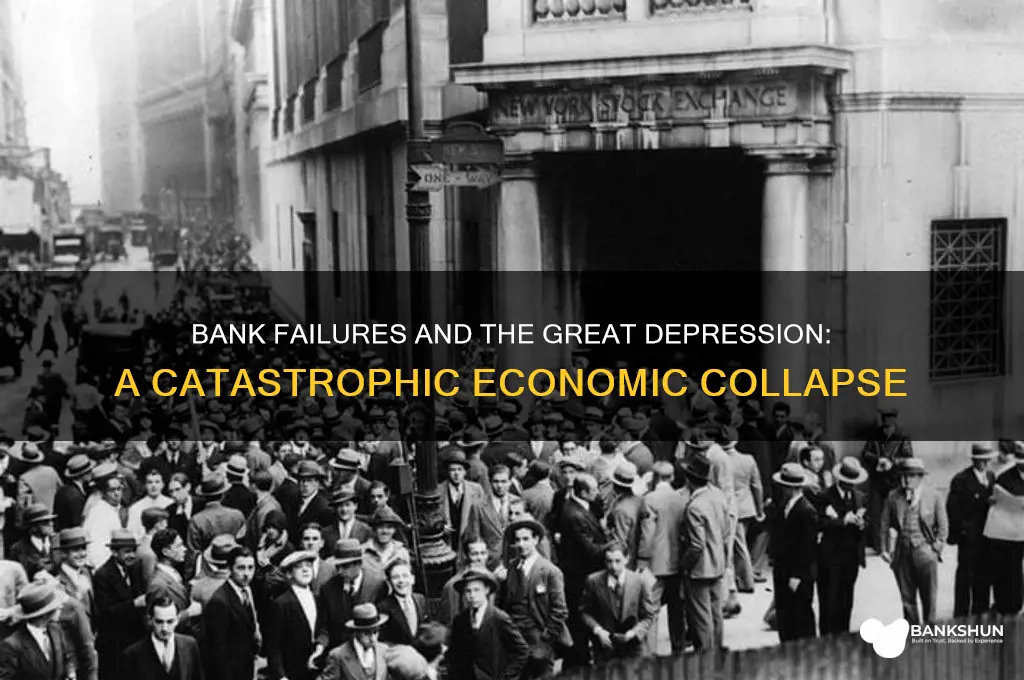

The Great Depression, one of the most severe economic downturns in history, was significantly exacerbated by widespread bank failures in the United States during the early 1930s. Following the stock market crash of 1929, public confidence in financial institutions plummeted, leading to panic-driven bank runs as depositors rushed to withdraw their funds. With limited reserves and heavily invested in risky assets, thousands of banks were unable to meet withdrawal demands, resulting in their collapse. These failures wiped out billions of dollars in savings, severely contracted the money supply, and crippled the credit system, halting economic activity. As businesses lost access to loans and consumers lost their savings, spending and investment plummeted, deepening the economic crisis and prolonging the Depression. The lack of federal deposit insurance and regulatory safeguards further amplified the crisis, highlighting the fragility of the banking system and its role in triggering and sustaining the Great Depression.

| Characteristics | Values |

|---|---|

| Bank Panics | Widespread fear and loss of confidence in banks led to mass withdrawals (bank runs), depleting reserves and forcing bank closures. |

| Contagion Effect | Failures of major banks triggered a domino effect, causing smaller banks to collapse due to interconnectedness. |

| Loss of Deposits | Approximately $140 billion (in today’s dollars) in deposits were lost during the Great Depression due to bank failures (adjusted from historical data). |

| Reduction in Lending | Bank failures reduced the money supply by 35% between 1929-1933, severely limiting credit availability for businesses and consumers. |

| Economic Contraction | Bank failures contributed to a 27% decline in GDP between 1929-1933, exacerbating the economic downturn. |

| Unemployment Spike | Unemployment rose from 3.2% in 1929 to 24.9% in 1933, partly due to reduced economic activity caused by bank failures. |

| Deflation | The money supply contraction led to deflation, with prices falling 25% between 1929-1933, further depressing economic activity. |

| Government Response | The Emergency Banking Act (1933) and the creation of the FDIC (1933) restored confidence and insured deposits up to $5,000 (now $250,000). |

| Long-Term Impact | Bank failures deepened and prolonged the Great Depression, with full economic recovery taking until the late 1930s/early 1940s. |

| Global Contagion | U.S. bank failures contributed to global financial instability, as international trade and credit markets collapsed. |

Explore related products

What You'll Learn

![]()

Bank runs and panic

The Great Depression was a period of severe economic downturn that began with the stock market crash of 1929 and lasted throughout the 1930s. One of the key factors that exacerbated this crisis was the phenomenon of bank runs and panic, which led to widespread bank failures and further destabilized the economy. A bank run occurs when a large number of customers withdraw their deposits simultaneously due to fears that the bank will go bankrupt. This panic-driven behavior was a direct response to the economic uncertainty of the time, as well as the lack of confidence in the banking system. During the early 1930s, rumors of bank insolvency spread rapidly, causing depositors to rush to banks to withdraw their money before it was too late. This self-fulfilling prophecy often led to banks exhausting their cash reserves and being unable to meet the demands of their customers, ultimately forcing them to close their doors.

Bank runs were not isolated incidents but rather a contagious process that spread from one bank to another, creating a domino effect. When one bank failed, it eroded public trust in the entire banking system, prompting depositors at other banks to question the safety of their own funds. This widespread panic was fueled by the absence of federal deposit insurance, which meant that depositors risked losing their entire savings if their bank failed. As more banks succumbed to runs, the financial system became increasingly fragile, leading to a contraction in credit and investment. Businesses and individuals found it difficult to obtain loans, which further stifled economic activity and deepened the depression. The inability of banks to function as intermediaries between savers and borrowers was a critical factor in the economic collapse.

The frequency and severity of bank runs were closely tied to the speculative excesses of the 1920s and the subsequent stock market crash. Many banks had invested heavily in the stock market or made risky loans during the boom years, leaving them vulnerable when the market collapsed. As asset prices plummeted, banks faced mounting losses, and their solvency came into question. Depositors, already shaken by the economic turmoil, reacted by withdrawing their funds en masse, accelerating the decline of troubled banks. This vicious cycle of panic and failure highlighted the interconnectedness of the financial system and the lack of safeguards to prevent systemic collapse. By 1933, over 9,000 banks had failed, wiping out billions of dollars in assets and destroying the financial security of millions of Americans.

The impact of bank runs and panic extended beyond the financial sector, contributing to a broader economic and social crisis. As banks closed, businesses lost access to credit, leading to layoffs and business closures. Unemployment soared, and consumer spending plummeted, creating a deflationary spiral. Farmers, already struggling with falling crop prices, were particularly hard hit as they could no longer secure loans to purchase seed or equipment. The loss of savings also devastated households, eroding confidence in the economic system and exacerbating poverty. The psychological effects of bank failures cannot be overstated, as the loss of life savings led to despair and a loss of faith in the future. This widespread insecurity further dampened economic activity, making recovery even more challenging.

Efforts to stem the tide of bank runs and panic were initially inadequate, as both state and federal authorities lacked the tools and resources to stabilize the banking system. However, the crisis prompted significant reforms, most notably the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 as part of the Glass-Steagall Act. The FDIC provided federal insurance for bank deposits, restoring confidence in the banking system and preventing future runs. Additionally, the Emergency Banking Act of 1933 allowed the government to inspect and reopen solvent banks, further stabilizing the financial sector. These measures, combined with broader economic policies, eventually helped to restore trust and lay the groundwork for recovery. The lessons of bank runs and panic during the Great Depression underscored the importance of regulatory oversight and deposit insurance in maintaining financial stability.

Does Citizens Bank Offer CoinStar Services? A Quick Guide

You may want to see also

Explore related products

![]()

Loss of consumer confidence

The Great Depression was a period of severe economic downturn that began with the stock market crash of 1929 and lasted throughout the 1930s. One of the critical factors that exacerbated the crisis was the loss of consumer confidence, which was significantly fueled by widespread bank failures. During the early 1930s, thousands of banks across the United States collapsed, eroding the trust that individuals and businesses had in the financial system. As banks failed, depositors lost their savings, and the fear of further collapses spread rapidly. This fear led consumers to adopt a cautious mindset, hoarding cash and drastically reducing spending. The reduction in consumer spending created a ripple effect, as businesses faced declining demand, leading to layoffs and further economic contraction.

The loss of consumer confidence was not merely a psychological response but a rational reaction to the tangible risks posed by bank failures. When banks closed their doors, people lost access to their money, which was often their life savings. This immediate financial insecurity made consumers hesitant to spend on anything beyond essentials. Additionally, the lack of deposit insurance prior to the establishment of the Federal Deposit Insurance Corporation (FDIC) in 1933 meant that depositors had no safety net. As a result, even those with money in stable banks began to withdraw their funds, fearing that their bank could be next. This widespread panic accelerated the decline in consumer spending, deepening the economic crisis.

Another critical aspect of the loss of consumer confidence was its impact on investment and credit. As trust in banks vanished, lending activity plummeted. Businesses, unable to secure loans, cut back on production and investment, leading to further job losses. Consumers, witnessing the economic instability, postponed major purchases such as homes, cars, and durable goods. This decline in investment and consumption created a vicious cycle, as reduced economic activity led to lower incomes, which in turn further diminished consumer confidence. The feedback loop between bank failures, reduced spending, and economic contraction became a defining feature of the Great Depression.

The loss of consumer confidence also had long-term psychological effects that outlasted the immediate bank failures. The trauma of losing savings and witnessing economic collapse instilled a deep-seated frugality in many Americans. Even as some banks reopened and economic conditions began to stabilize, consumers remained wary of spending or investing. This prolonged hesitation slowed the recovery process, as the economy relied heavily on consumer demand to rebound. The Great Depression thus highlighted the critical role that consumer confidence plays in economic stability and the devastating consequences when that confidence is shattered.

In conclusion, the loss of consumer confidence was a direct and devastating consequence of bank failures during the Great Depression. The collapse of banks not only wiped out savings but also created a pervasive fear that discouraged spending, investment, and borrowing. This reduction in economic activity deepened the crisis, leading to widespread unemployment and business failures. The establishment of deposit insurance and other financial reforms in the aftermath of the Depression aimed to restore trust in the banking system and prevent such a catastrophic loss of confidence in the future. The lesson from this period remains clear: consumer confidence is a fragile yet essential pillar of economic health, and its collapse can have far-reaching and long-lasting effects.

Sugar Mommas and Bank Info: A Red Flag?

You may want to see also

Explore related products

![]()

Credit contraction and deflation

The Great Depression was a period of severe economic downturn that began with the stock market crash of 1929 and lasted throughout the 1930s. One of the key mechanisms through which bank failures exacerbated and prolonged the depression was credit contraction. As banks failed in large numbers, the surviving banks became increasingly cautious, tightening their lending standards and reducing the availability of credit. This credit contraction had a cascading effect on the economy. Businesses, which relied heavily on bank loans to finance operations and expansions, found it difficult or impossible to secure the funds they needed. As a result, many businesses were forced to cut back on production, lay off workers, or close entirely. This reduction in economic activity further diminished the demand for goods and services, creating a vicious cycle of decline.

Closely linked to credit contraction was deflation, another critical factor in the deepening of the Great Depression. Deflation occurs when the general price level of goods and services falls, often due to a decrease in the money supply or a drop in aggregate demand. As banks failed and credit contracted, the money supply shrank, leading to deflationary pressures. Falling prices might seem beneficial to consumers, but during the Great Depression, deflation had devastating effects. Consumers and businesses delayed purchases, anticipating that prices would fall further, which led to a further decline in demand and production. Additionally, deflation increased the real burden of debt, as borrowers had to repay loans with dollars that were worth more than those they had borrowed. This made it even harder for individuals and businesses to meet their financial obligations, leading to more defaults and further bank failures.

The interplay between credit contraction and deflation created a self-reinforcing downward spiral. As credit became scarce, businesses and consumers reduced spending, which in turn led to lower prices and deflation. Deflation then discouraged borrowing and investment, as the real cost of debt rose, further tightening credit conditions. This cycle was particularly damaging because it undermined confidence in the financial system. Depositors, fearing additional bank failures, withdrew their funds, accelerating the collapse of more banks and reducing the money supply even further. The Federal Reserve, which could have intervened to stabilize the banking system and expand the money supply, failed to act decisively, allowing the contraction and deflation to worsen.

The impact of credit contraction and deflation was not limited to the financial sector; it had profound effects on employment and industrial output. With businesses unable to secure loans, investment in new projects and equipment plummeted, leading to widespread factory closures and job losses. Unemployment soared, reaching over 25% by 1933, as millions of workers were laid off. The reduction in household incomes further depressed consumer spending, exacerbating the deflationary trend. Farmers, already struggling with falling crop prices, were particularly hard-hit, as they could not obtain loans to sustain their operations. The combination of credit contraction and deflation thus created a systemic crisis that affected nearly every sector of the economy.

In conclusion, credit contraction and deflation were central to the economic collapse of the Great Depression, driven in large part by widespread bank failures. The reduction in available credit stifled business activity and investment, while deflation discouraged spending and increased the burden of debt. These forces interacted to create a feedback loop of declining economic activity, falling prices, and further financial instability. The failure of policymakers to address the credit contraction and deflationary pressures early on allowed the crisis to deepen, resulting in unprecedented economic hardship. Understanding this dynamic is crucial for recognizing the importance of a stable financial system and proactive monetary policy in preventing similar crises in the future.

Yemen's Central Bank: Rothschild Influence or National Control?

You may want to see also

Explore related products

![]()

Business closures and unemployment

The wave of bank failures during the early 1930s had a devastating ripple effect on businesses across the United States, triggering widespread closures and skyrocketing unemployment. When banks collapsed, they took with them the savings and credit lines that businesses relied on for daily operations, expansion, and inventory purchases. Small and medium-sized enterprises, which often lacked substantial cash reserves, were particularly vulnerable. Without access to capital, these businesses were unable to meet payroll, pay suppliers, or invest in production, leading to a rapid decline in their ability to function. This financial paralysis forced countless businesses to shut their doors, leaving behind empty storefronts and idle factories.

As businesses closed, millions of workers found themselves without jobs, exacerbating the unemployment crisis. The loss of employment was not confined to a single sector but spanned industries, from manufacturing and retail to agriculture and services. For example, factories that depended on bank loans to purchase raw materials were forced to halt production, laying off workers en masse. Similarly, retail stores, unable to restock shelves due to lack of credit, had to downsize or close entirely, further contributing to job losses. This cascade of business closures created a vicious cycle: fewer businesses meant fewer jobs, which in turn reduced consumer spending and deepened the economic downturn.

The impact of bank failures on unemployment was compounded by the lack of a robust social safety net during the Great Depression. With no federal unemployment insurance until 1935, jobless workers had little to fall back on, leading to widespread poverty and desperation. Families that relied on a single breadwinner were particularly hard-hit, as the loss of a job often meant the loss of their primary source of income. This economic insecurity further reduced consumer demand, as people cut back on spending to conserve what little money they had, which in turn forced more businesses to close and lay off workers.

Moreover, the psychological effects of business closures and unemployment cannot be overstated. The sudden loss of livelihoods shattered confidence in the economy and eroded trust in financial institutions. Workers who had once felt secure in their jobs now faced uncertainty and fear about their future. This loss of confidence discouraged investment and spending, perpetuating the economic stagnation. Businesses that might have otherwise survived were unable to attract customers or secure financing, leading to further closures and job losses.

In summary, bank failures during the Great Depression directly contributed to business closures and unemployment by cutting off access to essential credit and capital. The resulting wave of layoffs and shutdowns created a self-reinforcing cycle of economic decline, as reduced consumer spending and investment deepened the crisis. The absence of a safety net for unemployed workers further exacerbated the situation, leading to widespread poverty and a loss of confidence in the economy. This interconnected collapse of businesses and jobs remains a stark reminder of the critical role banks play in sustaining economic stability.

Routing Numbers: How Long Are They?

You may want to see also

Explore related products

![]()

Government policy failures

The Great Depression was a catastrophic global economic crisis, and while bank failures played a significant role, government policy failures exacerbated the situation, turning a severe recession into a prolonged depression. One of the most critical policy failures was the lack of a centralized banking system and regulatory oversight. Prior to the Great Depression, the United States had a decentralized banking system with thousands of small, independent banks. These banks were often undercapitalized and lacked diversification in their loan portfolios, making them highly vulnerable to local economic shocks. The Federal Reserve, established in 1913, failed to act as an effective lender of last resort or to regulate the banking system adequately. This lack of oversight allowed banks to engage in risky practices, such as excessive lending during the 1920s boom, which left them ill-prepared for the economic downturn.

Another major policy failure was the inadequate response to the initial wave of bank failures. As the economy began to contract in the late 1920s, bank runs became widespread, eroding public confidence in the financial system. Instead of implementing measures to stabilize the banking sector, such as guaranteeing deposits or injecting liquidity, the government and the Federal Reserve adopted a hands-off approach. This inaction allowed bank failures to spiral out of control, leading to a severe contraction in the money supply and credit availability. The failure to address the banking crisis promptly deepened the economic downturn, as businesses and consumers lost access to essential financial services.

The adherence to the gold standard also played a detrimental role in government policy failures. By maintaining the gold standard, the Federal Reserve was constrained in its ability to expand the money supply and stimulate the economy. Deflation became rampant as prices and wages fell, increasing the real burden of debt and further depressing economic activity. Additionally, the gold standard fostered a global deflationary spiral, as countries were forced to implement contractionary policies to defend their gold reserves. The refusal to abandon the gold standard until later in the Depression limited the government's ability to respond effectively to the crisis.

Furthermore, the implementation of protectionist policies, such as the Smoot-Hawley Tariff Act of 1930, exacerbated the economic collapse. This legislation raised tariffs on over 20,000 imported goods, triggering retaliatory measures from trading partners and severely restricting international trade. The decline in global trade reduced demand for American exports, further weakening the economy. Protectionist policies not only failed to protect domestic industries but also deepened the global economic crisis, demonstrating a profound failure in trade policy.

Lastly, the initial reluctance to pursue fiscal stimulus was a significant policy failure. President Herbert Hoover’s administration initially relied on voluntarist approaches, such as encouraging businesses to maintain wages and avoid layoffs, rather than direct government intervention. This approach proved ineffective in the face of a rapidly deteriorating economy. It was not until later, under the Franklin D. Roosevelt administration, that significant fiscal measures were taken through the New Deal. However, the delay in implementing robust fiscal policies allowed the Depression to worsen, highlighting the failure of early government responses to address the crisis effectively.

In summary, government policy failures—including inadequate banking regulation, a slow response to bank failures, adherence to the gold standard, protectionist trade policies, and reluctance to pursue fiscal stimulus—were central to the severity and duration of the Great Depression. These failures amplified the effects of bank collapses, turning a financial crisis into a decade-long economic catastrophe.

Fulton Bank Employment: Fingerprinting Requirement Explained for Job Seekers

You may want to see also

Frequently asked questions

Bank failures played a critical role in the onset of the Great Depression by eroding public confidence in the financial system. As banks collapsed, depositors lost their savings, leading to widespread panic and a rush to withdraw funds (bank runs). This liquidity crisis caused a severe contraction in credit, reducing spending and investment, which further deepened the economic downturn.

Bank failures were rampant due to a combination of factors, including speculative lending during the 1920s, a lack of deposit insurance, and the economic shock of the 1929 stock market crash. Many banks had invested heavily in risky assets, and when the economy contracted, borrowers defaulted on loans, leaving banks insolvent. The absence of a safety net for depositors exacerbated the crisis.

Bank failures devastated ordinary Americans by wiping out their savings, leaving many without access to funds for basic needs. The loss of credit also made it difficult for businesses to operate, leading to widespread job losses and economic hardship. This created a vicious cycle of reduced consumer spending, business closures, and further bank failures, prolonging the Great Depression.