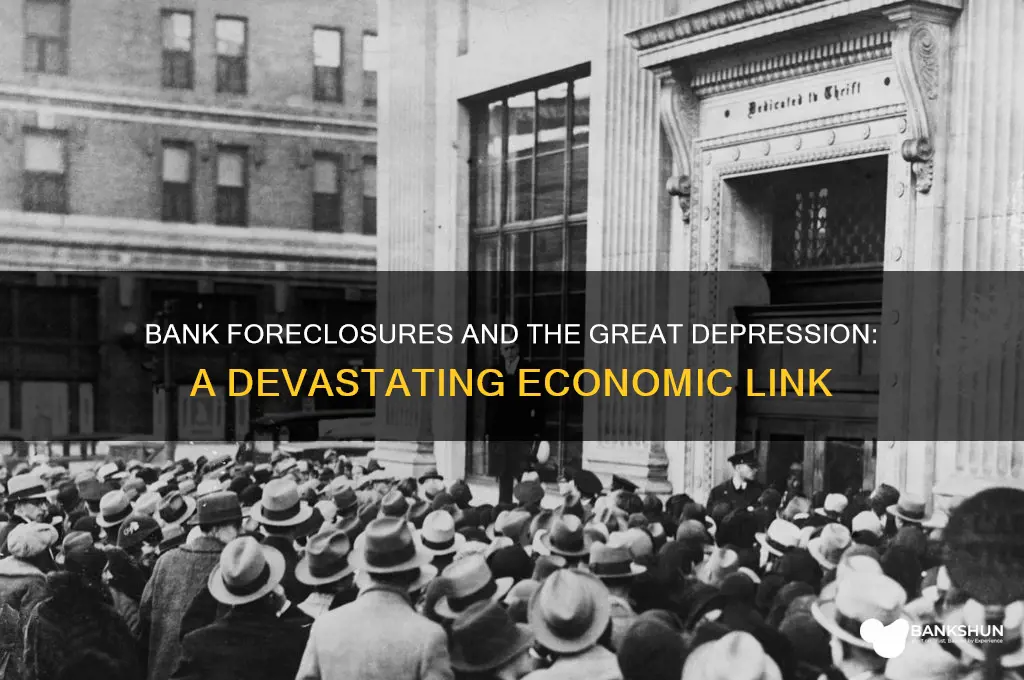

Bank foreclosures played a significant role in exacerbating the Great Depression, as the widespread default on mortgage payments led to a cascade of financial instability. During the 1920s, speculative lending practices and overvalued real estate markets created a fragile foundation for the economy. When the stock market crashed in 1929, unemployment soared, and homeowners were unable to meet their mortgage obligations, triggering a wave of foreclosures. Banks, already strained by deposit withdrawals and declining asset values, were forced to seize and liquidate properties, often at significantly reduced prices. This further depressed property values, eroded consumer wealth, and diminished bank reserves, leading to widespread bank failures. The resulting contraction in credit availability stifled economic activity, deepening the Depression and prolonging its devastating effects on families, communities, and the broader economy.

| Characteristics | Values |

|---|---|

| Bank Failures | Over 9,000 banks failed between 1929 and 1933, leading to widespread loss of savings and credit. |

| Wealth Destruction | Foreclosures wiped out homeowner equity, reducing consumer spending and investment. |

| Credit Contraction | Banks reduced lending due to insolvency, stifling business growth and economic activity. |

| Unemployment | Foreclosures and bank failures contributed to unemployment rising to 25% by 1933. |

| Deflation | Asset prices plummeted, exacerbating debt burdens and deepening the economic downturn. |

| Loss of Confidence | Public trust in the banking system collapsed, leading to hoarding of cash and reduced economic activity. |

| Agricultural Distress | Farm foreclosures surged, worsening rural poverty and reducing agricultural output. |

| Government Intervention | The Emergency Banking Act (1933) and the creation of the FDIC aimed to restore trust and stabilize banks. |

| Long-Term Economic Impact | Foreclosures and bank failures prolonged the Great Depression, with recovery taking over a decade. |

| Social Unrest | Widespread foreclosures and poverty fueled social unrest and political instability. |

Explore related products

What You'll Learn

- Foreclosure surge exacerbates housing market collapse during the Great Depression

- Bank failures due to foreclosures deepen economic crisis and unemployment

- Foreclosures reduce consumer spending, worsening deflation and economic stagnation

- Loss of homes leads to widespread homelessness and social instability

- Government intervention in foreclosures delays economic recovery during the Depression

![]()

Foreclosure surge exacerbates housing market collapse during the Great Depression

The foreclosure surge during the Great Depression played a pivotal role in exacerbating the housing market collapse, creating a vicious cycle of economic decline. As the stock market crashed in 1929, banks faced significant financial strain due to widespread loan defaults and a loss of depositor confidence. This led to a sharp reduction in lending capacity, forcing banks to call in outstanding loans and initiate foreclosures on properties whose owners could no longer make payments. The sudden influx of foreclosed homes flooded the market, driving down property values as supply far outstripped demand. This decline in home prices further weakened banks' balance sheets, as the collateral securing their loans was now worth significantly less, triggering a feedback loop of financial instability.

The surge in foreclosures directly contributed to the erosion of homeowner equity, leaving millions of Americans with properties worth less than their mortgages. This phenomenon, known as negative equity, discouraged consumer spending and investment, as households felt financially insecure and trapped in their homes. Additionally, the loss of homes to foreclosure displaced families, leading to a rise in homelessness and social unrest. The housing market collapse also undermined construction and related industries, as new homebuilding projects were halted due to the lack of demand and financing. This ripple effect further deepened the economic downturn, as unemployment soared and consumer confidence plummeted.

Banks' aggressive foreclosure practices during this period amplified the crisis by destabilizing communities and reducing the overall wealth of the population. As foreclosed properties were often sold at auction for a fraction of their original value, banks recovered only a small portion of their losses, while neighborhoods suffered from blight and declining property values. The concentration of foreclosures in certain areas created "redlining" effects, where entire communities were stigmatized as high-risk, further limiting access to credit and investment. This spatial concentration of distress deepened regional economic disparities, making recovery even more challenging.

The foreclosure surge also exposed systemic weaknesses in the financial system, particularly the lack of safeguards to prevent widespread defaults and the over-reliance on mortgage debt. Many loans issued during the 1920s were based on speculative assumptions of rising home values, which proved unsustainable. When the market turned, borrowers and lenders alike were caught off guard, leading to a cascade of failures. The absence of federal deposit insurance at the time further eroded trust in banks, leading to bank runs and additional failures, which in turn fueled more foreclosures. This interconnectedness between the banking sector and the housing market highlighted the need for regulatory reforms to prevent future crises.

In conclusion, the foreclosure surge during the Great Depression was both a symptom and a driver of the housing market collapse, creating a self-reinforcing cycle of economic distress. The interplay between bank foreclosures, declining property values, and reduced consumer spending deepened the severity and duration of the Depression. This period underscored the critical importance of a stable housing market to overall economic health and prompted significant policy changes, including the establishment of the Federal Housing Administration (FHA) and the Home Owners' Loan Corporation (HOLC), aimed at stabilizing the housing sector and preventing future collapses. The lessons from this era remain relevant, emphasizing the need for prudent lending practices, robust financial regulation, and support for homeowners during economic downturns.

Does Customers Bank Have Euros on Hand? Availability Explained

You may want to see also

Explore related products

![]()

Bank failures due to foreclosures deepen economic crisis and unemployment

The wave of bank failures during the Great Depression was both a symptom and a catalyst of the broader economic collapse, with foreclosures playing a central role in this vicious cycle. As the Depression deepened, farmers and homeowners defaulted on their loans in unprecedented numbers, unable to meet mortgage payments due to plummeting incomes and deflation. These defaults led to a surge in foreclosures, which overwhelmed banks already struggling with illiquidity and insolvent balance sheets. When banks repossessed properties, they were left with assets that were difficult to sell in a depressed real estate market, further eroding their financial health. This cascade of foreclosures depleted banks' capital reserves, making it impossible for them to honor withdrawal requests from panicked depositors, ultimately leading to widespread bank failures.

Bank failures exacerbated the economic crisis by destroying public confidence in the financial system. As banks closed their doors, depositors lost access to their savings, which were often uninsured at the time. This loss of wealth reduced consumer spending and investment, key drivers of economic activity. Businesses, unable to secure loans or access their funds, were forced to lay off workers or shut down entirely. The resulting surge in unemployment created a feedback loop: fewer employed individuals meant reduced consumer demand, leading to further business closures and bank insolvencies. This cycle deepened the Depression, as the economy contracted and unemployment soared to unprecedented levels.

The impact of bank failures on unemployment was particularly severe due to the multiplier effect of lost financial intermediation. Banks serve as critical intermediaries in the economy, channeling savings into loans that fund business operations and expansion. When banks failed, this credit pipeline dried up, leaving businesses without the capital needed to sustain operations or hire workers. Small businesses, which relied heavily on local banks for credit, were especially hard-hit, contributing to a wave of bankruptcies. The collapse of these businesses not only increased unemployment directly but also reduced economic output, further depressing wages and consumer spending.

Foreclosures and bank failures also had a deflationary impact, which worsened the economic crisis and unemployment. As banks liquidated assets, including foreclosed properties, they flooded the market with cheap goods and real estate, driving down prices. Deflation increased the real burden of debt for borrowers, making it even harder for them to repay loans and avoid foreclosure. Simultaneously, falling prices reduced corporate profits, leading to further layoffs and wage cuts. This deflationary spiral deepened the Depression, as consumers and businesses delayed spending in anticipation of lower prices, further stifling economic activity and employment.

The interplay between foreclosures, bank failures, and unemployment highlights the systemic nature of the Great Depression. Policymakers at the time failed to address the banking crisis effectively, allowing it to metastasize into a full-blown economic collapse. The absence of deposit insurance and a lender of last resort mechanism meant that bank failures were both frequent and devastating. The lessons from this period underscore the importance of a stable financial system in maintaining economic health. Subsequent reforms, such as the establishment of the Federal Deposit Insurance Corporation (FDIC) and stronger banking regulations, were direct responses to the role of bank failures and foreclosures in deepening the Great Depression and its associated unemployment crisis.

Who Owns Ally Bank? Understanding the Ownership of Ally Bank

You may want to see also

Explore related products

![]()

Foreclosures reduce consumer spending, worsening deflation and economic stagnation

During the Great Depression, bank foreclosures played a significant role in reducing consumer spending, which in turn exacerbated deflation and economic stagnation. When banks foreclosed on homes and farms, families lost their primary assets and were often left with little to no disposable income. This sudden loss of wealth had a direct impact on their ability to purchase goods and services, as they were forced to prioritize basic necessities like food and shelter. As a result, consumer demand plummeted, causing businesses to reduce production and lay off workers, further decreasing overall spending power in the economy.

The reduction in consumer spending created a vicious cycle that worsened deflation. With less demand for goods and services, prices began to fall, leading to a deflationary spiral. As prices dropped, consumers delayed purchases, expecting prices to fall even further, which in turn reduced business revenues and profits. This decline in economic activity forced companies to cut costs, often by reducing wages or laying off employees, thereby decreasing the overall income available for spending. The continuous decline in prices and economic activity made it increasingly difficult for individuals and businesses to repay debts, leading to more foreclosures and further reductions in consumer spending.

Foreclosures also had a psychological impact on consumers, fostering a sense of economic uncertainty and fear. As people witnessed their neighbors losing homes and livelihoods, they became more cautious with their spending, saving more and consuming less. This shift in consumer behavior contributed to a decrease in aggregate demand, which is essential for economic growth. The widespread fear of job loss and financial instability led to a hoarding of cash, as individuals and families prioritized financial security over discretionary spending. This behavioral change reduced the velocity of money in the economy, slowing economic activity and deepening the stagnation.

The decline in consumer spending due to foreclosures had a ripple effect across various sectors of the economy. Industries such as manufacturing, retail, and construction, which heavily relied on consumer demand, experienced sharp declines in sales and production. This led to widespread business failures and further job losses, reducing the overall income available for spending. As unemployment rose, the purchasing power of the population decreased, creating a feedback loop that perpetuated deflation and economic stagnation. The interconnectedness of these sectors meant that the impact of foreclosures was felt throughout the entire economy, amplifying the severity of the Great Depression.

Moreover, the reduction in consumer spending hindered the ability of businesses to invest in future growth. With lower revenues and uncertain economic conditions, companies were reluctant to expand operations or hire new workers. This lack of investment further stifled economic recovery, as innovation and productivity growth slowed. The combination of reduced consumer spending, declining business investment, and widespread unemployment created an environment where economic stagnation became self-sustaining. Foreclosures, by initiating this chain of events, were a critical factor in the prolonged and severe nature of the Great Depression, highlighting the importance of addressing housing and financial stability in economic policy.

Israeli Settlements: Legality in the West Bank

You may want to see also

Explore related products

![]()

Loss of homes leads to widespread homelessness and social instability

The wave of bank foreclosures during the Great Depression had a devastating impact on American families, as millions lost their homes due to an inability to keep up with mortgage payments. With unemployment soaring and the economy in freefall, many homeowners found themselves without the means to pay their mortgages, leading to a sharp increase in foreclosures. Banks, already struggling with insolvency, were forced to repossess homes en masse, leaving countless families displaced. This sudden loss of homes did not just strip individuals of their most valuable asset; it also uprooted families from their communities, severing social ties and support networks that were crucial for emotional and financial stability.

The immediate consequence of widespread foreclosures was a dramatic rise in homelessness. Families who had once owned their homes were now forced to seek shelter in makeshift camps, often referred to as "Hoovervilles," named after President Herbert Hoover, who was blamed for the economic crisis. These shantytowns sprang up across the country, housing the newly homeless in squalid and overcrowded conditions. The lack of adequate shelter exposed individuals to harsh weather, disease, and malnutrition, further exacerbating their suffering. Children, in particular, suffered from disrupted education and the trauma of losing their homes, which had long-term effects on their development and well-being.

Homelessness on such a massive scale also contributed to social instability. The loss of homes eroded the sense of security and dignity that comes with having a permanent residence, leading to increased desperation and frustration among the affected population. This desperation often manifested in rising crime rates, as individuals turned to theft or other illegal activities to survive. Additionally, the sight of once-prosperous families living in poverty and despair fueled public discontent and eroded trust in government and financial institutions. Protests and riots became more frequent, as people demanded relief and accountability for their plight.

The social fabric of communities was further strained as the homeless population grew. Local governments and charities were overwhelmed by the sheer number of people in need, leading to inadequate resources for food, shelter, and healthcare. This strain on public services deepened societal divisions, as those who still had homes grew fearful of the growing underclass. The breakdown of community cohesion also weakened the collective resilience needed to weather the economic storm, making recovery even more challenging. The loss of homes, therefore, was not just an individual tragedy but a catalyst for broader social unraveling.

Finally, the psychological impact of losing one's home cannot be overstated. For many, their home represented not just a physical space but a symbol of stability, identity, and achievement. The loss of this cornerstone of family life led to widespread feelings of hopelessness, shame, and despair. Mental health issues such as depression and anxiety became rampant, further crippling individuals' ability to seek employment or rebuild their lives. This emotional toll, combined with the physical hardships of homelessness, created a cycle of poverty and instability that persisted long after the Great Depression officially ended. The legacy of these foreclosures underscored the profound connection between housing security and societal stability.

When to Send 1099s for Bank Fees

You may want to see also

Explore related products

![]()

Government intervention in foreclosures delays economic recovery during the Depression

During the Great Depression, bank foreclosures played a significant role in exacerbating economic hardship, as millions of Americans lost their homes and farms due to an inability to repay loans. The collapse of the banking system and the subsequent wave of foreclosures created a vicious cycle of declining property values, reduced consumer spending, and widespread unemployment. In response to this crisis, the government implemented various interventionist policies aimed at mitigating the impact of foreclosures. However, while these measures were intended to provide relief, they often had unintended consequences that delayed economic recovery. One of the primary issues was the extension of loan repayment periods and the reduction of interest rates, which, although helpful to some borrowers, discouraged banks from lending and stifled new investment.

Government intervention in foreclosures during the Depression frequently involved the creation of new agencies and programs designed to refinance mortgages and prevent further defaults. For instance, the Home Owners' Loan Corporation (HOLC) was established in 1933 to refinance mortgages for homeowners at risk of foreclosure. While the HOLC succeeded in saving over a million homes, it also contributed to market distortions by artificially propping up property values and delaying the necessary correction in housing prices. This delay hindered the natural process of market adjustment, preventing resources from being reallocated efficiently and slowing the overall economic recovery.

Another aspect of government intervention was the implementation of moratoriums on foreclosures, which temporarily halted the eviction of homeowners. These moratoriums provided short-term relief but created long-term uncertainty for both lenders and borrowers. Banks became increasingly reluctant to issue new loans, fearing that future government interventions could undermine their ability to recover debts. This reluctance tightened credit markets, reducing the availability of funds for businesses and consumers alike. As a result, economic activity remained subdued, and the recovery process was prolonged.

Furthermore, government policies often prioritized political expediency over economic efficiency, leading to inefficient resource allocation. For example, the Agricultural Adjustment Act (AAA) sought to reduce farm foreclosures by paying farmers to limit production, which helped some farmers but also led to the destruction of crops and livestock, exacerbating food shortages and inflating prices. Such interventions not only failed to address the root causes of the foreclosure crisis but also created new economic distortions that impeded recovery. The focus on short-term relief over long-term structural reforms meant that the economy remained fragile and vulnerable to further shocks.

In conclusion, while government intervention in foreclosures during the Great Depression was motivated by a desire to alleviate suffering, it often had counterproductive effects that delayed economic recovery. By distorting market mechanisms, creating uncertainty, and misallocating resources, these policies hindered the natural process of economic adjustment. Although some measures provided temporary relief, they failed to address the underlying issues of overindebtedness and market imbalances. The experience of the Great Depression highlights the importance of carefully designed policies that balance immediate relief with long-term economic stability, ensuring that interventions do not inadvertently prolong crises.

Trump's Federal Bank Takeover: Was It Real?

You may want to see also

Frequently asked questions

Bank foreclosures played a significant role in the onset of the Great Depression by destabilizing the financial system. As banks foreclosed on farms, homes, and businesses due to loan defaults, it led to widespread financial panic. Depositors lost confidence in banks, triggering bank runs, which further depleted reserves and caused thousands of bank failures. This reduced credit availability, stifled economic activity, and deepened the economic downturn.

Bank foreclosures exacerbated unemployment during the Great Depression by forcing businesses and farms to close. When banks seized assets, many businesses could no longer operate, leading to layoffs. Farmers who lost their land were left without a means to earn a living, contributing to rural unemployment. The ripple effect of these closures spread to related industries, further increasing job losses across the economy.

Bank foreclosures devastated housing markets and communities during the Great Depression. Families lost their homes, leading to widespread homelessness and displacement. Neighborhoods deteriorated as vacant properties fell into disrepair, reducing property values and destabilizing communities. The loss of homeownership also eroded personal wealth, limiting economic recovery and perpetuating poverty.

To address bank foreclosures, the U.S. government implemented several measures during the Great Depression. The Home Owners' Loan Corporation (HOLC) was established to refinance mortgages and prevent foreclosures. The Agricultural Adjustment Act (AAA) provided relief to farmers by reducing crop surpluses and stabilizing prices. Additionally, the Banking Act of 1933 (Glass-Steagall Act) introduced reforms to stabilize banks and restore public confidence in the financial system.