The question of whether a bank has a substantial amount of cash on hand is a critical aspect of understanding its financial health and operational capabilities. Banks typically hold cash reserves to meet daily transaction demands, comply with regulatory requirements, and ensure liquidity for unexpected withdrawals or economic downturns. However, the amount of cash a bank maintains can vary significantly depending on factors such as its size, customer base, and strategic priorities. While some banks may prioritize holding larger cash reserves for stability, others might invest more in loans or other assets to maximize profitability. Analyzing a bank's cash position involves examining its balance sheet, liquidity ratios, and operational policies to gauge its ability to manage short-term obligations and support long-term growth.

Explore related products

What You'll Learn

- Cash Reserves: How much cash does the bank hold in reserve for daily operations

- Liquidity Ratio: What is the bank’s liquidity ratio, and is it sufficient

- Cash Flow: Does the bank have positive cash flow from lending and investments

- Withdrawal Capacity: Can the bank handle large customer withdrawals without issues

- Emergency Funds: Does the bank maintain enough cash for unexpected financial crises

![]()

Cash Reserves: How much cash does the bank hold in reserve for daily operations?

Banks maintain cash reserves to ensure they can meet daily operational demands, such as customer withdrawals, fund transfers, and settlement of transactions. The amount of cash a bank holds in reserve is carefully managed to balance liquidity needs with profitability. Typically, banks do not hold "lots of cash" in the sense of vast physical currency stacks, as this would be inefficient and risky. Instead, they keep a combination of physical cash in vaults and ATMs, and digital reserves in the form of deposits with central banks or in highly liquid accounts.

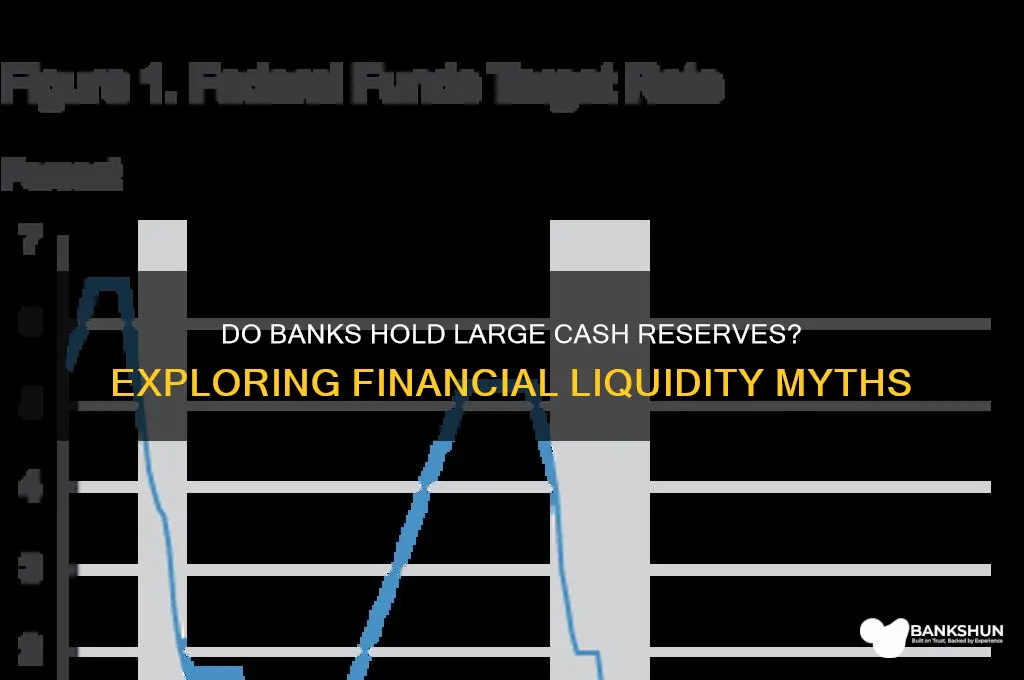

The level of cash reserves a bank holds is influenced by regulatory requirements, which vary by country. For instance, in the United States, the Federal Reserve sets reserve requirements mandating that banks hold a percentage of their deposits as reserves. These requirements ensure banks have enough liquidity to handle routine transactions and unexpected withdrawals. While reserve ratios have decreased in recent years due to changes in monetary policy, banks still maintain sufficient reserves to comply with regulations and manage their liquidity risk effectively.

In addition to regulatory mandates, banks also hold cash reserves based on their own risk management strategies and operational needs. Factors such as customer behavior, transaction volumes, and seasonal fluctuations influence how much cash a bank keeps on hand. For example, banks may increase reserves during periods of high withdrawal activity, such as holidays or economic uncertainty, to avoid liquidity shortages. Conversely, they may reduce reserves when demand is low to allocate funds to more profitable activities, like lending.

Physical cash reserves are primarily held in bank vaults and ATMs to meet immediate customer needs. The amount of physical cash varies depending on the bank's size, location, and customer base. Urban banks with high foot traffic, for instance, may hold more cash than rural branches. However, physical cash represents only a small portion of a bank's total reserves, as most liquidity is maintained in digital form for efficiency and security.

Ultimately, while banks do hold cash reserves for daily operations, the notion of them having "lots of cash" is a misconception. Their reserves are carefully calibrated to meet operational and regulatory demands without tying up excessive capital. By maintaining a balance between physical and digital reserves, banks ensure they can fulfill their obligations while maximizing profitability and minimizing risk. Understanding this dynamic is key to grasping how banks manage liquidity in the modern financial system.

Finding Icelandic Krona in US Banks

You may want to see also

Explore related products

![]()

Liquidity Ratio: What is the bank’s liquidity ratio, and is it sufficient?

The liquidity ratio is a critical financial metric used to assess a bank's ability to meet its short-term obligations without incurring significant losses. It measures the proportion of a bank's assets that are readily convertible into cash to cover withdrawals, loan demands, and other immediate liabilities. For banks, maintaining an adequate liquidity ratio is essential to ensure stability and confidence among depositors and investors. The most commonly used liquidity ratios in banking include the current ratio, quick ratio, and the liquidity coverage ratio (LCR), with the LCR being a key regulatory requirement under Basel III standards. The LCR specifically mandates that banks hold enough high-quality liquid assets (HQLA) to cover total net cash outflows over a 30-day stress period.

A bank's liquidity ratio is typically expressed as a percentage or a fraction, indicating the amount of liquid assets relative to its short-term liabilities. For example, an LCR of 100% means the bank has sufficient liquid assets to cover all projected cash outflows over the next 30 days. Regulatory bodies often set minimum thresholds for these ratios to ensure banks remain solvent during periods of financial stress. In the U.S., the Federal Reserve requires banks to maintain an LCR of at least 100%, while other jurisdictions may have similar or slightly different requirements. A ratio above the regulatory minimum is generally considered sufficient, but banks often aim for higher ratios to provide a buffer against unexpected liquidity shocks.

Determining whether a bank's liquidity ratio is sufficient involves analyzing both quantitative and qualitative factors. Quantitatively, the ratio should exceed regulatory thresholds and be benchmarked against industry peers. However, a high liquidity ratio alone does not guarantee financial health; it must be balanced with profitability, as excessive liquidity can lead to underutilized assets and reduced returns. Qualitatively, the composition of liquid assets matters—assets like cash, Treasury bonds, and other HQLA are more reliable than less liquid assets like loans or illiquid securities. Additionally, the bank's funding structure, deposit stability, and access to emergency liquidity facilities (e.g., central bank lending) play a crucial role in assessing overall liquidity adequacy.

Banks with a sufficient liquidity ratio are better positioned to withstand market volatility, deposit runs, or other liquidity crises. For instance, during the 2008 financial crisis, banks with robust liquidity ratios were more resilient than those heavily reliant on short-term wholesale funding. Conversely, a low liquidity ratio can signal potential distress, as the bank may struggle to meet its obligations without selling assets at a loss or seeking emergency funding. Investors and regulators closely monitor liquidity ratios as part of their risk assessment, as a decline in this metric can erode confidence and trigger further liquidity pressures.

In conclusion, a bank's liquidity ratio is a vital indicator of its ability to manage short-term cash needs and maintain operational stability. While regulatory thresholds provide a baseline, banks must strive for ratios that reflect their risk appetite, business model, and market conditions. Stakeholders should evaluate not only the ratio itself but also the quality of liquid assets, funding sources, and the bank's broader risk management framework. By maintaining a sufficient liquidity ratio, banks can ensure they have "lots of cash" in practical terms, safeguarding their operations and the broader financial system during both normal and stressed conditions.

Exploring PNC Bank Arts Center: Food Options and Dining Experience

You may want to see also

Explore related products

![]()

Cash Flow: Does the bank have positive cash flow from lending and investments?

Banks, as financial institutions, manage a complex interplay of cash inflows and outflows, making the question of whether they have "lots of cash" nuanced. At the heart of this inquiry is the concept of cash flow, specifically whether banks generate positive cash flow from their primary activities: lending and investments. Positive cash flow indicates that a bank’s income from these activities exceeds its expenses, ensuring liquidity and stability. To assess this, one must examine the bank’s core operations and financial statements, particularly the cash flow statement, which details operating, investing, and financing activities.

Lending is a bank’s primary source of cash flow. When banks issue loans, they receive interest payments from borrowers, which contribute to their cash inflows. However, the timing and reliability of these inflows depend on factors such as loan repayment terms, interest rates, and borrower creditworthiness. For instance, long-term loans may provide steady cash inflows over time, but they tie up capital for extended periods. Conversely, short-term loans generate quicker returns but may expose the bank to higher volatility. A bank with a diversified loan portfolio is more likely to maintain consistent positive cash flow from lending, as it mitigates risks associated with defaults or economic downturns.

Investments also play a critical role in a bank’s cash flow. Banks invest in various assets, such as government securities, corporate bonds, and money market instruments, to generate returns. These investments provide cash inflows through interest, dividends, or capital gains. However, the liquidity and risk profile of these investments vary. For example, highly liquid assets like treasury bills offer quick cash but lower returns, while long-term bonds provide higher yields but lock up cash for longer periods. A bank’s ability to maintain positive cash flow from investments depends on its asset allocation strategy and market conditions.

To determine if a bank has positive cash flow from lending and investments, one must analyze its net cash flow from operating activities. This metric reflects the cash generated from interest income, fees, and other banking services, minus operating expenses. A positive net cash flow indicates that the bank’s core operations are profitable and sustainable. Additionally, the net cash flow from investing activities should be examined to assess how effectively the bank manages its investment portfolio. If both metrics are positive, the bank is likely generating robust cash flow from its primary activities.

However, it’s essential to consider external factors that can impact a bank’s cash flow. Economic conditions, regulatory requirements, and market volatility can affect loan demand, interest rates, and investment returns. For instance, during a recession, loan defaults may rise, reducing cash inflows from lending. Similarly, rising interest rates can increase borrowing costs, squeezing profit margins. Banks must maintain sufficient liquidity and diversify their revenue streams to ensure positive cash flow in varying economic environments.

In conclusion, whether a bank has "lots of cash" depends on its ability to generate positive cash flow from lending and investments. By analyzing its cash flow statement, loan portfolio, and investment strategy, one can assess the bank’s financial health and liquidity. A bank with a well-managed lending operation, a diversified investment portfolio, and robust risk management practices is more likely to maintain positive cash flow, ensuring it has ample cash to meet obligations and support growth.

Equifax or Transunion: Which One Do Banks Prefer?

You may want to see also

Explore related products

![]()

Withdrawal Capacity: Can the bank handle large customer withdrawals without issues?

Banks are required to maintain a certain level of liquidity to ensure they can meet customer withdrawal demands, even during periods of high stress or unexpected events. Withdrawal capacity refers to a bank's ability to handle large customer withdrawals without facing liquidity issues or compromising its financial stability. This is a critical aspect of banking operations, as it directly impacts customer trust and the overall health of the financial system.

A bank's withdrawal capacity is primarily determined by its liquidity position, which is influenced by the amount of cash and cash equivalents it holds, as well as its ability to quickly convert assets into cash. Banks are required to maintain a minimum level of liquidity, often in the form of reserves held at the central bank, to ensure they can meet withdrawal demands. Additionally, banks may hold liquid assets such as government securities, which can be easily sold to raise cash if needed. The composition of a bank's asset portfolio, including the proportion of loans, investments, and cash, also plays a significant role in determining its withdrawal capacity.

When considering whether a bank can handle large customer withdrawals without issues, it's essential to examine its liquidity coverage ratio (LCR) and net stable funding ratio (NSFR). The LCR measures a bank's ability to withstand a 30-day stress scenario, while the NSFR assesses its ability to maintain a stable funding profile over a one-year period. A bank with a high LCR and NSFR is generally better equipped to handle large withdrawals, as it has a sufficient buffer of liquid assets to draw upon. Furthermore, banks with diverse funding sources, such as customer deposits, wholesale funding, and capital markets, are typically more resilient to withdrawal shocks.

In practice, banks employ various strategies to manage their withdrawal capacity, including stress testing, contingency planning, and liquidity risk management frameworks. Stress testing involves simulating extreme scenarios, such as a sudden surge in withdrawals, to assess the bank's ability to withstand the shock. Contingency plans outline the steps a bank will take to address liquidity shortfalls, including accessing emergency funding sources or selling assets. Effective liquidity risk management requires banks to monitor their liquidity position regularly, set internal limits, and maintain a robust liquidity risk appetite framework. By implementing these measures, banks can ensure they are well-prepared to handle large customer withdrawals without compromising their financial stability.

Ultimately, a bank's withdrawal capacity is a key indicator of its overall financial health and resilience. Customers, regulators, and investors closely scrutinize this aspect of banking operations, as it directly impacts the bank's ability to fulfill its obligations and maintain trust. Banks that prioritize liquidity management, maintain a strong capital base, and implement robust risk management frameworks are better positioned to handle large withdrawals without issues. As such, it is crucial for banks to regularly assess and strengthen their withdrawal capacity to ensure they can withstand various stress scenarios and maintain financial stability in the face of unexpected events. By doing so, banks can foster confidence among customers, regulators, and investors, and contribute to a more resilient financial system.

Underwriters Scrutinize Bank Charges: What You Need to Know

You may want to see also

Explore related products

![]()

Emergency Funds: Does the bank maintain enough cash for unexpected financial crises?

Banks play a critical role in maintaining financial stability, and one of the key aspects of this responsibility is ensuring they have sufficient emergency funds to weather unexpected financial crises. The question of whether a bank maintains enough cash for such scenarios is central to its ability to protect depositors, meet withdrawal demands, and continue operations during turbulent times. To address this, banks are required by regulatory bodies to hold a certain percentage of their deposits as reserves. These reserves serve as a buffer to cover sudden cash outflows, such as mass withdrawals during a financial panic or economic downturn. The exact reserve requirement varies by jurisdiction and the size of the bank, but it is designed to ensure liquidity without hindering the bank’s lending capabilities.

In addition to regulatory reserves, many banks voluntarily maintain excess cash or highly liquid assets as part of their emergency funds. This proactive approach allows them to respond swiftly to unforeseen events, such as a market crash, natural disaster, or geopolitical instability. For instance, during the 2008 financial crisis, banks with robust emergency funds were better equipped to handle the surge in withdrawal requests and maintain trust among their customers. However, striking the right balance is crucial; holding too much cash can reduce profitability, while holding too little can expose the bank to liquidity risks.

Another aspect of emergency funds is the bank’s access to central bank facilities, such as the Federal Reserve’s discount window in the United States. These facilities provide a safety net by offering short-term loans to banks facing temporary liquidity shortages. While this is not a direct cash reserve, it acts as a supplementary measure to ensure banks can meet their obligations during crises. However, reliance on central bank support should not replace a bank’s own emergency funds, as excessive borrowing can signal weakness and erode confidence.

Transparency and stress testing are essential tools for assessing whether a bank’s emergency funds are adequate. Regulators often conduct stress tests to evaluate how banks would fare under extreme scenarios, such as a severe recession or a run on deposits. These tests help identify vulnerabilities and ensure banks are prepared for the worst-case scenarios. Depositors and investors should also scrutinize a bank’s financial statements to understand its liquidity position and risk management practices.

Ultimately, the question of whether a bank maintains enough cash for unexpected financial crises depends on a combination of regulatory compliance, prudent management, and proactive planning. While banks are required to hold reserves, their ability to navigate crises effectively relies on a broader strategy that includes excess liquidity, access to central bank support, and robust risk assessment. For individuals and businesses, understanding a bank’s emergency fund policies can provide reassurance and help in making informed decisions about where to deposit or invest their money. In an uncertain financial landscape, a bank’s preparedness for emergencies is not just a regulatory requirement but a cornerstone of trust and stability.

Understanding Property Tax Payments: Does Your Bank Handle Them for You?

You may want to see also

Frequently asked questions

Banks typically keep a certain amount of cash on hand to meet daily withdrawal demands, but they do not store large amounts of cash in branches. Most funds are held electronically or invested in loans and securities.

Yes, you can withdraw a large sum of cash, but banks may require advance notice for amounts exceeding their daily cash limits. They may also ask for identification and the purpose of the withdrawal.

Banks minimize physical cash holdings to reduce security risks and operational costs. Instead, they rely on digital transactions and central reserves to manage liquidity efficiently.