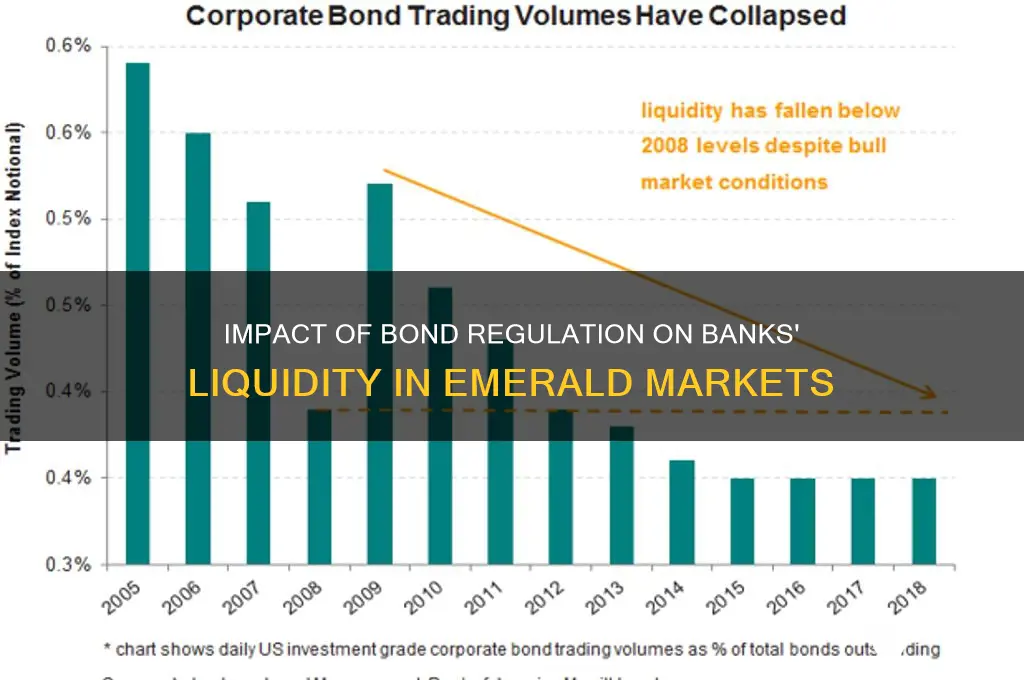

Bond regulation plays a critical role in shaping banks' liquidity management, particularly in the context of Emerald, where financial stability and market efficiency are paramount. Regulatory frameworks governing bond issuance, trading, and holding directly impact banks' ability to maintain sufficient liquid assets to meet short-term obligations and manage cash flows effectively. Stricter bond regulations, such as higher capital requirements or tighter eligibility criteria for collateral, can reduce banks' liquidity by limiting their access to bond markets or increasing the cost of holding liquid assets. Conversely, more flexible regulations may enhance liquidity by facilitating smoother bond transactions and improving market depth. In Emerald, the interplay between bond regulation and bank liquidity is further influenced by local economic conditions, investor sentiment, and the broader regulatory environment, making it essential for policymakers to strike a balance that fosters both financial stability and market liquidity.

Explore related products

What You'll Learn

- Impact of bond regulations on banks' liquidity management strategies

- Regulatory compliance costs affecting banks' bond market participation

- Bond regulation influence on banks' asset-liability mismatch risks

- Effects of liquidity requirements on banks' bond portfolio composition

- Role of bond regulations in stabilizing banks' funding sources

![]()

Impact of bond regulations on banks' liquidity management strategies

Bond regulations have a profound impact on banks' liquidity management strategies, as they directly influence the availability, cost, and risk associated with liquid assets. One of the primary effects of bond regulations is the requirement for banks to hold a higher proportion of high-quality liquid assets (HQLA), such as government bonds, to meet liquidity coverage ratios (LCR) and net stable funding ratios (NSFR). This shift compels banks to reallocate their portfolios toward safer, more liquid instruments, reducing their reliance on less liquid assets like corporate bonds or structured products. While this enhances overall financial stability, it can also limit banks' ability to generate higher returns from riskier assets, thereby affecting profitability.

Another significant impact of bond regulations is the increased cost of compliance and the need for more sophisticated liquidity management frameworks. Banks must invest in robust systems to monitor and report their liquidity positions in real-time, ensuring compliance with regulatory thresholds. This includes stress testing their bond portfolios to assess resilience under adverse market conditions. As a result, banks often adopt more conservative liquidity management strategies, such as maintaining larger buffers of liquid assets than the minimum regulatory requirements. This conservatism, while prudent, can tie up capital that could otherwise be deployed for lending or investment, potentially constraining credit availability to the broader economy.

Bond regulations also influence banks' funding strategies by encouraging longer-term funding sources over short-term wholesale funding. For instance, regulations like the NSFR incentivize banks to issue longer-dated bonds or attract stable retail deposits to reduce reliance on volatile short-term funding markets. This shift helps mitigate liquidity risks during periods of market stress but may increase funding costs if long-term interest rates are higher. Additionally, banks may face challenges in issuing bonds that meet regulatory criteria for HQLA, particularly in markets with limited supply of eligible sovereign or supranational bonds, further complicating their liquidity management efforts.

The interplay between bond regulations and market dynamics is another critical factor affecting liquidity management. Regulatory requirements can create demand pressures for specific types of bonds, such as government securities, potentially distorting their prices and yields. Banks must navigate these market conditions carefully, balancing the need for regulatory compliance with the goal of optimizing their asset-liability management. For example, if government bond yields are low due to high regulatory demand, banks may need to diversify into other liquid assets, albeit with higher risk profiles, to maintain yield levels.

Lastly, bond regulations have spurred innovation in liquidity management tools and techniques. Banks are increasingly leveraging technology, such as data analytics and artificial intelligence, to forecast liquidity needs, optimize bond portfolios, and enhance risk monitoring. Regulatory pressures have also driven the development of new financial instruments, such as contingent convertible bonds (CoCo bonds), which can absorb losses during stress periods while providing flexibility in liquidity management. However, the complexity of these tools requires banks to invest in skilled personnel and advanced infrastructure, adding to operational costs but ultimately improving their ability to manage liquidity risks effectively.

In summary, bond regulations significantly shape banks' liquidity management strategies by dictating the composition of their asset portfolios, increasing compliance costs, influencing funding decisions, and driving innovation. While these regulations enhance financial stability, they also present challenges that require banks to adopt more conservative, data-driven, and adaptive approaches to liquidity management. Balancing regulatory compliance with profitability and market responsiveness remains a key priority for banks operating in this evolving regulatory landscape.

Iowa Bank Meeting Minutes: Public Access or Private?

You may want to see also

Explore related products

![]()

Regulatory compliance costs affecting banks' bond market participation

Regulatory compliance costs have become a significant factor influencing banks' participation in the bond market, particularly in the context of how bond regulations affect bank liquidity. As financial institutions navigate an increasingly complex regulatory landscape, the associated costs of compliance are reshaping their strategies and capabilities in bond market operations. These costs encompass not only direct expenses, such as hiring specialized staff and investing in technology, but also indirect costs, including the opportunity cost of allocating resources away from revenue-generating activities. For banks, the burden of compliance often translates into reduced flexibility in managing their liquidity positions, as resources that could be used to optimize bond portfolios are instead diverted to meet regulatory requirements.

One of the primary ways regulatory compliance costs impact banks' bond market participation is through increased operational expenses. Banks are required to implement robust systems and processes to ensure adherence to regulations such as Basel III, MiFID II, and Dodd-Frank, which govern capital adequacy, market transparency, and risk management. These systems demand substantial upfront and ongoing investments, particularly in data management, reporting, and monitoring capabilities. As a result, banks may find it less economically viable to engage in certain bond market activities, especially in less liquid or more complex segments where the cost-benefit ratio is unfavorable. This can lead to a reduction in market-making activities, thereby affecting overall market liquidity.

Moreover, regulatory compliance costs can constrain banks' ability to hold and trade bonds effectively, directly impacting their liquidity management. For instance, higher capital requirements under regulations like the Supplementary Leverage Ratio (SLR) increase the cost of holding bonds, particularly those with lower yields or longer maturities. Banks may respond by reducing their bond inventories or shifting towards shorter-duration, more liquid securities, which can limit their role as market intermediaries. This shift not only affects the banks' profitability but also reduces the depth and resilience of the bond market, as fewer participants are willing or able to provide liquidity during times of stress.

Another critical aspect is the impact of regulatory compliance on banks' risk appetite and strategic decision-making. The need to comply with stringent regulations often leads banks to adopt a more conservative approach to bond market participation. For example, banks may prioritize low-risk, high-liquidity assets over higher-yielding but less liquid bonds to minimize regulatory capital charges. While this approach helps in meeting compliance requirements, it can stifle innovation and limit the banks' ability to diversify their portfolios effectively. Consequently, the bond market may experience reduced activity and innovation, as banks focus on minimizing compliance costs rather than exploring new opportunities.

In conclusion, regulatory compliance costs are a critical determinant of banks' bond market participation, with far-reaching implications for their liquidity management and market dynamics. As these costs continue to rise, banks face difficult trade-offs between maintaining regulatory compliance and optimizing their bond market strategies. Policymakers and regulators must carefully consider the unintended consequences of their actions, ensuring that regulations achieve their intended goals without unduly burdening banks or compromising the liquidity and efficiency of the bond market. Striking this balance is essential for fostering a healthy financial ecosystem where banks can effectively manage liquidity while contributing to the stability and growth of the bond market.

Does Nirvana Seed Bank Ship to the US? Find Out Here

You may want to see also

Explore related products

![]()

Bond regulation influence on banks' asset-liability mismatch risks

Bond regulations play a pivotal role in shaping banks' asset-liability management, particularly in mitigating mismatch risks. Asset-liability mismatch occurs when the maturity or cash flow characteristics of a bank’s assets and liabilities do not align, exposing the institution to liquidity and solvency risks. Bond regulations, such as those governing the issuance, trading, and holding of bonds, directly influence banks' ability to manage these mismatches. For instance, regulations that mandate higher capital requirements for long-term assets or restrict the use of certain types of bonds can force banks to rebalance their portfolios, reducing the likelihood of mismatches. By imposing stricter standards on bond holdings, regulators aim to ensure that banks maintain sufficient liquidity buffers to meet short-term obligations without destabilizing their balance sheets.

One significant way bond regulations impact asset-liability mismatch risks is through maturity transformation constraints. Banks often engage in maturity transformation by funding long-term assets with short-term liabilities, a practice that can exacerbate mismatch risks. Regulatory frameworks, such as Basel III, introduce liquidity coverage ratios (LCR) and net stable funding ratios (NSFR), which require banks to hold a minimum level of high-quality liquid assets (HQLA), including government bonds, to cover short-term outflows. These regulations incentivize banks to align the maturities of their assets and liabilities more closely, reducing the potential for liquidity shortages during stress periods. However, such regulations may also limit banks' ability to profit from maturity transformation, forcing them to adopt more conservative funding strategies.

Another critical aspect of bond regulation is its influence on the composition of banks' bond portfolios. Regulations often differentiate between types of bonds based on their risk profiles, with sovereign bonds typically considered safer than corporate bonds. By favoring the holding of safer, more liquid bonds, regulators aim to enhance banks' resilience to market shocks. For example, banks may be required to hold a higher proportion of government bonds in their HQLA portfolios, which can reduce mismatch risks by ensuring a stable source of liquidity. Conversely, restrictions on riskier bond holdings, such as high-yield corporate bonds, can limit banks' exposure to credit and market risks but may also constrain their ability to generate higher returns, impacting profitability.

The interplay between bond regulations and market conditions further complicates banks' asset-liability management. During periods of economic uncertainty, bond yields may fluctuate significantly, affecting the value and liquidity of banks' bond holdings. Regulatory requirements that mandate mark-to-market accounting for bond portfolios can amplify these effects, as banks may be forced to recognize losses on their balance sheets, potentially triggering liquidity pressures. To mitigate these risks, banks may adopt hedging strategies or diversify their bond portfolios across different issuers and maturities. However, such strategies must comply with regulatory guidelines, which may limit their effectiveness in addressing mismatch risks.

In conclusion, bond regulations have a profound influence on banks' asset-liability mismatch risks by shaping the structure and composition of their balance sheets. While these regulations are designed to enhance financial stability and reduce systemic risks, they also impose constraints on banks' operational flexibility and profitability. Banks must navigate this regulatory landscape carefully, balancing compliance with the need to maintain liquidity and manage risks effectively. As regulatory frameworks continue to evolve, banks will need to adapt their asset-liability management strategies to remain resilient in the face of changing market conditions and regulatory expectations.

Does Citi Bank Group Issue Green Bonds? Exploring Sustainability Efforts

You may want to see also

Explore related products

![]()

Effects of liquidity requirements on banks' bond portfolio composition

Liquidity requirements imposed on banks have a profound impact on the composition of their bond portfolios, as these regulations necessitate a shift towards more liquid assets to meet potential funding needs. Banks are required to hold a certain proportion of high-quality liquid assets (HQLA), such as government bonds and highly rated corporate bonds, to ensure they can withstand short-term liquidity shocks. This regulatory mandate directly influences the types of bonds banks hold, favoring those that are easily convertible to cash without significant loss of value. As a result, banks tend to increase their holdings of sovereign bonds and other HQLA-eligible securities, which are typically more liquid and less risky compared to other bond types.

The emphasis on liquidity also leads to a reduction in the proportion of less liquid bonds in banks' portfolios, such as long-term corporate bonds, asset-backed securities (ABS), and bonds from lower-rated issuers. These assets, while potentially offering higher yields, are more difficult to sell quickly in stressed market conditions, making them less attractive under stringent liquidity requirements. Consequently, banks may reallocate their bond holdings away from these less liquid instruments to avoid falling short of regulatory liquidity thresholds. This reallocation not only affects the risk profile of the bond portfolio but also impacts the overall yield banks can generate from their fixed-income investments.

Another effect of liquidity requirements is the increased demand for short-duration bonds, as they align better with the need to maintain liquid assets. Short-duration bonds are less sensitive to interest rate changes and can be more readily sold or used as collateral in liquidity operations. This shift towards shorter-duration bonds can alter the maturity structure of banks' bond portfolios, potentially reducing their exposure to interest rate risk but also limiting their ability to benefit from higher yields typically associated with longer-term bonds. Banks must carefully balance these trade-offs to ensure compliance with liquidity regulations while optimizing portfolio returns.

Furthermore, liquidity requirements can incentivize banks to diversify their bond portfolios across different issuers and sectors to mitigate concentration risk. Holding a diverse range of liquid assets ensures that banks are not overly reliant on any single market or issuer for their liquidity needs. For instance, banks may increase their holdings of bonds from supranational organizations or diversify across various government and corporate issuers to enhance the resilience of their liquidity buffers. This diversification strategy, while beneficial for liquidity management, adds complexity to portfolio management and requires robust risk assessment frameworks.

Lastly, the impact of liquidity requirements on bond portfolio composition extends to banks' funding strategies and market behavior. As banks prioritize liquid assets, they may become more active participants in primary bond markets for HQLA-eligible securities, influencing issuance volumes and pricing. Additionally, the demand for liquid bonds can affect secondary market dynamics, potentially tightening spreads for highly liquid securities while widening those for less liquid ones. These market effects underscore the broader implications of liquidity regulations on banks' bond portfolio decisions and their interaction with the financial ecosystem.

Sperm Bank Purchase: What You Need to Know

You may want to see also

Explore related products

![]()

Role of bond regulations in stabilizing banks' funding sources

Bond regulations play a pivotal role in stabilizing banks' funding sources by ensuring that these institutions maintain sufficient liquidity to meet their obligations while managing risks effectively. One of the primary ways bond regulations achieve this is by mandating transparency and disclosure requirements. Banks issuing bonds are required to provide detailed information about their financial health, risk exposure, and capital structure. This transparency helps investors make informed decisions, reducing information asymmetry and fostering trust in the banking system. As a result, banks can access funding more reliably, even during periods of market volatility, as investors are better equipped to assess the risks associated with their investments.

Another critical aspect of bond regulations is the imposition of capital adequacy requirements. These rules ensure that banks maintain a minimum level of capital relative to their risk-weighted assets, including bond issuances. By doing so, regulators compel banks to hold sufficient buffers to absorb losses, thereby reducing the likelihood of insolvency. This stability in capital structure enhances banks' ability to issue bonds consistently, as investors are more confident in the bank's ability to honor its debt obligations. Additionally, capital adequacy requirements discourage excessive risk-taking, further stabilizing funding sources by minimizing the potential for sudden liquidity crises.

Bond regulations also contribute to stabilizing funding sources by standardizing bond issuance processes and structures. Regulatory frameworks often dictate the terms and conditions under which bonds can be issued, including maturity profiles, covenants, and redemption features. This standardization reduces complexity and uncertainty for both issuers and investors, making the bond market more efficient and liquid. For banks, this means easier access to funding, as standardized bonds are more attractive to a broader range of investors. Moreover, standardized structures facilitate secondary market trading, providing banks with an additional avenue to manage their liquidity needs.

Furthermore, bond regulations often include provisions for stress testing and scenario analysis, requiring banks to assess their resilience under adverse market conditions. These tests ensure that banks have robust contingency plans to maintain liquidity and honor bond obligations even during financial downturns. By mandating such preparedness, regulators help banks avoid funding shortages that could lead to systemic risks. This proactive approach not only stabilizes individual banks' funding sources but also contributes to the overall stability of the financial system, as banks are better equipped to withstand shocks without resorting to emergency measures.

Lastly, bond regulations often encourage diversification in banks' funding sources by imposing limits on reliance on any single funding channel. For instance, regulators may cap the proportion of a bank's liabilities that can be funded through short-term bonds or wholesale markets. This diversification reduces the vulnerability of banks to specific market disruptions, ensuring a more stable and resilient funding base. By balancing their funding mix, banks can mitigate the risks associated with over-reliance on volatile funding sources, thereby enhancing their overall liquidity position and ability to issue bonds consistently.

In conclusion, bond regulations are instrumental in stabilizing banks' funding sources by promoting transparency, ensuring capital adequacy, standardizing bond issuances, mandating stress testing, and encouraging funding diversification. These measures collectively enhance investor confidence, reduce systemic risks, and ensure that banks maintain sufficient liquidity to meet their obligations. As such, bond regulations are a cornerstone of financial stability, enabling banks to access reliable funding while safeguarding the broader financial ecosystem.

Does the Ex-Im Bank Still Exist? Unraveling Its Current Status

You may want to see also

Frequently asked questions

Bond regulation affects bank liquidity by influencing the availability and cost of funding. Stricter regulations may limit banks' ability to issue bonds, reducing their liquidity, while looser regulations can enhance liquidity by facilitating bond issuance.

Emerald’s bond regulation, if stringent, may require banks to hold more capital against bond issuances, reducing their liquidity. Conversely, if regulations are supportive, banks in Emerald may experience improved liquidity through easier access to bond markets.

Yes, if bond regulations in Emerald become overly restrictive, banks may face a liquidity crunch due to reduced access to bond markets, higher funding costs, and increased capital requirements.

Banks in Emerald may manage liquidity under tight bond regulations by diversifying funding sources, increasing deposits, reducing lending, or relying more on central bank facilities to maintain sufficient liquidity.

Long-term effects depend on the nature of the regulation. Strict regulations may stabilize liquidity by reducing risk but could also stifle growth, while flexible regulations may enhance liquidity and support economic expansion in Emerald.