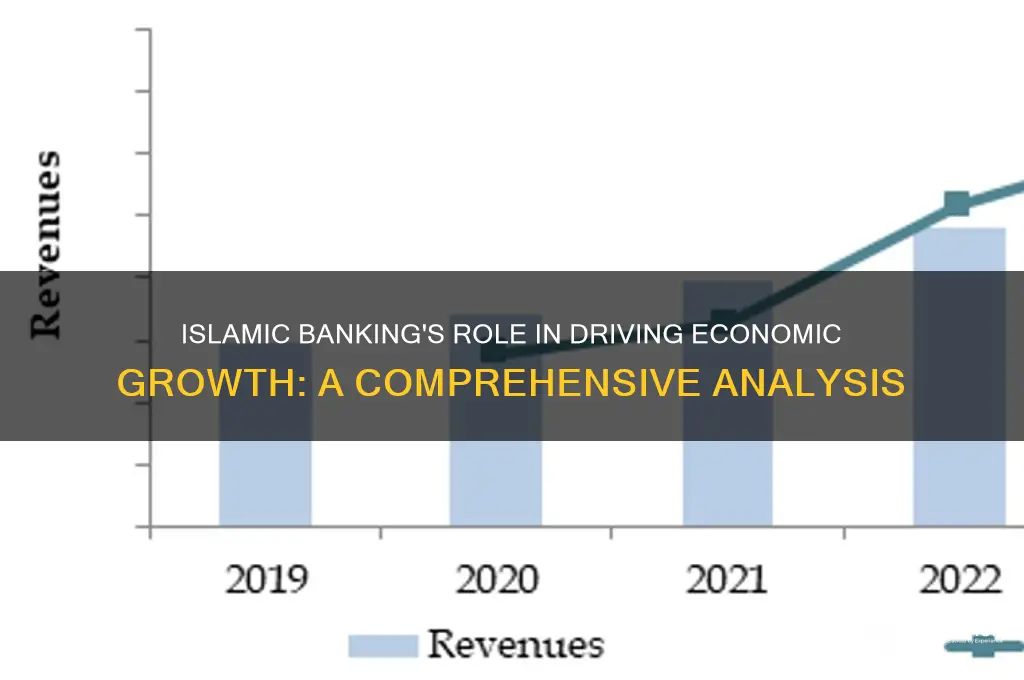

Impact on GDP Growth: Measuring the contribution of Islamic banking to national economic output and productivity

The impact of Islamic banking on GDP growth is a critical area of study in understanding its contribution to national economic output and productivity. Islamic banking, grounded in Sharia principles, operates on a profit-sharing model, avoiding interest-based transactions. This unique structure fosters financial inclusion by attracting individuals and businesses who prefer ethical financial practices, thereby expanding the economic participant base. Studies suggest that this inclusivity can stimulate economic activity, particularly in regions with significant Muslim populations, by channeling more funds into productive investments. For instance, research by Beck, Demirgüç-Kunt, and Levine (2007) highlights that financial systems aligned with religious beliefs can enhance savings and investment rates, which are key drivers of GDP growth.

Measuring the direct contribution of Islamic banking to GDP growth requires analyzing its role in mobilizing domestic savings and financing investment projects. Islamic banks emphasize asset-backed financing, such as Murabaha and Ijara, which are linked to real economic activities. This approach reduces speculative investments and encourages funding for tangible assets like infrastructure, real estate, and small and medium enterprises (SMEs). SMEs, in particular, are vital for job creation and innovation, contributing significantly to GDP. A study by the Islamic Research and Training Institute (IRTI) found that Islamic banking’s focus on SMEs in countries like Malaysia and Indonesia has positively influenced GDP growth by fostering entrepreneurship and local economic development.

Another dimension of Islamic banking’s impact on GDP growth is its role in enhancing financial stability. The risk-sharing nature of Islamic finance instruments, such as Mudaraba and Musharaka, aligns the interests of financiers and entrepreneurs, reducing moral hazard and adverse selection. This stability can lead to sustained economic growth by minimizing financial crises and ensuring continuous capital flow to productive sectors. For example, during the 2008 global financial crisis, Islamic banks demonstrated greater resilience compared to conventional banks, maintaining credit flows to businesses and households, which helped stabilize economies in countries like Malaysia and the UAE.

Quantifying the contribution of Islamic banking to GDP growth also involves assessing its impact on human capital development and productivity. Islamic banks often finance education and healthcare projects through Sukuk (Islamic bonds), which are critical for long-term economic growth. Improved access to education and healthcare enhances workforce productivity, a key determinant of GDP. Additionally, Islamic banking’s emphasis on ethical investments can attract foreign direct investment (FDI) from Sharia-compliant investors, further boosting economic output. A World Bank report (2015) noted that countries with robust Islamic financial sectors tend to experience higher FDI inflows, particularly from Gulf Cooperation Council (GCC) countries.

However, measuring the precise contribution of Islamic banking to GDP growth is challenging due to the lack of standardized metrics and data availability. Econometric models often struggle to isolate the impact of Islamic banking from other economic factors. Future research should focus on developing frameworks that account for the unique characteristics of Islamic finance, such as its emphasis on asset-backed transactions and risk-sharing. Policymakers can also play a role by promoting regulatory environments that support the growth of Islamic banking while ensuring its integration with national economic goals. In conclusion, while Islamic banking shows promise in contributing to GDP growth through financial inclusion, stability, and productivity enhancement, rigorous empirical studies are needed to fully quantify its impact.

Does Fun Bank Require a Minimum Balance? Exploring the Facts

You may want to see also

Frequently asked questions

Yes, Islamic banking contributes to economic growth by promoting financial inclusion, mobilizing savings, and channeling funds into productive sectors such as infrastructure, SMEs, and real estate. Its asset-backed and risk-sharing principles encourage ethical investment and reduce speculative activities, fostering sustainable economic development.

Islamic banking supports SMEs through profit-sharing models like Mudarabah and revenue-sharing contracts like Musharakah, which provide accessible financing without interest-based loans. This empowers SMEs to grow, create jobs, and stimulate local economies, thereby contributing to overall economic growth.

Yes, Islamic banking enhances financial stability by avoiding interest-based transactions and focusing on real economic activities. Its risk-sharing nature reduces systemic risks and encourages long-term investments, which can lead to more resilient economies and sustained growth.