The shadow banking system, a critical yet often overlooked component of the global financial landscape, encompasses a vast array of non-bank financial intermediaries and activities that operate outside traditional banking regulations. Estimates suggest its size is substantial, with some studies indicating it rivals or even surpasses the traditional banking sector in scale. As of recent data, the shadow banking system is estimated to account for trillions of dollars in assets globally, with significant portions concentrated in the United States, China, and Europe. Its growth has been fueled by the increasing demand for credit, regulatory arbitrage, and the rise of complex financial instruments. However, its opacity and lack of oversight raise concerns about systemic risks, particularly during periods of financial stress. Understanding the true size and scope of the shadow banking system is essential for policymakers and regulators to mitigate potential risks and ensure financial stability.

Explore related products

What You'll Learn

![]()

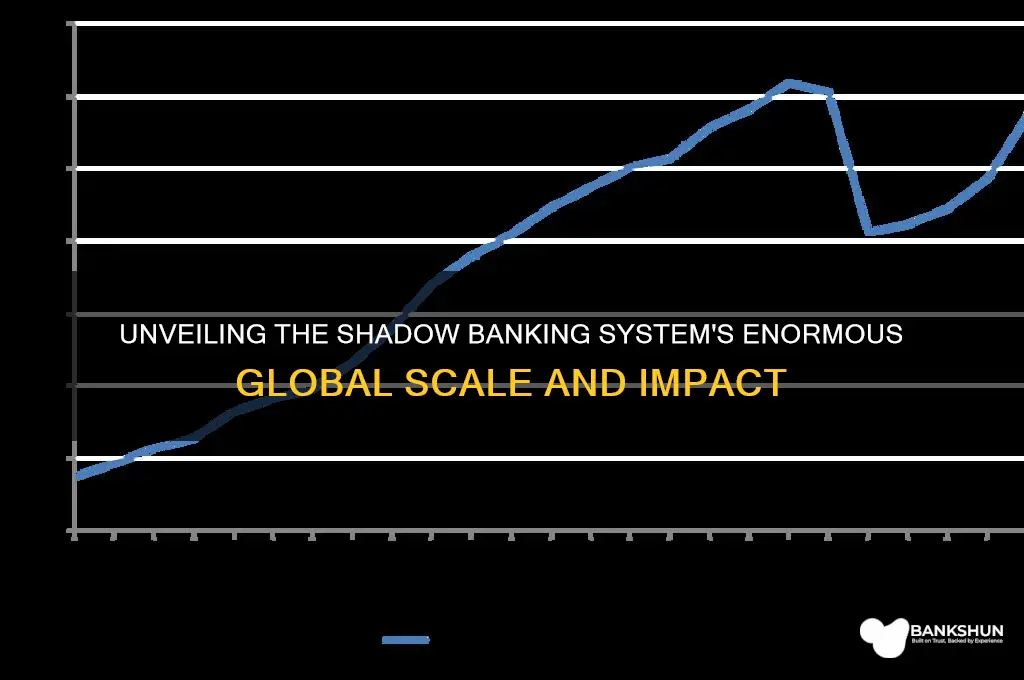

Global Shadow Banking Assets

The global shadow banking system, often referred to as non-bank financial intermediation, has grown significantly over the past few decades, becoming a critical component of the global financial landscape. Global shadow banking assets are estimated to be in the tens of trillions of dollars, rivaling the size of traditional banking systems in many countries. According to the Financial Stability Board (FSB), which monitors and provides data on shadow banking activities, the total assets of the global shadow banking system stood at approximately $60 trillion in 2022. This figure represents a substantial portion of the global financial system, highlighting the sector's importance and potential risks.

Shadow banking encompasses a wide range of entities and activities, including investment funds, money market funds, hedge funds, and structured finance vehicles. These entities operate outside the traditional banking regulatory framework, allowing them to engage in credit intermediation and maturity transformation. Global shadow banking assets are particularly significant in advanced economies, where they account for a larger share of financial activity. For instance, in the United States and Europe, shadow banking assets constitute a substantial portion of the overall financial system, often exceeding 50% of GDP. In emerging markets, while the shadow banking sector is smaller in relative terms, it has been growing rapidly, driven by increasing demand for credit and financial innovation.

One of the key drivers of the growth in global shadow banking assets is the search for yield in a low-interest-rate environment. Institutional investors, such as pension funds and insurance companies, have turned to shadow banking entities to achieve higher returns on their investments. Additionally, regulatory arbitrage has played a role, as some financial activities migrate to less regulated shadow banking entities to avoid stringent capital and liquidity requirements imposed on traditional banks. However, this growth has raised concerns among regulators and policymakers about financial stability, as shadow banking activities can amplify systemic risks, particularly during periods of market stress.

The size and complexity of global shadow banking assets pose challenges for regulators seeking to monitor and mitigate risks. Unlike traditional banks, shadow banking entities are not subject to uniform global regulations, making it difficult to assess their interconnectedness and potential impact on the broader financial system. Efforts by organizations like the FSB to enhance transparency and oversight have led to improved data collection and reporting, but gaps remain. For example, the lack of consistent definitions and reporting standards across jurisdictions complicates efforts to accurately measure the scale and risks of shadow banking activities.

Despite these challenges, global shadow banking assets continue to play a vital role in channeling funds from savers to borrowers, particularly in sectors underserved by traditional banks. They provide liquidity, diversify funding sources, and support economic growth. However, their rapid expansion underscores the need for a balanced regulatory approach that fosters innovation while safeguarding financial stability. Policymakers must address the risks associated with shadow banking, such as leverage, liquidity mismatches, and opacity, without stifling the benefits it brings to the global economy.

In conclusion, global shadow banking assets represent a significant and growing segment of the global financial system, with estimates placing their size at around $60 trillion. Their expansion reflects broader trends in financial innovation and the evolving needs of investors and borrowers. While shadow banking enhances market efficiency and credit availability, it also introduces risks that require careful monitoring and regulation. As the sector continues to evolve, international cooperation and robust regulatory frameworks will be essential to ensure its contributions to economic growth are sustainable and do not undermine financial stability.

Israel's Skin Bank: The World's Largest? Uncovering the Truth

You may want to see also

Explore related products

$157.17 $199.99

![]()

Shadow Banking vs. Traditional Banking

The shadow banking system, often referred to as non-bank financial intermediation, operates outside the traditional banking sector but performs similar functions, such as credit intermediation and maturity transformation. Unlike traditional banks, shadow banking entities—which include investment banks, money market funds, hedge funds, and structured investment vehicles—are not subject to the same stringent regulations. This lack of oversight allows them to grow rapidly, often fueled by investor demand for higher yields and more flexible financial products. According to estimates from the Financial Stability Board (FSB), the global shadow banking system's assets reached approximately $60 trillion in 2021, highlighting its significant size and influence in the global financial ecosystem.

One of the key differences between shadow banking and traditional banking lies in their regulatory frameworks. Traditional banks are heavily regulated, with requirements for capital adequacy, liquidity ratios, and deposit insurance to protect customers and maintain financial stability. In contrast, shadow banking entities operate in a less regulated environment, which enables them to take on higher risks and offer more innovative products. However, this also makes them more vulnerable to systemic risks, as evidenced during the 2008 financial crisis when the collapse of shadow banking entities like Lehman Brothers exacerbated the global downturn. The absence of a safety net in shadow banking means that investors bear more risk, and the potential for contagion is higher.

Another critical distinction is the funding structure. Traditional banks rely primarily on customer deposits, which are insured and provide a stable source of funding. Shadow banks, on the other hand, depend on wholesale funding, such as repurchase agreements (repos) and short-term loans, which can be volatile and prone to sudden withdrawals. This reliance on market-based funding makes shadow banks more susceptible to liquidity shocks, particularly during times of financial stress. For instance, during the 2020 market turmoil caused by the COVID-19 pandemic, shadow banking entities faced significant liquidity challenges, prompting central banks to intervene with emergency lending facilities.

The size and growth of the shadow banking system also raise questions about its role in financial stability. While traditional banks are subject to regular stress tests and supervisory oversight, shadow banking activities often occur in opaque markets, making it difficult for regulators to monitor risks effectively. The interconnectedness between shadow banks and traditional banks further complicates matters, as distress in one sector can quickly spill over to the other. For example, traditional banks may have exposure to shadow banking entities through lending or investment activities, creating channels for risk transmission.

Despite these risks, shadow banking plays a crucial role in diversifying the financial system and providing alternative sources of credit, particularly for borrowers who may not qualify for traditional bank loans. It also fosters innovation in financial products and services, catering to the needs of sophisticated investors and institutions. However, the trade-off between innovation and stability remains a central challenge. Policymakers must strike a balance by implementing targeted regulations that mitigate systemic risks without stifling the benefits that shadow banking brings to the broader economy.

In conclusion, the shadow banking system's size and complexity underscore its importance as a complement to traditional banking. While it offers advantages in terms of flexibility and innovation, its lack of regulation and reliance on volatile funding sources pose significant risks. Understanding the differences between shadow banking and traditional banking is essential for assessing their respective roles in the financial system and designing policies that ensure stability while promoting growth. As the shadow banking sector continues to evolve, ongoing vigilance and adaptive regulation will be critical to managing its potential impact on global financial health.

Avoid Fees: Understand Bank Charges on Negative Balances

You may want to see also

Explore related products

![The Shadow Banker's Secrets: Investment Banking for Alternatives [2nd Edition]](https://m.media-amazon.com/images/I/61ZpfJjflvL._AC_UY218_.jpg)

![]()

Regulatory Oversight Challenges

The shadow banking system, a vast network of non-bank financial intermediaries, presents significant regulatory oversight challenges due to its size, complexity, and opacity. Estimates suggest that the global shadow banking sector assets range from $50 trillion to $100 trillion, rivaling or even surpassing the traditional banking system in some regions. This scale alone underscores the difficulty regulators face in monitoring and mitigating risks within this sector. Unlike traditional banks, shadow banking entities—such as investment funds, money market funds, and structured investment vehicles—operate outside the stringent regulatory frameworks designed for banks. This lack of uniform oversight creates gaps that can amplify systemic risks, particularly during periods of financial stress.

One of the primary regulatory oversight challenges is the fragmented and inconsistent regulatory environment across jurisdictions. Shadow banking activities often span multiple countries, each with its own regulatory approach. For instance, while some nations have implemented stricter rules for money market funds or securitization practices, others remain lax, creating regulatory arbitrage opportunities. This inconsistency allows shadow banking entities to exploit loopholes, shifting operations to less regulated markets. Harmonizing global regulatory standards is essential but remains elusive due to differing national priorities and legal frameworks.

Another critical challenge is the opacity and complexity of shadow banking activities. Many shadow banking entities engage in intricate transactions, such as securitization and repo markets, which are difficult to track and assess for risk. The use of special purpose vehicles (SPVs) and off-balance-sheet structures further obscures the true nature and extent of their activities. Regulators often lack real-time data and transparency into these operations, making it challenging to identify emerging risks or enforce compliance. Enhancing data collection and reporting requirements is crucial but requires significant technological and operational investments.

The interconnectedness of shadow banking with the traditional financial system also poses regulatory challenges. Shadow banks rely heavily on short-term funding from traditional banks and capital markets, creating a web of dependencies. During times of market stress, this interconnectedness can lead to rapid contagion, as seen during the 2008 financial crisis. Regulators struggle to monitor these linkages effectively, as shadow banking entities are not subject to the same liquidity and capital requirements as banks. Strengthening macroprudential oversight and stress testing frameworks is necessary to address these systemic risks.

Finally, the rapid innovation and evolution of shadow banking outpace regulatory frameworks. New financial products, technologies, and business models emerge constantly, often in response to existing regulations. For example, the rise of decentralized finance (DeFi) and digital assets introduces novel risks that traditional regulatory tools are ill-equipped to handle. Regulators must adopt a more agile and forward-looking approach, balancing innovation with risk management. This includes fostering international cooperation and leveraging technology, such as artificial intelligence and blockchain, to enhance monitoring capabilities.

In conclusion, the regulatory oversight challenges of the shadow banking system are multifaceted and require a coordinated, proactive response. Addressing these challenges demands global regulatory harmonization, improved transparency, robust risk assessment tools, and adaptive regulatory frameworks. Without such measures, the shadow banking system will continue to pose significant risks to financial stability.

Finding Mortgage Lenders: The Bank Rate's Limitations

You may want to see also

Explore related products

$31.85 $42.99

![]()

Shadow Banking in Emerging Markets

The shadow banking system, often referred to as non-bank financial intermediation, plays a significant role in emerging markets, where it has grown rapidly in recent years. Shadow banking activities in these economies are driven by factors such as limited access to traditional banking services, high demand for credit, and regulatory arbitrage opportunities. In emerging markets, shadow banking entities include non-bank financial institutions, money market funds, pawnshops, and peer-to-peer (P2P) lending platforms. According to estimates, the size of the shadow banking system in emerging markets is substantial, accounting for a significant portion of the global shadow banking assets. For instance, China, one of the largest emerging markets, has a shadow banking sector estimated to be worth trillions of dollars, with wealth management products, trust loans, and underground banking being the primary components.

In many emerging markets, shadow banking has become an essential source of credit for small and medium-sized enterprises (SMEs) and individuals who are often underserved by traditional banks. This is particularly true in countries with underdeveloped financial systems, where shadow banking entities fill the gap by providing alternative financing options. However, the rapid growth of shadow banking in these markets has also raised concerns about financial stability, as these entities often operate outside the regulatory perimeter, making them more susceptible to risks such as liquidity mismatches, credit defaults, and fraud. Moreover, the interconnectedness between shadow banking entities and the formal banking system can amplify these risks, potentially leading to systemic vulnerabilities.

The size and complexity of shadow banking in emerging markets vary widely across countries, depending on factors such as the level of financial development, regulatory frameworks, and economic conditions. In some countries, such as India and Brazil, shadow banking activities are relatively small compared to the overall financial system, while in others, like China and Indonesia, they play a more significant role. According to a report by the Financial Stability Board (FSB), emerging markets account for a substantial share of global shadow banking assets, with Asia being the largest contributor. The report highlights that the shadow banking system in emerging markets is often characterized by a high degree of informality, with many activities taking place outside the formal financial sector.

One of the key challenges in assessing the size and risks of shadow banking in emerging markets is the lack of comprehensive data and transparency. Many shadow banking entities operate in a regulatory gray area, making it difficult for authorities to monitor their activities and assess potential risks. Furthermore, the diverse nature of shadow banking activities across emerging markets requires a nuanced approach to regulation and supervision. Policymakers need to strike a balance between promoting financial inclusion and innovation, while also safeguarding financial stability and consumer protection. This can be achieved through a combination of measures, including enhancing data collection and reporting requirements, strengthening regulatory frameworks, and promoting financial literacy among consumers.

To address the risks associated with shadow banking in emerging markets, regulators and policymakers need to adopt a proactive and coordinated approach. This includes improving the monitoring and supervision of shadow banking entities, enhancing disclosure requirements, and promoting the development of robust risk management frameworks. Additionally, there is a need for greater international cooperation and information sharing among regulators, given the cross-border nature of many shadow banking activities. By taking a comprehensive and forward-looking approach, emerging markets can harness the benefits of shadow banking while mitigating its risks, ultimately contributing to a more inclusive, stable, and resilient financial system. As the shadow banking system in emerging markets continues to evolve, it is essential for stakeholders to remain vigilant and adaptive, ensuring that the benefits of financial innovation are shared widely, while minimizing the potential risks to financial stability.

Stride Bank and Chime: What's the Difference?

You may want to see also

Explore related products

![]()

Risks to Financial Stability

The shadow banking system, estimated to be worth over $50 trillion globally, operates outside the traditional banking sector and is largely unregulated. Its size and complexity pose significant risks to financial stability, particularly due to its interconnectedness with the formal banking system. Shadow banks, which include entities like investment funds, money market funds, and structured investment vehicles, often engage in credit intermediation, maturity transformation, and leverage, similar to traditional banks. However, they lack the same level of oversight, capital requirements, and access to central bank liquidity. This opacity and lack of regulation make it difficult for regulators to monitor systemic risks effectively.

One of the primary risks to financial stability is the potential for contagion and systemic risk amplification. Shadow banks are deeply interconnected with traditional banks through funding relationships, asset holdings, and derivative contracts. During times of market stress, a failure in one part of the shadow banking system can quickly spread to other financial institutions, triggering a domino effect. For example, the collapse of Lehman Brothers in 2008 highlighted how the shadow banking system’s reliance on short-term funding (e.g., repurchase agreements) can lead to sudden liquidity droughts, freezing credit markets and destabilizing the broader financial system.

Another critical risk is liquidity mismatch and run dynamics. Many shadow banking entities fund long-term, illiquid assets with short-term liabilities, creating a vulnerability to liquidity shocks. If investors lose confidence and withdraw funds en masse, these institutions may be forced to sell assets at fire-sale prices, exacerbating market downturns. Money market funds, for instance, are particularly susceptible to runs, as seen during the 2008 crisis when the Reserve Primary Fund "broke the buck," leading to widespread panic and intervention by central banks.

Leverage and opacity further compound these risks. Shadow banks often operate with high levels of leverage, amplifying both gains and losses. Unlike traditional banks, their leverage is not subject to uniform regulatory limits, making it difficult to assess the true extent of risk in the system. Additionally, the use of complex financial instruments and off-balance-sheet activities obscures the interconnectedness and risk exposures of shadow banks, leaving regulators and investors in the dark about potential vulnerabilities.

Finally, the regulatory arbitrage inherent in the shadow banking system poses a long-term threat to financial stability. As traditional banks face stricter capital and liquidity requirements post-2008, more financial activities have migrated to the shadow banking sector to avoid regulation. This not only undermines the effectiveness of post-crisis reforms but also concentrates risk in an under-regulated area. Without comprehensive oversight and harmonized global regulations, the shadow banking system will continue to grow, potentially becoming a source of future financial crises.

In conclusion, the size and complexity of the shadow banking system, combined with its lack of regulation and transparency, create significant risks to financial stability. Addressing these risks requires enhanced regulatory frameworks, improved monitoring of interconnectedness, and global coordination to prevent regulatory arbitrage. Failure to do so could leave the financial system vulnerable to shocks that reverberate far beyond the shadow banking sector.

Venmo Transfers: Weekends and Bank Holidays

You may want to see also

Frequently asked questions

The global shadow banking system is estimated to be worth over $50 trillion, though exact figures vary due to its unregulated and opaque nature.

Shadow banking accounts for approximately 15-20% of the total global financial system, with significant regional variations.

The United States, China, and the Eurozone are among the largest contributors to the shadow banking system, with China’s sector growing rapidly in recent years.

While still smaller than traditional banking, shadow banking has grown significantly, with its assets often rivaling those of major banks in some regions.

The shadow banking system has been growing, particularly in emerging markets, though regulatory efforts in some countries have slowed its expansion in recent years.