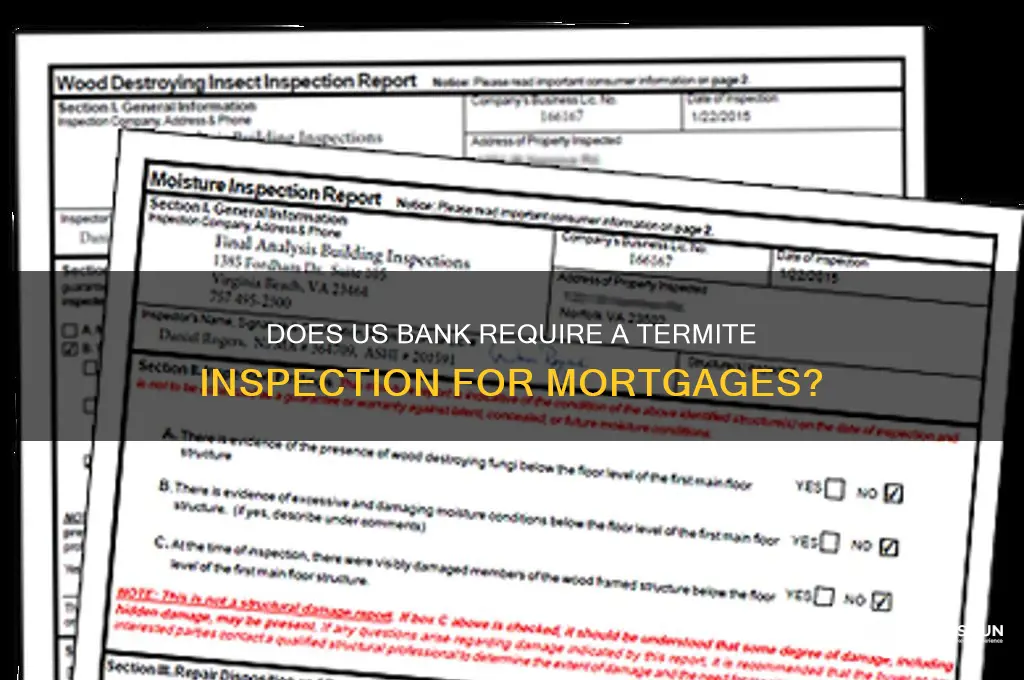

When considering a home purchase or refinance with U.S. Bank, one common question that arises is whether the bank requires a termite inspection. While U.S. Bank itself does not mandate a termite inspection as part of its standard lending requirements, the necessity of such an inspection often depends on factors like the property’s location, age, and condition. In areas prone to termite activity, lenders may recommend or require a termite inspection to ensure the property’s structural integrity. Additionally, some states or local jurisdictions may have specific regulations that necessitate a termite inspection. Borrowers should consult with their loan officer and review their loan agreement to understand if a termite inspection is required or advisable for their specific transaction.

| Characteristics | Values |

|---|---|

| Requirement | U.S. Bank does not universally require a termite inspection for all mortgage loans. |

| Loan Type | Requirements may vary depending on the type of loan (e.g., conventional, FHA, VA). |

| Property Type | Termite inspections are more likely required for properties in areas with high termite activity or for older homes. |

| State Regulations | Some states may mandate termite inspections regardless of lender requirements. |

| Appraisal Findings | If the appraisal report indicates signs of termite damage, U.S. Bank may require an inspection. |

| VA Loans | VA loans typically require a termite inspection as part of the appraisal process. |

| FHA Loans | FHA loans may require a termite inspection in certain regions or if there is evidence of infestation. |

| Conventional Loans | Less likely to require a termite inspection unless there are specific concerns about the property. |

| Cost Responsibility | The borrower is usually responsible for the cost of the termite inspection. |

| Inspection Report | If required, a clear termite inspection report is needed to proceed with the loan approval. |

Explore related products

What You'll Learn

![]()

USDA Loan Requirements

When considering a USDA loan, it's essential to understand the specific requirements and guidelines set by the United States Department of Agriculture (USDA). One common question among homebuyers is whether a termite inspection is mandatory for USDA loans. While the USDA itself does not explicitly require a termite inspection, it is often a condition imposed by lenders, including US Bank, to ensure the property meets certain standards. This inspection is crucial for identifying any termite damage or infestations that could compromise the structural integrity of the home, which is a key concern for both the lender and the borrower.

Lenders like US Bank may require a termite inspection as part of their underwriting process to mitigate risk. The inspection typically involves a licensed pest control professional examining the property for signs of termite activity, damage, or conditions conducive to infestations. If issues are found, repairs may be required before the loan can be approved. Borrowers should be prepared for this potential requirement and factor the cost of the inspection and any necessary repairs into their homebuying budget.

Another critical aspect of USDA loan requirements is the property’s appraisal. The appraisal not only determines the home’s market value but also assesses its condition to ensure it meets USDA standards. While the appraisal may include a general assessment of the property’s structure, it does not replace a detailed termite inspection. Therefore, lenders often mandate a separate termite inspection to complement the appraisal process, ensuring all bases are covered regarding the property’s condition.

In summary, while the USDA does not explicitly require a termite inspection for its loans, lenders like US Bank often impose this condition to protect their investment and ensure the property is safe and habitable. Borrowers pursuing a USDA loan should be aware of this potential requirement and be prepared to comply with it. Understanding and meeting all USDA loan requirements, including those related to property inspections, is crucial for a smooth and successful homebuying process.

The Connection Between Ray J and Sasha Banks

You may want to see also

Explore related products

![]()

FHA Loan Policies

When considering an FHA loan, it's essential to understand the specific requirements and policies that borrowers must adhere to, including those related to property inspections. The Federal Housing Administration (FHA) has established guidelines to ensure that properties financed through FHA loans meet certain safety and habitability standards. One common question among prospective homebuyers is whether a termite inspection is required as part of the FHA loan process. The answer is not a simple yes or no, as it depends on various factors, including the location of the property and evidence of termite activity.

In regions where termites are less common, FHA loan policies may not explicitly require a termite inspection unless there is visible evidence of infestation or damage. However, lenders often have their own overlay requirements, which might include mandating a termite inspection regardless of FHA guidelines. This is because lenders want to mitigate risks associated with pest damage, which can significantly affect the property's value and structural integrity. Therefore, even if the FHA does not strictly require it, borrowers should be aware that their lender might still insist on a termite inspection.

It's important for borrowers to understand that if a termite inspection is required and issues are found, the FHA loan policies may necessitate that these problems be resolved before the loan can close. Repairs must be completed by a qualified professional, and the property must be re-inspected to ensure compliance with FHA standards. The cost of termite inspections and treatments is typically the responsibility of the buyer, so it’s crucial to factor these potential expenses into the overall cost of purchasing the home.

In summary, while FHA loan policies do not universally require a termite inspection, they emphasize the importance of ensuring that properties are free from significant pest-related damage. The need for an inspection often depends on geographic location, evidence of termite activity, and lender-specific requirements. Borrowers should consult with their lender and be prepared for the possibility of a termite inspection, especially in areas prone to infestations. Understanding these policies can help streamline the FHA loan process and ensure that the property meets all necessary safety and habitability standards.

Does Synchrony Bank Offer Two-Step Verification for Enhanced Security?

You may want to see also

Explore related products

![]()

Conventional Loan Standards

When considering a conventional loan through U.S. Bank or any other lender, understanding the specific requirements and standards is crucial. Conventional loans, which are not insured by the federal government, often have their own set of guidelines that borrowers must meet. One common question that arises is whether a termite inspection is required as part of the loan process. While U.S. Bank, like many lenders, does not universally mandate a termite inspection for all conventional loans, certain conditions may necessitate one. For instance, if the property is located in an area known for termite activity or if there are visible signs of infestation, the lender may require an inspection to ensure the property’s structural integrity.

The appraisal is a critical component of conventional loan standards, as it determines the property’s value and condition. During the appraisal, the appraiser may note any visible issues, including potential termite damage. If such issues are identified, the lender may require a termite inspection and clearance before proceeding with the loan. This ensures that the property meets the lender’s standards and does not pose a risk to the borrower or the lender’s investment. Borrowers should factor in the potential cost and time associated with a termite inspection when planning their loan process.

In addition to termite inspections, conventional loan standards often include other property-related requirements. These may involve ensuring the home is structurally sound, has functioning systems (such as plumbing, electrical, and HVAC), and complies with local building codes. Lenders may also require repairs or improvements if significant issues are identified during the appraisal or inspection process. Borrowers should be proactive in understanding these requirements and addressing any concerns early in the loan process to avoid delays.

Ultimately, while U.S. Bank does not automatically require a termite inspection for conventional loans, borrowers should be aware that one may be necessary under specific circumstances. Understanding conventional loan standards and being prepared for potential inspections can help streamline the loan process and ensure a smoother transaction. Borrowers are encouraged to discuss these requirements with their lender and real estate professionals to fully understand their obligations and the steps needed to secure their loan.

Test Banks: A Textbook Companion?

You may want to see also

Explore related products

![]()

VA Loan Guidelines

When considering a VA loan, it's essential to understand the specific guidelines and requirements set by the U.S. Department of Veterans Affairs (VA). One common question among homebuyers is whether a termite inspection is required as part of the VA loan process. According to VA loan guidelines, a termite inspection is indeed mandatory in certain circumstances. The VA requires a termite inspection in areas where termite infestations are prevalent, as identified by the VA’s Termite Risk Map. This map categorizes regions based on the likelihood of termite activity, ensuring that properties in high-risk areas are inspected to protect both the buyer and the lender.

The VA’s termite inspection requirement is part of its Minimum Property Requirements (MPRs), which ensure that the property is safe, sanitary, and structurally sound. During the inspection, a licensed pest control professional assesses the property for evidence of termite damage or active infestations. If termites are found, the seller is typically responsible for treating the infestation and repairing any damage before the loan can be approved. This requirement safeguards the investment of the homebuyer and ensures the property meets the VA’s standards for habitability.

It’s important to note that the cost of the termite inspection is usually the responsibility of the buyer, though this can sometimes be negotiated with the seller. The inspection report must be completed on the official NPMA-33 form, which is specifically designed for VA loans. This form details the findings of the inspection and any necessary treatments or repairs. Without a satisfactory termite inspection report, the VA loan cannot be finalized, as it is a critical component of the appraisal process.

While the termite inspection requirement may seem like an additional step, it is a crucial aspect of the VA loan guidelines designed to protect homebuyers. Termite damage can significantly impact a property’s value and structural integrity, making this inspection a valuable safeguard. Borrowers should work closely with their lender and real estate agent to ensure all VA requirements, including the termite inspection, are met promptly. Understanding these guidelines upfront can help streamline the homebuying process and prevent delays.

In summary, the VA loan guidelines mandate a termite inspection in areas identified as high-risk for termite activity. This requirement is part of the VA’s broader effort to ensure properties financed through VA loans are safe and sound investments. Buyers should be prepared for this step, both in terms of scheduling and budgeting, to ensure a smooth loan approval process. By adhering to these guidelines, veterans and active-duty service members can confidently purchase homes that meet the VA’s high standards.

Why FDIC Insurance is Essential for Banks

You may want to see also

Explore related products

![]()

Termite Inspection Costs

When considering whether U.S. Bank requires a termite inspection for mortgage approval, it’s essential to understand the associated termite inspection costs. While U.S. Bank, like many lenders, may mandate a termite inspection for certain properties (especially in high-risk areas), the expense typically falls on the buyer or homeowner. The cost of a termite inspection varies based on several factors, including the size of the property, its location, and the inspection company’s pricing structure. On average, homeowners can expect to pay between $75 and $150 for a standard termite inspection. This fee is a one-time expense but is crucial for identifying potential termite damage that could affect the property’s value or structural integrity.

For larger homes or properties with complex structures, termite inspection costs may increase. Inspections for properties over 2,000 square feet can range from $150 to $300 or more. Additionally, if the inspector identifies signs of termite activity, further costs may arise from follow-up inspections or treatments. It’s important to note that while U.S. Bank may require the inspection, they do not dictate the pricing, which is set by the inspection company. Homebuyers should budget for this expense as part of their closing costs or home maintenance expenses.

Geographic location also plays a significant role in termite inspection costs. In states like California, Texas, or Florida, where termite activity is prevalent, inspections may be more expensive due to higher demand and the need for specialized equipment. Conversely, in regions with lower termite risk, costs may be on the lower end of the spectrum. Homebuyers should research local inspection companies and obtain quotes to ensure they are getting a fair price.

Some homeowners may wonder if termite inspection costs are negotiable. While prices are generally fixed, some companies offer discounts for first-time buyers, bundled services (e.g., combined termite and home inspections), or promotions. It’s worth asking about potential savings, especially if U.S. Bank’s requirement necessitates the inspection. Additionally, if the seller agrees to cover the inspection as part of the negotiation, this can alleviate the financial burden on the buyer.

Finally, it’s important to distinguish between a termite inspection and a termite treatment or repair, as the costs differ significantly. While an inspection typically ranges from $75 to $300, treatments can cost $500 to $2,500 or more, depending on the severity of the infestation. If U.S. Bank requires an inspection and issues are found, the lender may also require treatment before approving the loan. Understanding these distinctions helps homebuyers prepare financially and ensures compliance with the bank’s requirements. Always consult with U.S. Bank and a reputable inspection company to clarify expectations and costs.

Columbus Banks Accepting Rolled Coins Deposits

You may want to see also

Frequently asked questions

US Bank may require a termite inspection depending on the property's location, age, and condition, as well as the loan type. It is not a universal requirement but is often necessary in areas prone to termite activity.

Typically, the buyer is responsible for paying for the termite inspection, though this can vary based on the purchase agreement and local customs.

If significant termite damage is found, US Bank may require repairs to be completed before approving the loan. The seller or buyer may need to negotiate who covers the repair costs.

While US Bank may not always require it, skipping a termite inspection is risky, especially in areas with high termite activity. It’s a valuable step to protect your investment.

The validity period varies, but termite inspection reports are typically valid for 30 to 90 days. US Bank may require an updated report if the initial one expires before closing.